Dollar Recovery Slows Ahead of FOMC Minutes as Market Seeks Clarity – Action Forex

Dollar’s near-term rebound is still intact as markets head into US session. But appears to be fading as traders await fresh catalysts. While the greenback has benefited from stabilizing sentiment, there’s a lack of conviction behind the move, particularly with no data releases of note today. Markets are now turning their attention to the upcoming FOMC minutes, though expectations for a clear policy signal remain low.

The minutes from the May 6–7 FOMC meeting are expected to show a divided Fed grappling with increased volatility and an unpredictable policy backdrop, largely stemming from trade tensions. A key point of debate within the Fed may have been how to respond if elevated tariffs return and remain in place. While some officials may view tariff-driven inflation as transitory and argue for policy support to counteract the drag on growth, others may be more concerned about a shift in inflation expectations and the risk of persistent price pressures. Despite those differences, there is likely consensus around two core ideas: that tariffs are inherently stagflationary, and that it’s too early to commit to rate adjustments amid current uncertainty.

As a result, today’s release is unlikely to shift the market narrative in a meaningful way. Trading may remain subdued unless there’s an unexpected shift in tone or language around inflation risks or rate sensitivity. With Fed still firmly in a no-hurry, data-dependent mode, the market may continue to drift until the next major inflation print or employment report.

Looking across the broader currency markets, Dollar remains the week’s strongest performer so far. Kiwi follows as second, receiving a boost after RBNZ delivered a 25bps rate cut with a surprising dissent. Euro also finds modest support, ranking third on the performance board. In contrast, Yen remains the weakest major, weighed down by falling super-long JGB yields. Aussie and Swiss Franc also trail, while Sterling and Loonie remain in the middle.

Technically, Ethereum might be ready to complete the near-term triangle consolidation pattern from 2737.57. Firm break of this resistance will resume the rally from 1382.55. Next target is 61.8% projection of 1382.55 to 2737.57 from 2507.39 at 3344.79. However, break of 2507.39 support will extend the corrective pattern with another falling leg instead.

In Europe, at the time of writing, FTSE is down -0.06%. DAX is down -0.45%. CAC is down -0.13%. UK 10-year yield is up 0.012 at 4.683. Germany 10-year yield is down -0.001 at 2.541. Earlier in Asia, Nikkei closed flat. Hong Kong HSI fell -0.53%. China Shanghai SSE fell -0.02%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield rose 0.052 to 1.518.

ECB survey shows short-term inflation expectations climb as growth outlook worsens

ECB’s latest Consumer Expectations Survey for April showed a modest but notable uptick in short-term inflation expectations.

Median expectations for inflation over the next 12 months rose to 3.1%, the highest since February 2024. However, medium- and long-term inflation expectations remained steady, with the three-year outlook unchanged at 2.5% and the five-year projection holding at 2.1% for the fifth straight month.

Alongside the rise in short-term inflation forecasts, the survey revealed an increase in uncertainty about inflation over the coming year, matching levels last seen in June 2024.

More concerning, however, is the deepening pessimism around growth and employment. Expectations for economic growth over the next 12 months dropped sharply to -1.9% from -1.2% in March. Expected unemployment ticked up slightly from 10.4% to 10.5%.

RBNZ cuts OCR to 3.25%, one member favors holding steady

RBNZ lowered the Official Cash Rate by 25 basis points to 3.25%, in line with market expectations. The decision was not unanimous, passed by a 5-1 vote.

The central bank emphasized that inflation is now within the target band and is “well placed” to respond to both domestic and international developments.

Meeting minutes revealed that some committee members favored holding the rate steady at 3.50%, citing a desire to monitor elevated global uncertainty and potential inflation risks stemming from recent tariff increases.

Maintaining the OCR, they argued, could have helped anchor inflation expectations more firmly around the 2% midpoint.

In its accompanying Monetary Policy Statement, RBNZ revised down its rate path projections slightly. The OCR is now expected to fall to 3.12% by September 2025 (previously 3.23%), and to 2.87% by June 2026 (previously 3.10%).

Australia’s monthly CPI unchanged 2.4%, core inflation edges higher

Australia’s monthly CPI held steady at 2.4% yoy in April, slightly above expectations of 2.3% yoy, marking the third consecutive month of unchanged headline inflation.

However, underlying inflation measures moved higher, with CPI excluding volatile items and holiday travel rising to 2.8% yoy from 2.6% yoy. Trimmed mean CPI also tickd up from 2.7% yoy to 2.8% yoy.

These developments suggest that while headline inflation appears stable, price pressures beneath the surface remain persistent.

Key contributors to the annual inflation rate included food and non-alcoholic beverages (+3.1%), recreation and culture (+3.6%), and housing (+2.2%).

BoJ’s Ueda highlights focus on short- and medium-term rates

BoJ Governor Kazuo Ueda told parliament today that shifts in short- and medium-term interest rates have a more pronounced impact on economic activity than movements in super-long yields.

He explained that corporate and household debt is more concentrated in those shorter maturities, making the economy more sensitive to changes in that segment of the yield curve.

However, Ueda also acknowledged the spillover effects of volatility in super-long bond yields, noting that sharp moves in that part of the curve can ripple through to shorter maturities and influence overall financial conditions.

“We’ll carefully watch market developments and their impact on the economy, he emphasized.

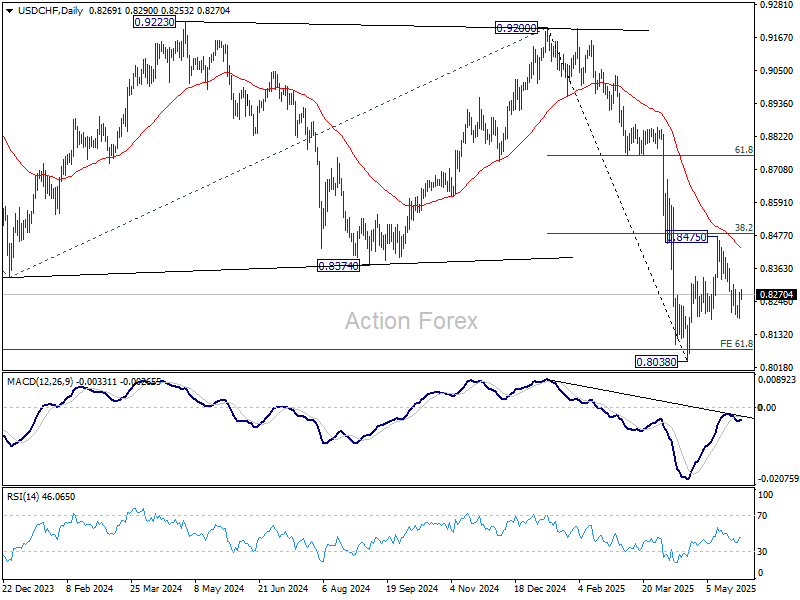

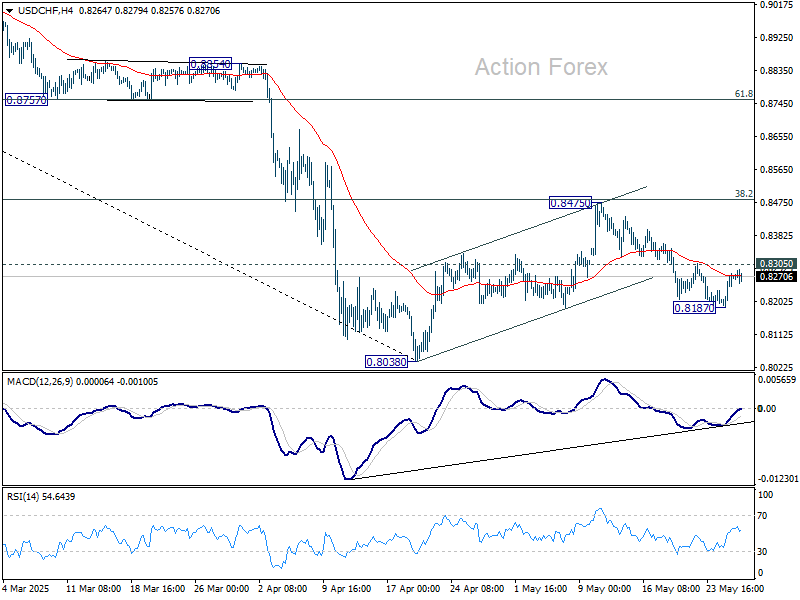

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8214; (P) 0.8247; (R1) 0.8306; More….

Range trading continues in USD/CHF and intraday bias stays neutral. Another fall is in favor as long as 0.8305 minor resistance holds. Below 0.8187 will target a retest on 0.8038 low first. Firm break there will resume larger down trend. Nevertheless, sustained break of 0.8305 will argue that pullback from 0.8475 has completed, and turn bias back to the upside to extend the pattern from 0.8038 with another rising leg.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8713) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.