Dollar Surges as US Court Strikes Down Trump’s Reciprocal Tariffs; Risk Appetite Rebounds – Action Forex

Dollar’s rebound gather extra momentum today, after the US Court of International Trade struck down President Donald Trump’s sweeping reciprocal tariffs, giving markets a fresh catalyst. The court ruled that the reciprocal tariffs imposed in April across multiple countries under claims of correcting trade imbalances exceeded presidential authority under the International Emergency Economic Powers Act. The decision marks a significant legal blow to Trump’s aggressive trade agenda.

In a strongly worded decision, the three-judge panel concluded that the “Worldwide and Retaliatory Tariff Orders exceed any authority granted to the President by IEEPA to regulate importation by means of tariffs.” The ruling also invalidated separate tariffs targeting Canada, Mexico, and China under the pretext of combating drug trafficking, stating those measures lacked a direct link to the threats cited. However, tariffs on specific items like steel and aluminum remain unaffected, as they were justified under different statutes not challenged in this case.

The Trump administration has ten days to comply with the ruling, though it has already filed an appeal to the US. Court of Appeals for the Federal Circuit. While the immediate legal outcome remains uncertain, markets responded decisively to the court’s move.

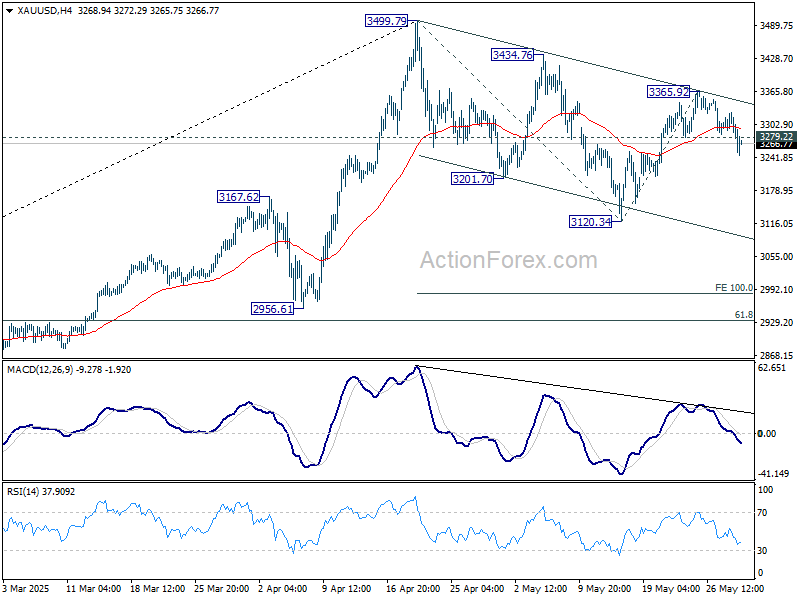

The decision sparked a broad risk-on reaction in financial markets, with DOW futures jumping over 500 points and Asian equities advancing, led by gains in Japan. Gold, which had been buoyed by safe-haven flows in recent sessions, fell below the 3250 level as investor sentiment improved. Nevertheless, 10-year Treasury yield remained steady around 4.5%, suggesting that bond markets are taking a more measured view, likely awaiting further clarity from the appeal process and ongoing trade negotiations.

Dollar dominated currency markets, emerging as the clear outperformer of the day. It was followed by the Aussie and Loonie, both benefiting from the upbeat mood. At the bottom end, Yen is staying at the bottom, while Swiss Franc and Euro also softened. Kiwi and Sterling are positing in the middle.

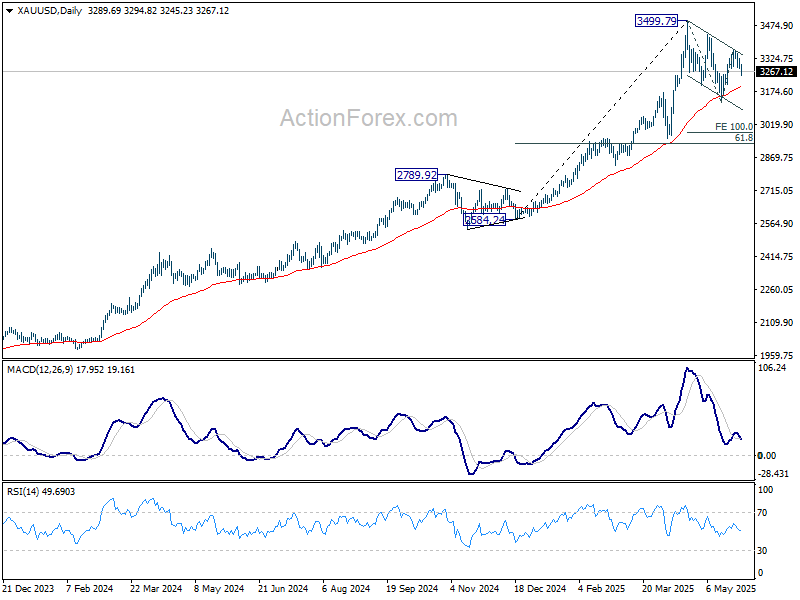

Technically, Gold’s break of 3279.22 support suggests that rebound from 3120.34 has already completed at 3365.92. Corrective pattern from 3499.79 should have started another falling leg. Deeper decline should be seen to 55 D EMA (now at 3190.95) first. Strong rebound from there will keep the pattern from 3499.79 a sideway one. However, sustained break of the 55 D EMA will open up deeper fall through 3120.34 to 100% projection of 3449.79 to 3120.34 from 3365.92 at 2980.47, which is slightly below 3000 psychological level.

In Asia, at the time of writing, Nikkei is up 1.79%. Hong Kong HSI is up 1.07%. China Shanghai SSE is up 0.72%. Singapore Strait Times is down -0.30%. Japan 10-year JGB yield is up 0.003 at 1.521. Overnight, DOW fell -0.58%. S&P 500 fell -0.56%. NASDAQ fell -0.51%. 10-year yield rose 0.043 to 4.477.

Looking ahead, the European calendar is empty with Switzerland, France and Germany on holiday. Later in the day, US will release GDP revision, jobless claims and pending home sales.

RBNZ’s Hawkesby: OCR in neutral zone, July cut not a done deal

RBNZ Governor Christian Hawkesby told Bloomberg TV today that another rate cut at the July meeting is “not a done deal” and “not something that’s programmed.”

With the OCR at 3.25% after this week’s reduction, it’s now sitting within the estimated neutral range of 2.5% to 3.5%. Hawkesby emphasized the central bank has entered a phase of “considered steps,” guided closely by incoming data rather than a preset easing path.

He acknowledged rising uncertainty, noting that near-term growth headwinds have intensified and both demand and inflation pressures are weaker than they were back in February. He also highlighted the uncertainty surrounding global trade policy, particularly tariff developments, which could play out in various ways.

NZ ANZ business confidence falls to 36.6, supporting case for further RBNZ easing

New Zealand’s ANZ Business Confidence index dropped sharply in May, falling from 49.3 to 36.6. Own Activity Outlook, a key indicator of firms’ expectations for their own performance, declined to 34.8 from 47.7.

Profit expectations also plunged to 11.1, indicating mounting pressure on margins. Although cost and wage expectations eased slightly, they remain elevated, while inflation expectations edged up from 2.65% to 2.71%.

According to ANZ, the survey paints a mixed picture: the economy is in recovery mode, but businesses continue to face tough operating conditions, particularly in passing on cost increases. The data reinforces the view that RBNZ can afford to support growth through further rate cuts, barring any major inflation or data surprises.

ANZ expects the OCR to eventually fall to 2.5%, as global headwinds and domestic fragilities persist.

FOMC minutes reveal deepening concerns over persistent inflation and trade-led slowdown

The FOMC minutes from the May 6–7 meeting highlighted growing anxiety among policymakers about the dual threat of persistent inflation and deteriorating growth prospects, largely stemming from US trade policies.

Nearly all participants flagged the risk that inflation could be “more persistent than expected” as the economy adjusts to elevated import tariffs. This situation, they warned, could force the Fed into “difficult tradeoffs” if inflation stays stubborn while growth and employment begin to falter.

The Committee agreed that uncertainty surrounding the economic outlook had “increased further”, justifying a cautious stance on monetary policy, “until the net economic effects of the array of changes to government policies become clearer.”

Fed staff revised their GDP projections lower for 2025 and 2026, citing a larger-than-anticipated drag from recent tariff announcements. Beyond the short-term impact, officials also warned of longer-term structural effects, with trade restrictions likely to slow productivity growth and reduce the economy’s potential “over the next few years.”

The labor market outlook has also darkened, with staff forecasting the unemployment rate to rise above its “natural rate” by year-end and remain elevated through 2027.

Inflation forecast was revised higher, with tariffs seen boosting prices notably in 2025, before gradually easing. Inflation is still expected to return to 2% by 2027, but the path there is now more complicated.

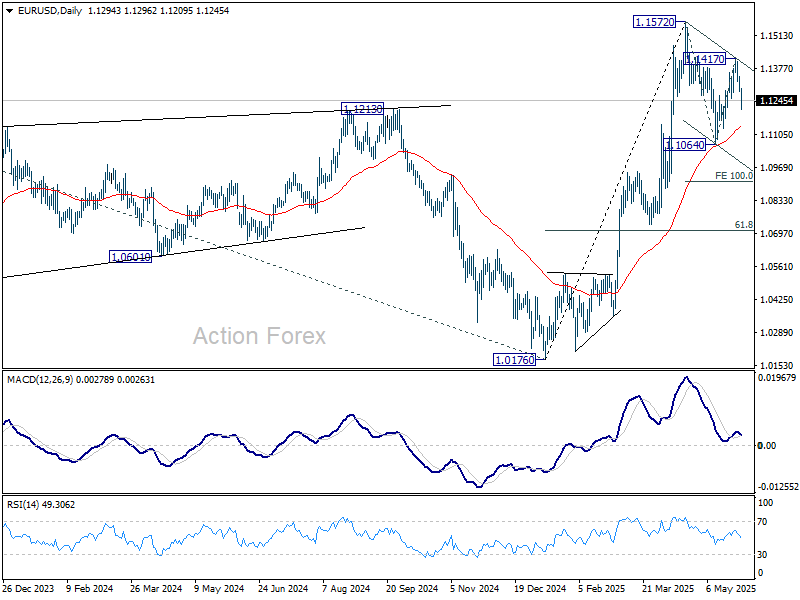

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1268; (P) 1.1307; (R1) 1.1329; More…

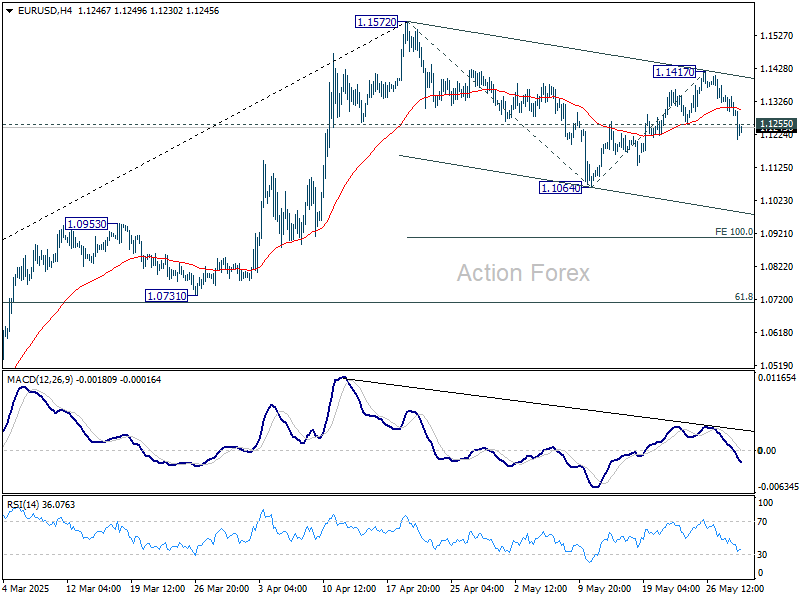

EUR/USD’s break of 1.1255 support suggests that rebound 1.1064 has completed at 1.1417. Corrective pattern from 1.1572 is now extending with another falling leg. Intraday bias is back on the downside for 1.1064 first. Break there will target 100% projection of 1.1572 to 1.1064 from 1.1417 at 1.0909. For now, risk will stay on the downside as long as 1.1417 resistance holds, in case of recovery.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 55 W EMA (now at 1.0858) holds.