Subdued Markets Drift as Tariff Tensions Resurface and BoC Decision Looms – Action Forex

Global markets remain subdued as investors struggle to find a firm direction. US stocks closed higher overnight, with NASDAQ extending to fresh multi-week highs, suggesting some resilience in tech-led risk appetite. Asian equities followed suit to some extent, but the overall momentum has been tepid.

In the currency markets, Dollar is attempting to recover from recent losses, though the rebound so far lacks strong conviction. Loonie and Kiwi are mildly firmer. However, Aussie and Yen are both underperforming, sitting at the bottom of the performance table and highlighting the absence of a coherent risk-on or risk-off narrative. European majors are positioned in the middle of the pack, with Swiss Franc slightly outperforming.

The trade backdrop remains tense. US President Donald Trump’s decision to double tariffs on most imported steel and aluminum to 50% took effect on today, marking a new escalation in the global trade conflict. According to economic adviser Kevin Hassett, the initial 25% steel tariffs delivered partial support, but “more help is needed,” hence the decision to double the rates. The move came just as the White House also demanded “best offers” from trade partners ahead of a self-imposed early July deadline. Attention now turns to the European Union, with markets awaiting any formal response or retaliatory measures.

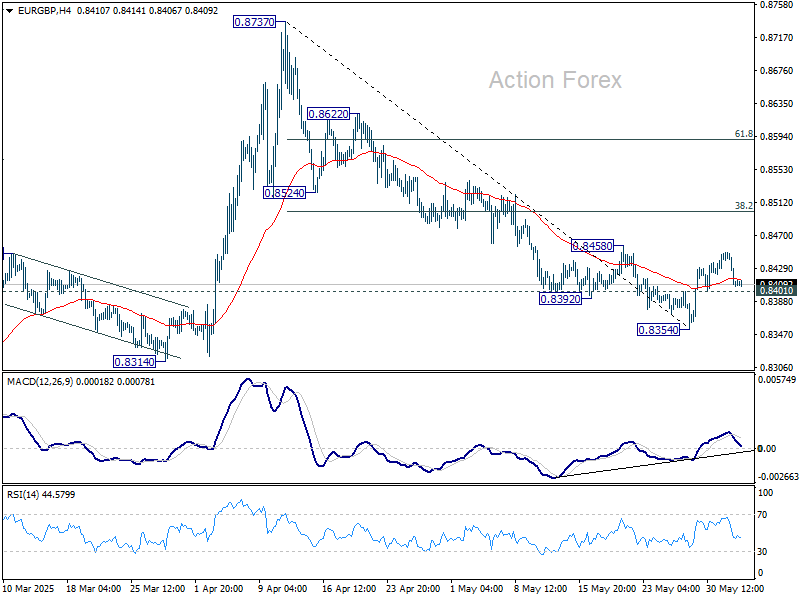

Technically, EUR/GBP’s recovery has stalled ahead of 0.8458 resistance and retreated notably. Focus is back on 0.8401 support. Firm break there will argue that fall from 0.8737 might be ready to resume through 0.8354. That, if happens, might be accompanied by extended pullback in EUR/USD or upside break out in GBP/USD, or both.

In Asia, at the time of writing, Nikkei is up 0.92%. Hong Kong HSI is up 0.47%. China Shanghai SSE is up 0.36%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is up 0.014 at 1.495. Overnight, DOW rose 0.51%. S&P 500 rose 0.58%. NASDAQ rose 0.81%. 10-year yield fell -0.002 to 4.460.

Looking ahead, final PMI Services data from both the Eurozone and the UK will be released in European session. In the US, markets will closely watch the ADP employment report and ISM services index for clues on labor market momentum and service sector resilience. Still, the day’s main event is BoC policy decision, where the central bank is widely expected to hold, but guidance could lean dovish as trade risks intensify.

BoC to hold rates at 2.75%, maintain dovish bias

BoC is widely expected to leave interest rate unchanged at 2.75% for the second consecutive meeting today.

While Q1 GDP surprised to the upside at 2.2% annualized, the growth was heavily front-loaded by export activity as US buyers rushed to stockpile Canadian goods ahead of impending tariffs. That one-off boost is unlikely to alter the central bank’s cautious stance in light of growing global and domestic uncertainties. Meanwhile, core inflation rose back to near the top of BoC’s 1-3% target range, offering a reasonable basis for a continued pause.

Overall, expectations are firmly anchored toward further easing later this year. A Reuters poll found that 75% (17 of 23) of economists anticipate at least two more cuts in 2025, with two of them forecasting as many as four.

Given the high degree of trade uncertainty, particularly around tariffs, BoC is likely to keep a flexible tone in its communication. While the rate is on hold today, policymakers are expected to leave the door open for adjustments ahead, depending on how the trade situation evolves.

In the currently markets, today’s BoC decision may not be the key driver for USD/CAD. Instead, market direction is still largely dictated by sentiment around US trade policy.

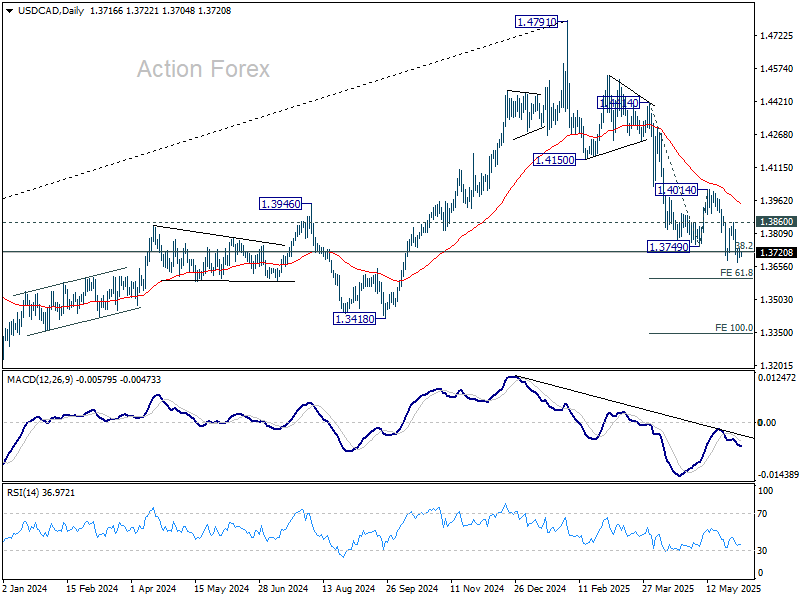

Technically, further decline is expected as long as 1.3860 resistance holds, to 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603. There might be some support from 1.3603 to contain downside and bring a rebound, as a correction to the five wave decline from 1.4791 high. However, decisive break there could prompt downside acceleration to 100% projection at 1.3349 rather quickly.

Australia’s GDP grows only 0.2% qoq in Q1, as weather and public investment drag

Australia’s GDP expanded just 0.2% qoq in Q1, falling short of expectations for 0.4% qoq growth. On an annual basis, GDP rose 1.3% yoy. However, GDP per capita declined by -0.2% qoq, marking a renewed contraction in individual economic output.

The ABS noted that severe weather disrupted key sectors including mining, tourism, and shipping, while also impacting domestic demand and exports.

The most notable drag came from public investment, which fell -2.0%, contributing to the largest negative impact from public spending since Q3 2017. Net exports also weighed slightly, subtracting -0.1 percentage points from quarterly growth.

Japan’s PMI composite finalized at 50.2, growth momentum falters

Japan’s private sector lost steam in May as final PMI Services reading slipped to 51.0 from April’s 52.4, while Composite PMI declined to 50.2 from 51.2. The data point to only marginal growth in overall activity, with a slowdown in services combining with a mild deterioration in manufacturing output.

S&P Global’s Annabel Fiddes noted that the rise in total new orders “moved closer to stagnation, as service sector sales grew at their slowest pace in six months and factory demand continued to decline. This moderation suggests that Japan’s private sector “may struggle to bounce back in the near-term”.

Underlying concerns were linked to external and structural factors, including an uncertain global demand outlook, persistent labor shortages, and mounting cost pressures.

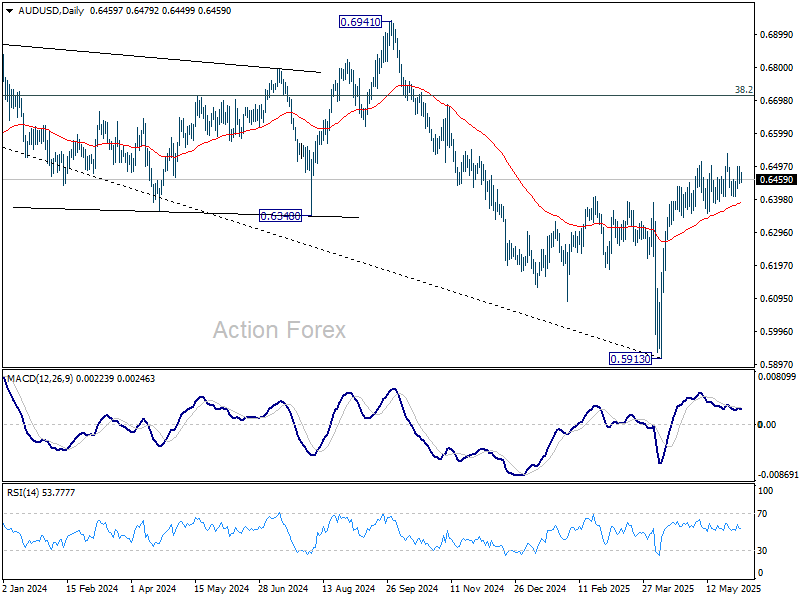

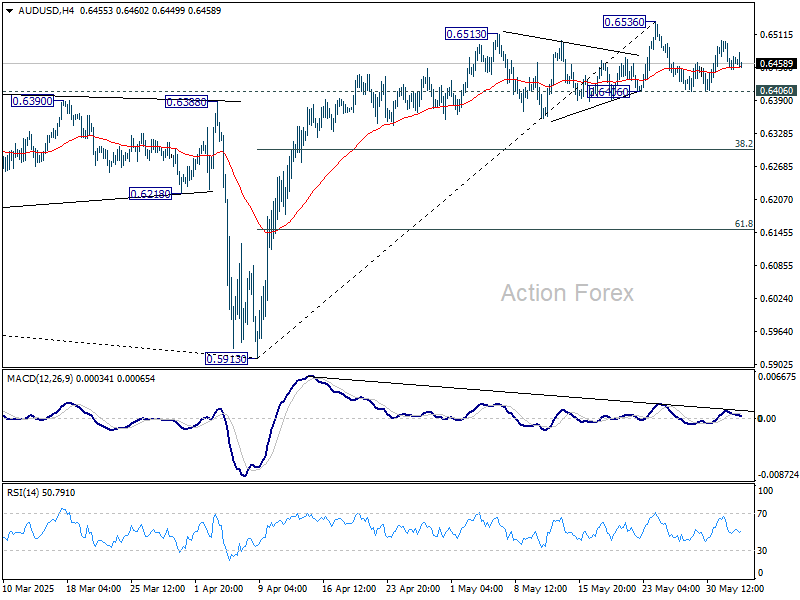

AUD/USD Daily Report

Daily Pivots: (S1) 0.6439; (P) 0.6470; (R1) 0.6492; More...

Intraday bias sin AUD/USD remains neutral for the moment. With 0.6406 support intact, further rally is expected. ON the upside, firm break of 0.6536 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, decisive break of 0.6406 will confirm short term topping, and turn bias back to the downside for 38.2% retracement of 0.5913 to 0.6536 at 0.6298.

In the bigger picture, AUD/USD is still struggling to sustain above 55 W EMA (now at 0.6441) cleanly, and outlook is mixed. Sustained trading above 55 W EMA will indicate that rise from 0.5913 is at least correcting the down trend from 0.8006 (2021 high), with risk of trend reversal. Further rise should be seen to 38.2% retracement of 0.8006 to 0.5913 at 0.6713. However, rejection by 55 W EMA will revive medium term bearishness for another fail through 0.5913 at a later stage.