Trade Rhetoric Sours Sentiment Again as US-China Tensions Resurface – Action Forex

Market sentiment took another bearish turn today following renewed rhetoric from US President Donald Trump, who accused China of having “totally violated” its preliminary trade agreement with the U.S. The comments, delivered via social media, were echoed by Trade Representative Jamieson Greer in a CNBC interview, where he expressed concern over China’s delayed compliance. Greer emphasized that while the US had fulfilled its commitments under the temporary trade deal, China was “slow rolling” its response—raising fears that tensions between the two economic powers may be re-escalating.

These remarks followed comments from Treasury Secretary Scott Bessent just a day earlier, who admitted that US-China trade talks were “a bit stalled,” though he hinted at possible high-level engagement in the coming weeks. However, the combined messaging from senior officials now points to growing frustration in Washington, increasing the risk of a renewed tariff cycle. That’s something the markets are highly sensitive to, especially with ongoing legal uncertainty surrounding the court-blocked reciprocal tariffs and their pending appeal.

On the macro front, the US April core PCE price index ticked down to 2.5% year-on-year, reaffirming that disinflation is progressing, albeit slowly. With inflation trending lower but global uncertainty mounting, Fed is widely expected to hold rates steady in the near term. Fed funds futures currently price in a 95% chance of a hold at the June FOMC meeting and a 73% chance of another hold in July. The soft inflation reading does little to shift the central bank’s cautious stance, especially as trade risks remain firmly in focus.

In the currency markets, Dollar is heading into the final house of the trading week as the strongest performer, followed by Swiss Franc and Euro. On the weaker end, Aussie struggles at the bottom, trailed by Yen and Loonie. Kiwi and Sterling are holding in the middle. However, with sentiment remaining fragile and trade headlines still in play, positioning could shift quickly before the weekly close.

In Europe, at the time of writing, FTSE is up 0.55%. DAX is up 0.72%. CAC is up 0.09%. UK 10-year yield is up 0.21 at 4.672. Germany 10-year yield is up 0.019 at 2.529. Earlier in Asia, Nikkei fell -1.22%. Hong Kong HSI fell -1.20%. China Shanghai SSE fell -0.47%. Singapore Strait Times fell -0.57%. Japan 10-year JGB yield fell -0.015 to 1.505.

US core PCE inflation cools to 2.5%, income surges

US headline PCE price index rose 0.1% mom in April, in line with expectations, while annual inflation slipped from 2.3% yoy to 2.1% yoy, below the consensus of 2.2%.

Core PCE, Fed’s preferred inflation gauge, also rose 0.1% mom and slowed from 2.6% yoy to 2.5% yoy, matching expectations. The data supports the view that disinflation remains intact, though the pace of moderation remains modest.

At the same time, personal income data surprised to the upside, jumping 0.8% mom or USD 210.1B, well above the expected 0.3% mom. Personal spending rose a more modest 0.2% mom, matching forecasts.

Canada GDP expands 0.1% mom in March, another 0.1% mom in April

Canada’s GDP grew by 0.1% mom in March, in line with market expectations. Strength in goods-producing industries continued to support overall output. The sector expanded by 0.2%, marking its second lead contribution in the past three months.

Services-producing industries also edged higher by 0.1%. In total, 9 out of 20 sectors posted growth.

Looking ahead, preliminary data from Statistics Canada suggests another 0.1% increase in real GDP for April.

ECB’s Panetta signals diminished room for further rate cuts

Italian ECB Governing Council member Fabio Panetta said today that while the central bank has made meaningful progress in easing monetary policy, bringing the deposit rate down from 4% to 2.25%, “the room for further rate cuts has naturally diminished”.

“However, the economic outlook remains weak, and trade tensions could lead to a deterioration,” he added. “It will be essential to maintain a pragmatic and flexible approach, considering liquidity conditions and the signals coming from financial and credit markets.”

Panetta also highlighted the high-stakes nature of ongoing trade talks between the EU and the US, warning that even tensions are likely to have a “significant impact” on the region’s economy.

BoE’s Taylor: Global headwinds justify lower monetary policy path

BoE MPC member Alan Taylor reinforced his dovish position in an interview with the Financial Times, highlighting growing downside risks to the UK economy from global developments.

Taylor, who alongside Swati Dhingra voted for a larger 50bps rate cut in May, argued that monetary policy should be on a “lower policy path” given the accumulating headwinds.

He specifically pointed to impact of Trump’s tariffs on imports would “be building up over the rest of this year in terms of trade diversion and drag on growth”.

While UK inflation unexpectedly jumped to 3.5% in April, Taylor downplayed the significance of the rise, attributing it to “one-time tax and administered price changes.”

Swiss KOF rises to 98.5, but growth outlook remains subdued

Switzerland’s KOF Economic Barometer edged up to 98.5 in May from 97.1, marking a modest improvement in economic sentiment. While the uptick is a positive signal, the barometer remains below its long-term average, suggesting that the broader outlook for the Swiss economy “remains subdued”.

According to the KOF, the manufacturing sector showed notable strength, contributing to the overall improvement. However, indicators tied to foreign demand and private consumption remain under pressure, highlighting the ongoing drag from weak external conditions and cautious domestic spending.

Japan’s industrial production falls -0.9% mom in April, but May rebound expected

Japan’s industrial production fell by -0.9% mom in April, a milder decline than the expected -1.4%. The Ministry of Economy, Trade and Industry maintained its view that production “fluctuates indecisively,” reflecting ongoing uncertainty, particularly around global trade developments.

While the ministry said the impact of US tariffs was limited in April, some firms have voiced concern about the manufacturing outlook as policy risks persist.

The breakdown of the data shows a mixed picture: six of 15 industrial sectors saw declines, including production machinery, fabricated metals, and transport equipment excluding motor vehicles. However, eight sectors recorded gains, with electronic parts and business-oriented machinery showing notable strength.

Manufacturers surveyed expect a sharp 9.0% rebound in May, followed by a -3.4% dip in June.

Also released, Japan’s retail sales grew by a stronger-than-expected 3.3% yoy in April, outpacing the consensus of 2.9% yoy. Meanwhile, the unemployment rate remained steady at 2.5%.

Tokyo core inflation accelerates to 3.6%, driven by food and services costs

Tokyo’s core CPI (excluding fresh food) accelerated to 3.6% yoy in May, up from 3.4% yoy and above market expectations of 3.5% yoy, marking the fastest pace since January 2023. This marks the third consecutive year that core inflation has exceeded the Bank of Japan’s 2% target.

While headline CPI ticked down slightly from 3.5% yoy to 3.4% yoy, the underlying core-core measure (excluding food and energy) also edged up fro 2.0% yoy to 2.1% yoy, suggesting broad-based inflation persistence.

The surge in non-fresh food prices, up 6.9% yoy, remains a dominant driver—highlighted by a staggering 93.2% yoy jump in rice prices.

Another notable development is the uptick in services inflation, which climbed to 2.2% yoy from 2.0% yoy , indicating that businesses are beginning to pass on higher labor costs.

Australia retail sales down -0.1% mom in April, weighed by weak clothing demand

Australia’s retail sales turnover unexpectedly declined by -0.1% mom in April, missing expectations for a 0.3% mom rise. On an annual basis, sales were up 3.8% compared to April 2024/

The Australian Bureau of Statistics noted that the decline was driven primarily by reduced spending on clothing. The weakness was partly offset by a rebound in Queensland, where businesses recovered from disruptions caused by ex-Tropical Cyclone Alfred in March.

RBNZ’s Silk: Data to guide timing and need for further cuts

RBNZ Assistant Governor Karen Silk said that interest rates are currently within the estimated neutral band of 2.5% to 3.5%.

She noted that the full impact of previous easing has yet to filter through the economy, making any future adjustments highly dependent on incoming data.

The OCR track indicates “whatever we do is going to be data-dependent, and then we will be looking to the data to help us to decide when or if we cut further from here,” she added.

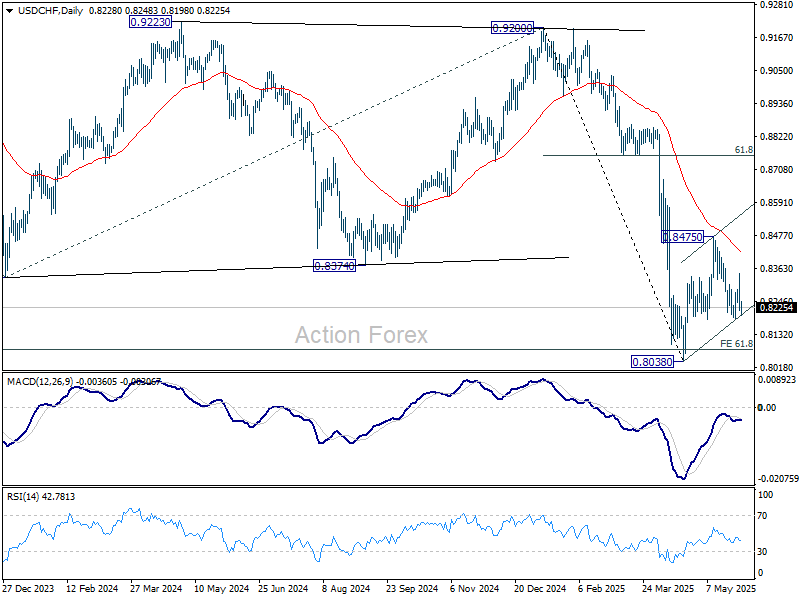

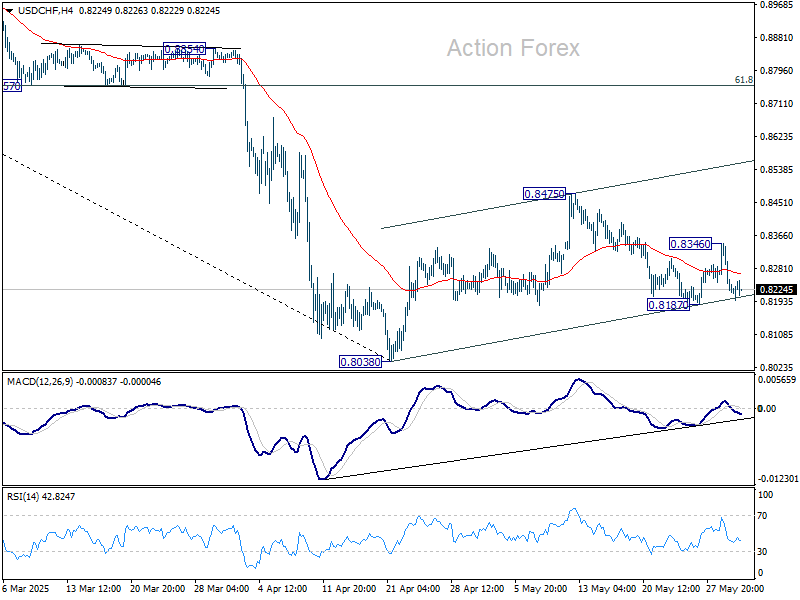

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8182; (P) 0.8265; (R1) 0.8312; More….

Range trading continues in USD/CHF and intraday bias stays neutral. On the downside, break of 0.8187 will resume the fall from 0.8475 to retest 0.8038 low. On the upside, above 0.8346 will bring stronger rise to 0.8475. Firm break there will extend the corrective pattern from 0.8038 with another rising leg.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8713) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.