Risk Appetite Returns After Trump Backs Off Immediate EU Tariff Threat – Action Forex

Global markets are showing tentative signs of relief after US President Donald Trump walked back his threat to impose a 50% tariff on the European Union. The abrupt shift to reinstate a July 9 deadline for negotiations has helped ease investor concerns for now. Stocks in Germany and France are trading modestly higher in European session, though the UK market remains closed for holiday. US equity futures are also pointing to a firmer open, suggesting a rebound from last week’s tariff-induced selloff. This shift in tone has also taken some steam out of safe-haven flows. Gold prices dipped slightly as investors rotated back into risk assets.

The European Commission confirmed that trade representatives from both sides are scheduled to talk later today, describing the development as a “new impetus”. A Commission spokesperson noted that both parties have agreed to fast-track negotiations and remain in close contact, providing hope that a workable framework could still be reached before the “old” deadline.

In the currency markets, the mildly risk-on environment is supporting higher-beta currencies. Kiwi and Aussie are leading the pack, with Sterling also gaining some traction. On the other hand, traditional safe havens like Yen, Swiss Franc are under modest pressure, while Dollar is also weak. Euro and Loonie positioning in the middle.

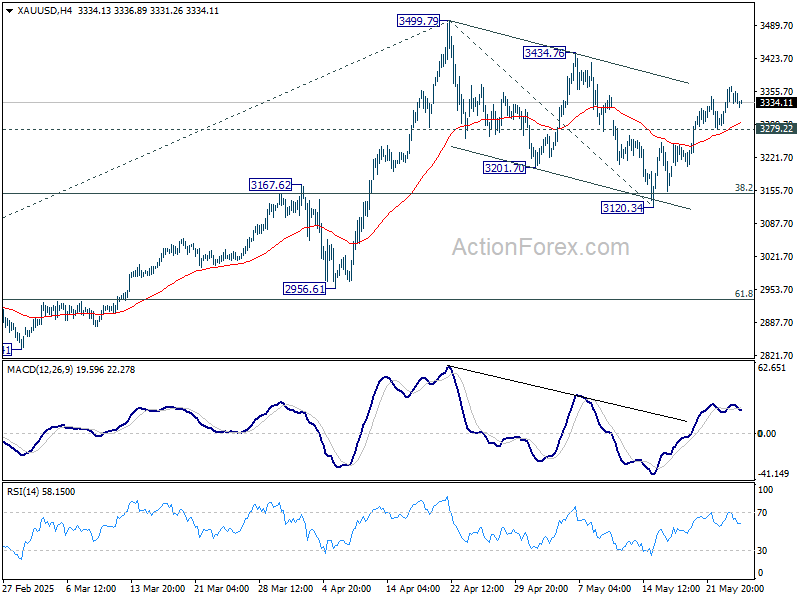

For Gold, as long as 3279.22 support holds, the bullish case for Gold still holds. That is, correction from 3499.79 should have completed with three waves down to 3120.34. Further rise should be seen to retest 3499.79 next. Firm break there will resume larger up trend. Nevertheless, break of 3279.22 will dampen this case and extend the corrective pattern with another falling leg.

In Europe, the UK is on holiday. DAX is up 1.45% at the time of writing, CAC i sup 0.97%. Germany 10-year yield is up 0.011 at 2.583. Earlier in Asia, Nikkei rose 1.00%. Hong Kong HSI fell -1.35%. China Shanghai SSE fell -0.05%. Singapore Strait Times fell -0.18%. Japan 10-year JGB yield fell -0.052 to 1.496.

Fed Kashkari: Uncertainty to delay policy at least until September

Minneapolis Fed President Neel Kashkari warned today that major shifts in US trade policies are clouding the outlook for monetary policy, making it difficult for the Fed to move on interest rates before September.

While “anything is possible,” Kashkari said in an interview with Bloomberg TV, he’s unsure whether the picture will be “clear enough” by then. Much hinges, he added, on whether trade negotiations between the US and its partners yield concrete deals in the coming months, which could “provide a lot of the clarity we are looking for.”

The uncertainty, Kashkari explained, is weighing on economic activity. He emphasized the stagflationary nature of the tariff shock, noting that its impact will depend on both the scale and duration of the levies.

On financial markets, Kashkari acknowledged that rising US Treasury yields might reflect a broader reassessment by global investors about the risks of holding American assets. He suggested that the current bond market reaction could signal a new global paradigm.

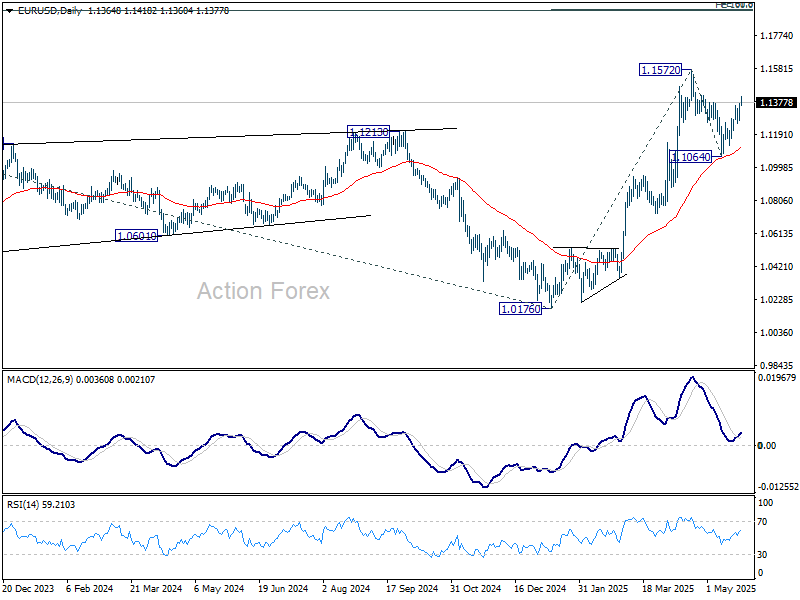

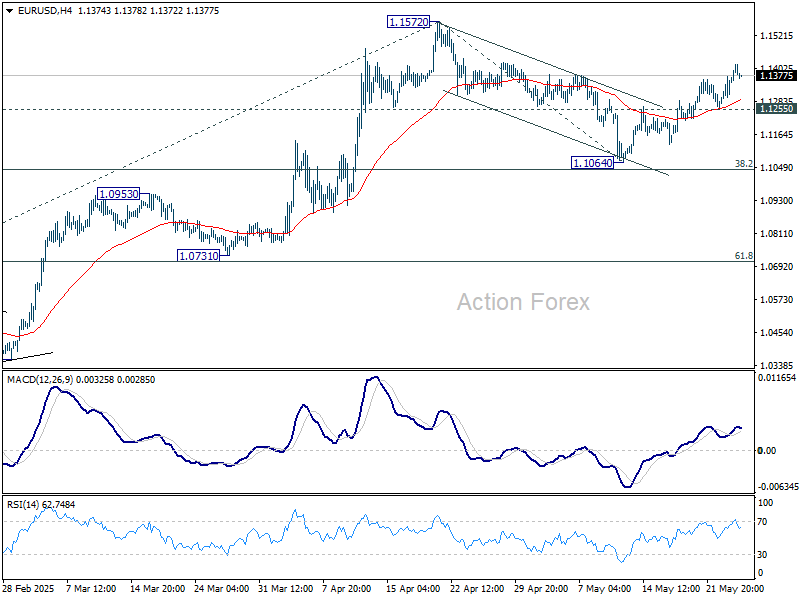

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1303; (P) 1.1339; (R1) 1.1402; More…

Intraday bias in EUR/USD remains on the upside for the moment. Correction from 1.1572 should have completed at 1.1064. Further rise should be seen to retest 1.1572 first. Decisive break there will resume larger up trend to 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. On the downside, below 1.1255 minor support will turn intraday bias neutral, and probably extend the corrective pattern with another falling leg.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0858) holds.