BoJ Doubts Offsets Strong CPI as Yen Tumbles – Action Forex

Despite an upside surprise in Japan’s core inflation data, Yen extended its decline across the board today. While CPI ex-food rose 3.7% yoy in May, much of the gain was driven by an outsized 100%+ surge in rice prices, which alone contributed nearly half of the index’s increase. This jump, widely seen as transitory due to supply issues, is expected to ease in the autumn, limiting its significance for monetary policy.

More importantly, the minutes from the BoJ’s May meeting revealed a central bank growing more cautious. One policymaker acknowledged that “the likelihood of realizing the outlook…was not as high as before,” while others emphasized the need to weigh both upside and downside risks amid extreme global uncertainty. With that tone, hopes for another rate hike this year are fading fast.

Adding to the caution is the ongoing threat of US-Japan trade friction. If Tokyo fails to secure exemptions from rising tariffs—especially on autos and steel—the economic drag could deepen into late 2025, further weakening the case for policy tightening. That reinforces a narrative of prolonged BoJ patience, even amid sticky inflation.

On the currency performance board, Yen sits firmly at the bottom for the week, joined by Loonie and Swiss Franc. In contrast, Aussie and Kiwi lead the pack, with the Dollar holding firm—for now—alongside them. Euro and Pound trade in the middle of the spectrum. However, Dollar strength looks increasingly fragile heading into the Friday close.

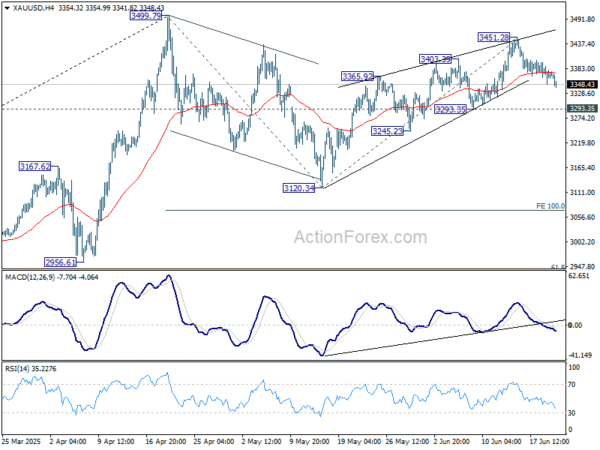

Technically, Gold’s extended retreat suggests that rebound from 3120.34 might have completed at 3451.28 already. Corrective pattern from 3499.79 high could already be in its third leg. On the downside, firm break of 3293.53 support will solidify this case, and target 3120.34 support and possibly below.

In Asia, at the time of writing, Nikkei is up 0.06%. Hong Kong HSI is up 1.03%. China Shanghai SSE is up 0.14%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield is up 0.001 at 1.413.

UK retail sales plunge -2.7% mom in May, led by sharp drop in food spending

UK retail sales volumes slumped -2.7% mom in May, far worse than expectations of a -0.5% decline, marking the steepest monthly fall since December 2023.

The downturn was driven by a sharp -5.0% mom drop in food store sales, reversing April’s 4.7% mom gain and registering the largest fall in this category since May 2021. Non-food store sales also retreated, down -1.4% mom on the month, as department and household-related purchases weakened amid cautious consumer sentiment.

Despite May’s setback, retail sales volumes rose by 0.8% in the three months to May compared to the prior three-month period ending February.

BoJ minutes reflect extremely high uncertainties, stresses need to judge without preconceptions

BoJ’s May policy meeting minutes reveal a board wary of “extremely high uncertainties” stemming from global trade tensions. While BoJ left its short-term interest rate unchanged at 0.5%, it sharply downgraded its growth and inflation outlooks, largely due to the expected hit on Japan’s economy from higher US tariffs.

Members reiterated that “if the outlook for economic activity and prices was realized,” further rate hikes would still be appropriate, aligning with gradual normalization. However, A key theme was the need to remain flexible and data-dependent, with many members emphasizing the importance of “carefully examining” the evolving outlook before acting.

Many members warned that it was crucial “to judge whether the outlook… would be realized, without any preconceptions.” One policymaker admitted that the probability of the forecast materializing was “not as high as before,” while another stressed that both upward and downward risks must be weighed.

The minutes also captured divergent internal views. One board member said that “while the Bank would enter a phase of pausing,” policy must remain “nimble and more flexible.” Another warned of the risk that simultaneous supply-chain disruptions and inflation spikes would leave Japan in a difficult position, especially given that “inflation expectations were not as anchored as in the United States.”

Japan’s CPI core jumps to 3.7% as rice prices more than double

Japan’s core consumer inflation (ex-fresh food) accelerated from 3.5% yoy to 3.7% yoy in May, beating expectations of 3.6% yoy and marking the fastest pace since January 2023. The gain was driven by soaring rice costs, which jumped over 100% amid supply shortages. The core-core inflation measure, excluding both fresh food and energy, also quickened to 3.3% yoy from 3.0% yoy, reflecting broadening price pressures.

While the headline CPI edged down slightly from 3.6% yoy to 3.5% yoy, underlying inflation trends continue to exceed BoJ’s 2% target, where they have remained since April 2022.

Also Service prices rose 1.4% yoy in May, up from 1.3% yoy in April, with dining and travel costs gaining momentum—an important sign for BoJ, which monitors this segment closely as a proxy for wage-driven inflation.

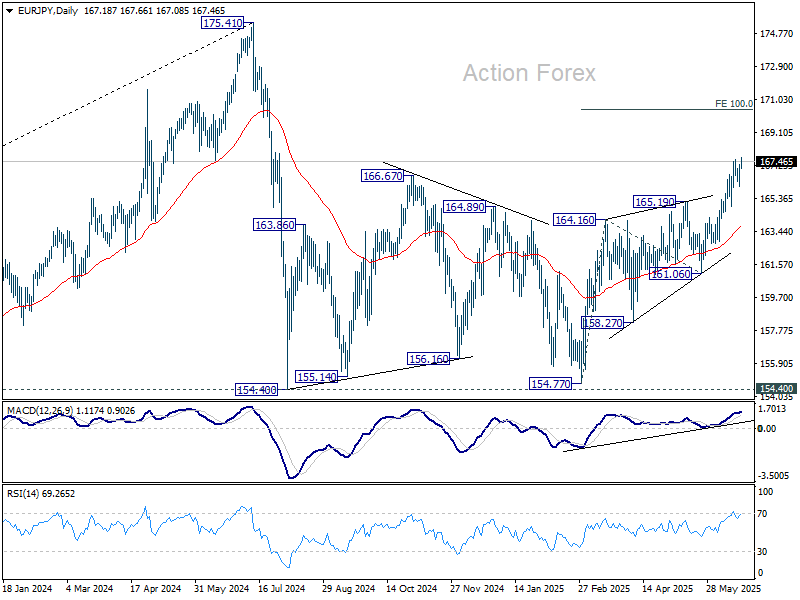

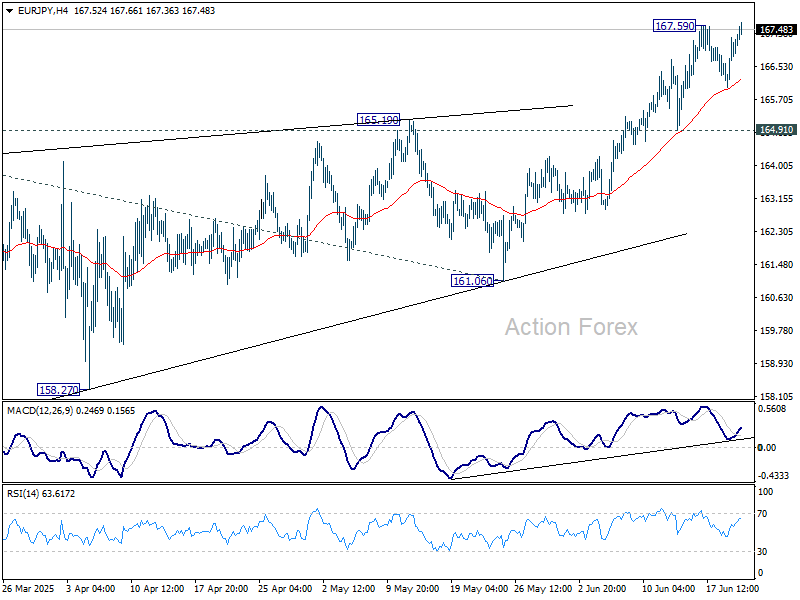

EUR/JPY Daily Outlook

Daily Pivots: (S1) 166.42; (P) 166.87; (R1) 167.70; More…

EUR/JPY rebounded strongly after drawing support from 55 4H EMA and focus is back on 167.59 resistance. Decisive break there will resume rally from 154.77. Next target is 100% projection of 154.77 to 165.19 from 161.06 at 170.45. For now, near term outlook will stay cautiously bullish as long as 164.91 support holds, even in case of another retreat.

In the bigger picture, price actions from 175.41 are seen as correction to up trend from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.