Markets Rattled as Trump Threatens 50% Tariffs on EU, Dollar Tumbles – Action Forex

Global financial markets are thrown back into turmoil today after US President Donald Trump reignited trade tensions by announcing he would recommend a sweeping 50% tariff on EU imports starting June 1. In a pointed social media post, Trump accused the EU of stonewalling negotiations, declaring that discussions were “going nowhere.” The announcement came on the heels of another threat, this time directed at Apple, with Trump warning of at least a 25% tariff if the company doesn’t relocate iPhone production to the US.

The market reaction was swift and severe. DOW futures plunged over 500 points, and European equities were battered as traders rushed to reprice geopolitical risk. The shock move revives fears of a new phase in the trade war, one with potentially deeper and more systemic consequences than the US-China dispute, especially given Europe’s central role in global supply chains and transatlantic investment flows.

Currency markets mirrored the chaos. While Euro was understandably under pressure from the tariff news, Dollar was hit even harder, staying at the bottom of the performance board for the day. Traders appear to be weighing the long-term implications of such a dramatic trade escalation on US economy.

Safe haven demand surged, with Yen leading gains. Kiwi and Swiss Franc are following. Sterling held up relatively well thanks to robust retail sales data. Aussie remained relatively steady, though vulnerable to shifts in global risk sentiment.

In Europe, at the time of writing, FTSE is down -0.95%. DAX is down 2.11%. CAC is down -2.33%. UK 10-year yield is down -0.044 at 4.712. Germany 10-year yield is down -0.079 at 2.567. Earlier in Asia, Nikkei rose 0.47%. Hong Kong HSI rose 0.24%. China Shanghai SSE fell -0.94%. Singapore Strait Times rose 0.06%. Japan 10-year JGB yield fell -0.013 to 1.549.

Canada retail sales rise 0.8% mom on autos, underlying momentum weakens

Canada’s retail sales rose by 0.8% mom in March, surpassing expectations of a 0.6% gain. Motor vehicle and parts dealers drove the advance with a strong 4.8% mom rebound. The first quarter posted a solid 1.2% gain in total retail activity, extending the streak of quarterly increases to four.

However, the underlying trend was less encouraging. Retail sales excluding autos plunged -0.7% mom, far worse than the expected -0.1% mom decline.

StatCan’s advance estimate points to a modest 0.5% rebound in April.

ECB’s Lane sees wages easing, cautions on persistent global shocks

ECB Chief Economist Philip Lane expressed confidence that services inflation will continue to moderate, citing subdued outcomes in recent wage agreements.

Speaking at a lecture, Lane noted that the current wage settlements for 2025 are already “quite low,” with those for 2026 appearing even more restrained. That suggested easing cost pressures in the services sector, a key driver of core inflation.

However, Lane tempered optimism by pointing to the persistent volatility in the global economic environment. He highlighted large recent swings in exchange rates and energy prices, attributing them to structural shifts in the global trading system.

ECB’s Rehn and Stournaras back June rate cut

ECB Governing Council members Olli Rehn and Yannis Stournaras signaled support for a rate cut in June, provided that incoming data confirms the current trend of stabilizing inflation and moderate growth. Rehn stressed the importance of maintaining a data-dependent approach amid a backdrop of “pervasive uncertainty” stemming from geopolitical tensions and global trade conflicts.

Speaking in an interview with Kathimerini, Rehn noted that “if incoming data and macroeconomic analysis confirm the current outlook for stabilizing inflation and somewhat subdued growth, the appropriate response in June would be to continue monetary easing and lower interest rates.”

However, he cautioned against making any assumptions beyond June. “let’s stay on the path of data-driven decision-making at every meeting, especially as we find ourselves under the clouds of pervasive uncertainty due to geopolitics and trade wars,” he emphasized.

Stournaras echoed the view of a June cut, but suggested the ECB may pause thereafter to reassess. “I believe we will reduce interest rates one more time in June and then I see a pause,” he said.

UK retail sales beat expectations with 1.2% mom growth, strongest annual gain since 2022

UK retail sales volumes jumped by 1.2% mom in April, significantly above the expected 0.3% mom gain. This marks the fourth consecutive monthly increase, with volumes now at their highest level since July 2022. Food store sales led the rise with a sharp 3.9% rebound, attributed largely to favorable weather conditions, offsetting declines seen in February and March.

On a broader basis, sales volumes grew 1.8% over the three months to April compared to the prior three-month period, the strongest gain since July 2021. Year-on-year, volumes rose 2.6%, the largest increase since March 2022.

Sticky inflation persist as Japan’s core CPI climbs to 3.5%

Japan’s inflation pressures remained elevated in April, with the core CPI (excluding fresh food) rising from 3.2% yoy to 3.5% yoy, beating expectations of 3.4% yoy and marking the highest level since January 2023. This keeps core inflation above the BoJ’s 2% target for over three years.

Core-core CPI, which excludes both food and energy, also ticked up from 2.9% yoy to 3.0% yoy, suggesting broader underlying price momentum. Headline CPI held steady at 3.6% yoy.

There were notable upward drivers in inflation. Energy prices surged 9.3% yoy, up from March’s 6.6% yoy. Food prices (excluding fresh items) jumped 7.0% yoy, up from 6.2% yoy. In particular, rice prices soared by 98.4% yoy, a seventh consecutive record high, reflecting persistent supply shortages.

However, services inflation, closely watched by BoJ as a wage-sensitive component, edged slightly lower to 1.3% from 1.4%, tempering some of the hawkish signals.

NZ retail sales rise 0.8% qoq in Q1, but ex-auto growth modest

New Zealand retail sales volumes rose a stronger-than-expected 0.8% qoq in Q1 to NZD 25B, offering a positive surprise relative to market expectations of flat growth.

According to Stats NZ, 10 of the 15 major retail industries saw increased activity, led by a 3.1% jump in motor vehicle and parts retailing and a 3.7% rise in pharmaceutical and other store-based sales. Clothing and accessories also saw a healthy 3.2% gain.

Despite the upbeat headline, underlying momentum appears less robust when excluding the volatile auto sector. Core retail sales rose just 0.4% qoq, sharply missing expectations of a 1.5% qoq rise.

Economic indicators spokesperson Michelle Feyen noted that growth was “modest” and broad-based.

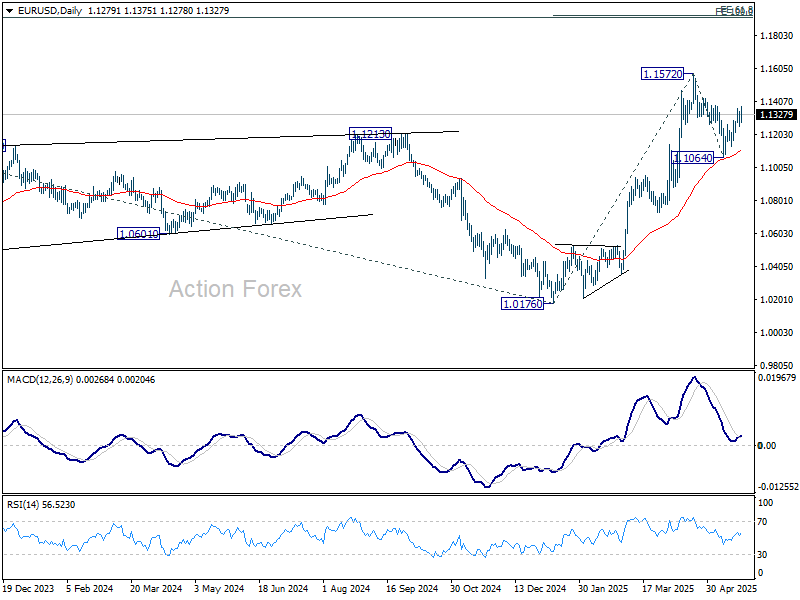

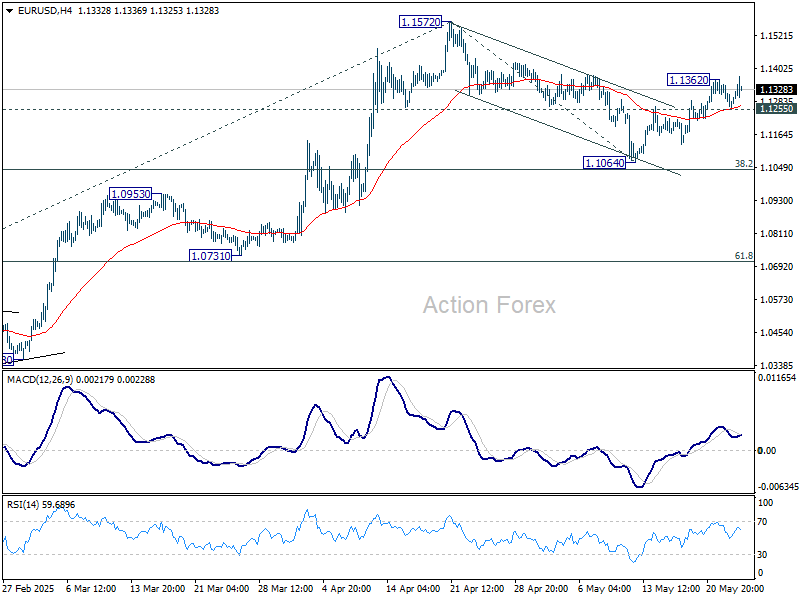

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1242; (P) 1.1294; (R1) 1.1331; More…

Intraday bias in EUR/USD is back on the upside with breach of 1.1362 temporary top. As noted before, correction from 1.1572 could have completed at 1.1064 already. Further rise should be seen to retest 1.1572 first. Firm break there will resume larger up trend. Next near term target will be 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, below 1.1255 minor support will dampen this view and turn intraday bias neutral again.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0818) holds.