Focus Turns to Fragile Trade Progress as Dollar Lags in Cautious Markets – Action Forex

Dollar is once again under pressure in a relatively calm Asian session, as broader financial markets appear to have stabilized following the earlier bout of volatility driven by US deficit and debt concerns. Wall Street closed the day nearly flat with little direction, while US 10-year Treasury yield held above the 4.5% level after recent volatility. In Asia, risk appetite is returning modestly, with regional equities trading slightly higher.

The spotlight, however, has shifted back to the slow-moving trade negotiations between the US and several of its major partners. Japan is intensifying its engagement with the US on tariff talks, with top negotiator Ryosei Akazawa said to make a fourth visit to Washington on May 30, just one week after this weekend’s third round. Akazawa is seeking a direct meeting with US Treasury Secretary Scott Bessent, who won’t attend the upcoming session. Prime Minister Shigeru Ishiba also held a 45-minute phone call with US President Donald Trump at the latter’s request, though Ishiba said Trump made no concessions on Japan’s demand for complete tariff elimination.

On the European front, the Financial Times reported that US Trade Representative Jamieson Greer plans to deliver a strong message to European Trade Commissioner Maros Sefcovic. Washington views Brussels’ recent “explanatory note” as insufficient and continues to push for unilateral tariff reductions on US goods. Without meaningful concessions, the US is prepared to impose additional 20% reciprocal tariffs on EU exports.

Meanwhile, US-China communication channels remain open but unclear. A call between Chinese Vice Foreign Minister Ma Zhaoxu and US Deputy Secretary of State Christopher Landau yielded “substantial progress” in Beijing’s phrasing, though neither side confirmed whether tariff issues were addressed. Earlier, Vice Premier He Lifeng emphasized China’s willingness to open its markets further to US firms, a potentially strategic signal of compromise from Beijing amid slow progress elsewhere.

Currency markets continue to reflect a defensive stance. Yen remains the top performer for the week, followed by Euro and Swiss Franc. Dollar lags as the weakest currency, alongside Aussie and Kiwi. Sterling and the Canadian Dollar are holding in mid-pack.

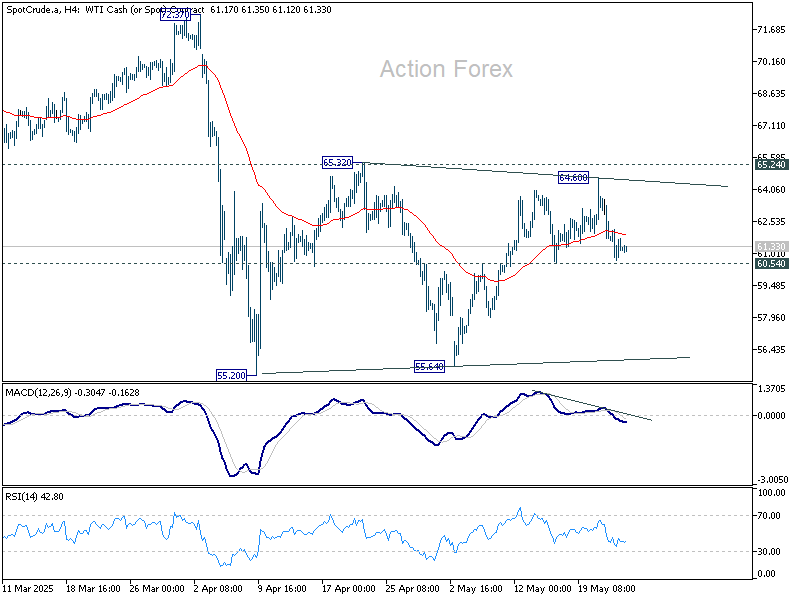

Technically, WTI crude oil reversed quickly after a brief spike to 64.60 earlier in the week. Overall outlook is that price actions from 55.20 low are merely a corrective pattern. Firm break of 60.54 support will suggest that the consolidation has completed with three waves to 64.60. Retest of 55.20/55.64 support zone should then be seen next.

In Asia, at the time of writing, Nikkei is up 0.58%. Hong Kong HSI is up 0.77%. China Shanghai SSE is up 0.03%. Singapore Strait Times is down -0.20%. Japan 10-year JGB yield is down -0.007 at 1.555. Overnight, DOW fell -0.00%. S&P 500 fell -0.04%. NASDAQ rose 0.28%. 10-year yield fell -0.043 to 4.553.

Looking ahead, retail sales data from the UK and Canada are the main focuses of the day.

Sticky inflation persist as Japan’s core CPI climbs to 3.5%

Japan’s inflation pressures remained elevated in April, with the core CPI (excluding fresh food) rising from 3.2% yoy to 3.5% yoy, beating expectations of 3.4% yoy and marking the highest level since January 2023. This keeps core inflation above the BoJ’s 2% target for over three years.

Core-core CPI, which excludes both food and energy, also ticked up from 2.9% yoy to 3.0% yoy, suggesting broader underlying price momentum. Headline CPI held steady at 3.6% yoy.

There were notable upward drivers in inflation. Energy prices surged 9.3% yoy, up from March’s 6.6% yoy. Food prices (excluding fresh items) jumped 7.0% yoy, up from 6.2% yoy. In particular, rice prices soared by 98.4% yoy, a seventh consecutive record high, reflecting persistent supply shortages.

However, services inflation, closely watched by BoJ as a wage-sensitive component, edged slightly lower to 1.3% from 1.4%, tempering some of the hawkish signals.

NZ retail sales rise 0.8% qoq in Q1, but ex-auto growth modest

New Zealand retail sales volumes rose a stronger-than-expected 0.8% qoq in Q1 to NZD 25B, offering a positive surprise relative to market expectations of flat growth.

According to Stats NZ, 10 of the 15 major retail industries saw increased activity, led by a 3.1% jump in motor vehicle and parts retailing and a 3.7% rise in pharmaceutical and other store-based sales. Clothing and accessories also saw a healthy 3.2% gain.

Despite the upbeat headline, underlying momentum appears less robust when excluding the volatile auto sector. Core retail sales rose just 0.4% qoq, sharply missing expectations of a 1.5% qoq rise.

Economic indicators spokesperson Michelle Feyen noted that growth was “modest” and broad-based.

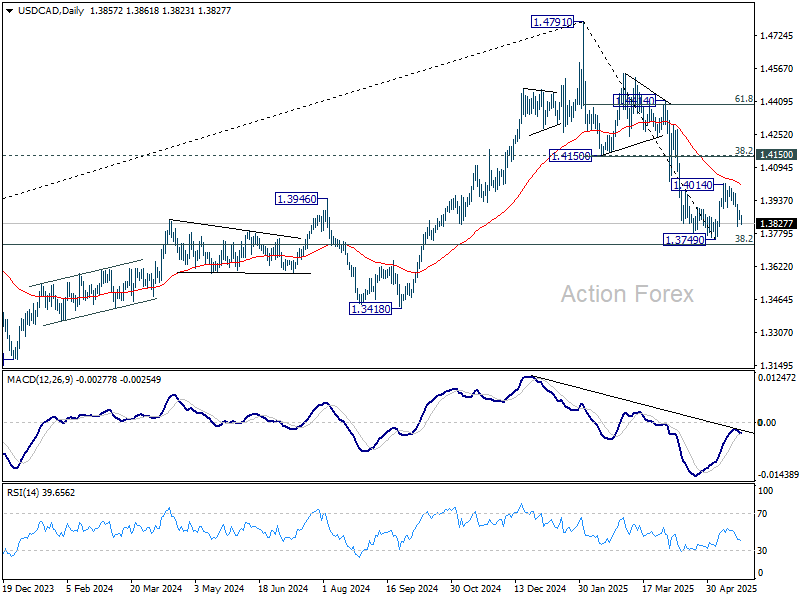

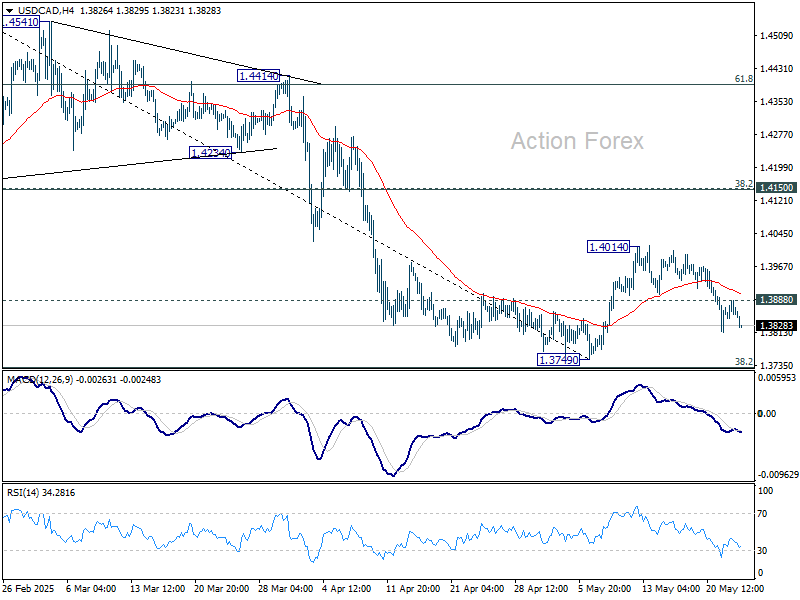

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3840; (P) 1.3864; (R1) 1.3883; More…

Intraday bias in USD/CAD remains mildly on the downside at this point. Deeper decline should be seen for retesting 1.3479 low, or further to 1.3727 key fibonacci level. Nevertheless, break of 1.3888 minor resistance will turn bias back to the upside, to extend the corrective pattern from 1.3749 with another rising leg.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.