Fragile Trade Progress and CPI Ahead Keep Risk Appetite in Check – Action Forex

Asian equities edged modestly higher on Wednesday, lifted by the announcement that US and Chinese officials reached a “framework” to implement the Geneva trade consensus and advance commitments made in the latest Trump-Xi phone call. While officials from both sides struck an optimistic tone, the agreement remains preliminary, lacking substantive details on thornier issues.

US Commerce Secretary Howard Lutnick confirmed that the deal would still require presidential approval on both sides before moving forward. One of the key elements of the framework involves China’s rare-earth exports, a pivotal issue as the US seeks to stabilize supply chains. Lutnick said the US expects export restrictions to be eased, with reciprocal rollback of recent US technology export bans to China.

However, the broader market reaction was muted. The US Court of Appeals allowed Trump’s contested tariffs to remain in place pending further legal review, undermining hopes of swift tariff rollback. The ruling enables the continued enforcement of “Liberation Day” tariffs, which apply to imports from major partners. This legal backdrop, coupled with still-fragile diplomatic progress, reinforces the market’s caution.

In the currency markets, the overall tone is mixed, with Swiss Franc and Dollar leading as the day’s strongest performers so far, followed by Loonie. On the other end, risk-sensitive currencies Kiwi and Aussie are softer, alongside Sterling. Euro and Yen are positioning in the middle of the pack. Despite modest equity gains, this is far from a full-fledged risk-on environment.

Attention now shifts to two major US events: US CPI report and 10-year Treasury note auction. The inflation data will serve as a critical barometer for how much of the tariff impact is bleeding into consumer prices. Simultaneously, the Treasury auction will test investor appetite for government debt amid lingering concerns over deficits, erratic trade policies, and rising issuance needs.

In Asia, at the time of writing, Nikkei is up 0.50%. Hong Kong HSI is up 0.92%. China Shanghai SSE is up 0.55%. Singapore Strait Times is down -0.51%. Japan 10-year JGB yield is down -0.017 at 1.463. Overnight, DOW rose 0.25%. S&P 500 rose 0.55%. NASDAQ rose 0.63%. 10-year yield fell -0.008 to 4.474.

Inflation data and treasury auction pose twin tests for US Bond Market

Two major events in the US are closely watched today. The May CPI report and the USD 39B 10-year Treasury auction converge to test sentiment in the bond market.

The May CPI will offer the clearest signal yet of whether tariffs are beginning to filter through to consumer prices. Economists expect a 0.2% mom gain, with annual headline inflation accelerating to 2.5%. Core CPI, is projected to rise 0.3% mom and accelerate to 2.9% yoy.

While today’s CPI reading will provide an initial glimpse, the real acceleration in prices may come in June as tariffs ripple through supply chains. The unpredictability of Trump’s trade strategy, frequent shifts between escalation and truce, could delay the impact but increasing its persistence. Fed’s challenge is not only identifying if inflation is returning, but determining whether it’s sticky enough to warrant policy action beyond holding rates steady.

Meanwhile, the 10-year Treasury auction will act as a referendum on fiscal credibility. With swelling deficits, an uncertain trade outlook, and ballooning spending commitments—including the administration’s touted “big, beautiful” infrastructure and defense budgets—investors will be watching bid-to-cover ratios and indirect bidder participation for signs of strain. A weak auction could rekindle fears of waning demand for US debt, driving yields higher and possibly stoking volatility across asset classes.

Technically, the 10-year yield has remained within a broad range since peaking at 4.997 in 2023. While it spiked to 4.629% in May following Moody’s downgrade of the US credit rating, the move was limited and quickly retraced. As long as the 4.809 resistance level caps upside attempts, the bond market appears relatively calm—though not immune to future shocks.

Japan’s CGPI cools to 3.2% in May, but food inflation continue to rise

Japan’s corporate goods price index slowed more than expected in May, easing from 4.1% to 3.2% yoy, versus the anticipated 3.5% yoy. The decline reflects the broader disinflationary trend in upstream prices, aided by the recent rebound in Yen. Yen-based import price index plunged -10.3% yoy, a sharper drop than April’s -7.3% yoy.

Falling raw material costs were evident across sectors, with steel prices down -4.8% yoy, chemicals -3.1% yoy, and non-ferrous metals -2.1% yoy

However, consumer-related categories showed more persistence in inflation. Prices of food and beverages accelerated to 4.2% yoy from April’s 4.0% yoy, suggesting that inflationary stickiness in essential goods remains a challenge despite broader producer-side cooling.

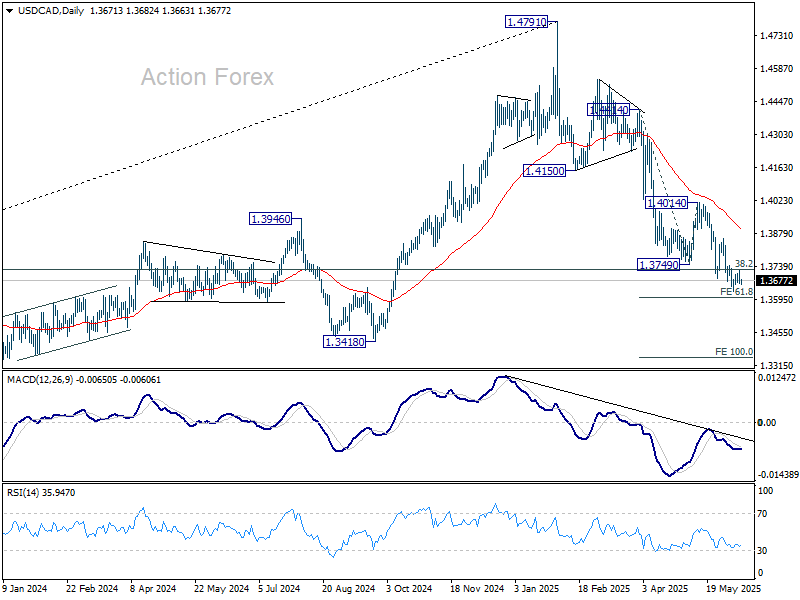

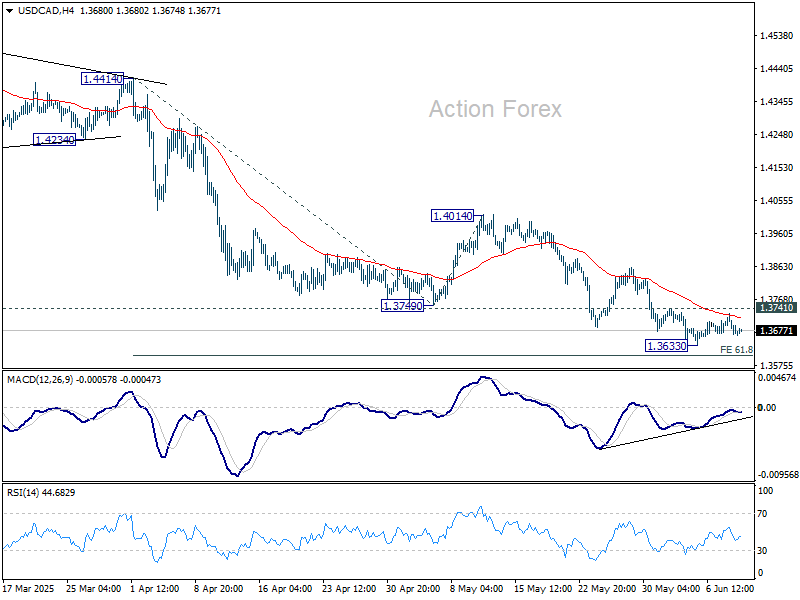

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3650; (P) 1.3689; (R1) 1.3711; More…

Intraday bias in USD/CAD remains neutral at this point. Considering bullish convergence condition in 4H MACD, firm break of 1.3741 will indicate short term bottoming at 1.3633. Intraday bias will turn back to the upside for stronger rebound to 1.4014 resistance, as a correction to fall from 1.4791. Nevertheless, decisive break of 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603 will pave the way to 100% projection at 1.3349.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.