Dollar Rebounds as NFP and Wages Beat Forecasts, Tariff Impact Yet to Materialize – Action Forex

Dollar staged a firm comeback today following slightly better-than-expected non-farm payroll figures, with job growth at 139k and wage growth coming in strong at 0.4% mom. While not a blowout report, the data was enough to alleviate immediate concerns of a sharp labor market slowdown. Stock futures also advanced, suggesting that investors are reassessing the near-term risks from tariffs and focusing instead on the resilience in headline economic indicators.

Despite ongoing caution over the economic toll of US trade policy, particularly with the expiration of the 90-day tariff truce looming in July, the effects haven’t yet registered decisively in labor markets. In fact, the stronger-than-expected wage growth might reinforce some Fed officials’ inflation concerns, supporting the market consensus that the next rate cut, if any, is unlikely before September.

Outside of the US, Loonie is also showing strength, underpinned by solid domestic jobs data. Aussie and Kiwi are mildly firmer too, buoyed by broader risk appetite. Meanwhile, safe havens are under pressure, with Yen and Swiss Franc the weakest of the day as investors rotate into higher-yielding and risk-correlated assets. Euro and Sterling are softer, but holding within familiar ranges.

In Europe, at the time of writing, FTSE is up 0.10%. DAX is down -0.15%. CAC is up 0.14%. UK 10-year yield is up 0.03 at 4.656. Germany 10-year yield is down -0.11 at 2.573. Earlier in Asia, Nikkei rose 0.50%. Hong Kong HSI fell -0.48%. China Shanghai SSE rose 0.04%. Japan 10-year JGB yield fell -0.002 to 1.459.

US NFP grows 139k in May, unemployment rate steady at 4.2%

US non-farm payroll employment rose 139k in May, above expectation of 130k. That’s slightly below average monthly gain of 149k over the prior 12 months.

Unemployment rate was unchanged at 4.2%, matched expectations. Participation rate fell from 62.6% to 62.4%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings have increased by 3.9% yoy.

Canada’s employment grow 8.8k in May, unemployment rate rises to 7%

Canada’s employment grew 8.8k in May, better than expectation of -11.9k fall. Growth in full-time employment (+58k; +0.3%) was offset by a decline in part-time work (-49k; -1.3%).

Unemployment rate rose from 6.9% to 7.0%, matched expectations. Employment rate held steady at 60.8%.

Average hourly wages among employees increased 3.4% you, same as in April.

ECB officials signal pause yesterday’s rate cut, emphasize flexibility

One day after ECB delivered its eighth rate cut in this easing cycle, a coordinated message emerged from several Governing Council members: ECB is not committing to further immediate action.

Latvian central banker Martins Kazaks was particularly blunt, stating that markets should not expect a rate cut at every meeting. He emphasized the value of preserving “policy space”.

“We don’t get much data between now and the July meeting so it may well be the case that we pause,” Kazaks said. “But uncertainty remains very high, the political situation may change every day. So forward guidance isn’t your friend in these circumstances.”

Greek central bank chief Yannis Stournaras echoed this sentiment, calling ECB’s work on inflation “nearly done,” while warning that further cuts would require growth to fall short of current forecasts.

Estonian Governor Madis Muller also struck a cautious tone, suggesting the rate-cutting cycle may be “almost finished,” but acknowledged that visibility is limited. All three policymakers stressed that decisions ahead would remain data-driven, and that it was too early to rule out any scenario.

French Governor François Villeroy de Galhau and Lithuania’s Gediminas Šimkus declared victory over inflation. However, both underlined the importance of maintaining flexibility in the face of mounting global uncertainty. Villeroy also reassured that “We have tools to react if there’s deflation.”

Eurozone retail sales inch up 0.1% mom April, mixed national trends

Eurozone retail sales rose just 0.1% mom in April, falling short of expectations for a 0.2% mom rise. Modest gains in food, drink, and tobacco sales (+0.5%) and a solid rebound in automotive fuel purchases (+1.3%) were offset by a -0.3% decline in non-food product sales.

Across the EU, retail sales rose a more robust 0.7% mom, but the underlying data painted a sharply divided picture. Poland led with a remarkable 7.5% surge, followed by Slovakia and Sweden at 2.4%. In contrast, Germany—the region’s largest economy—saw a -1.1% drop, dragging on the overall Eurozone figure.

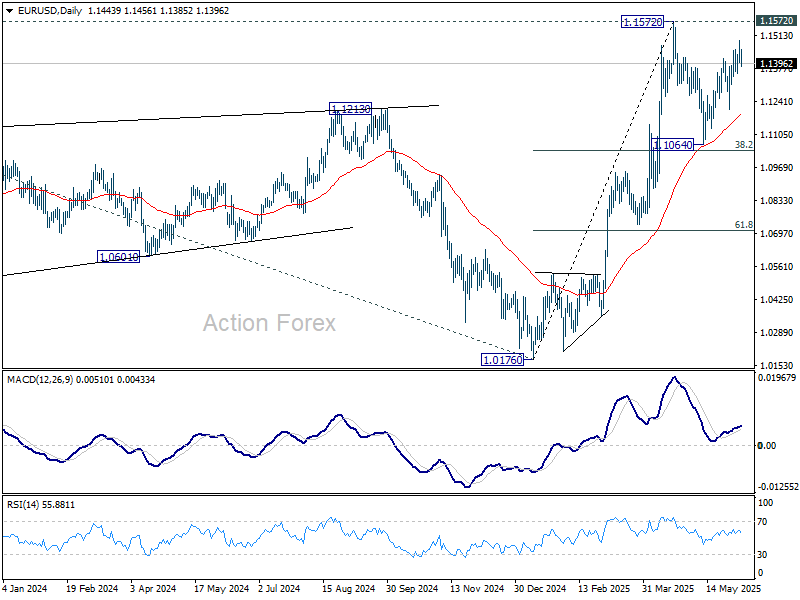

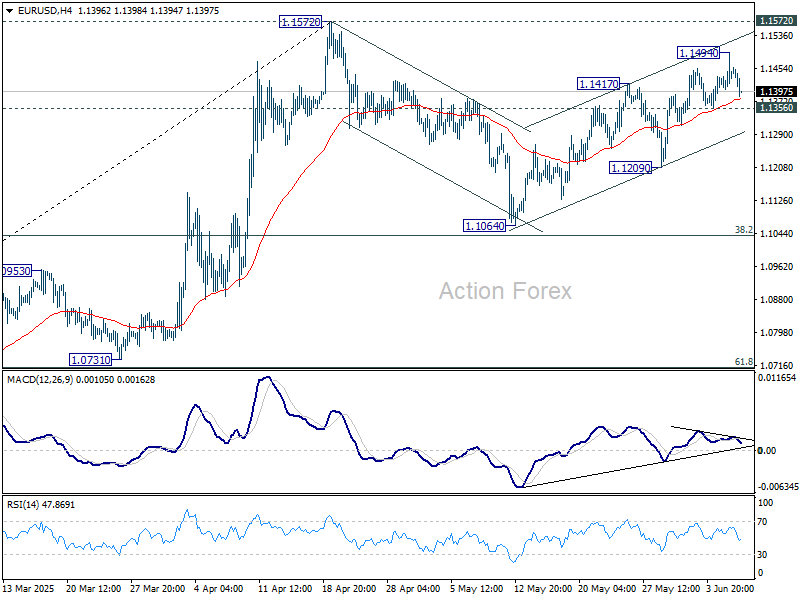

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1401; (P) 1.1448; (R1) 1.1491; More…

Intraday bias in EUR/USD is turned neutral with current retreat. While another rise might be seen, strong resistance could emerge from 1.1572 to limit upside, at least on first attempt. On the downside, break of 1.1356 support will indicate that the corrective pattern from 1.1572 might have started the third leg, and target 1.1209 support for confirmation.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.