Dollar Leads, But Euro’s Structural Story Gains Momentum – Action Forex

Markets were adrift last week as traders grappled with intensifying global risks. The unresolved twin threats of a full-blown trade war and escalating Middle East conflict kept investors on the defensive. Despite some tentative diplomatic efforts, neither front showed meaningful progress, leaving equities vulnerable after months of sustained gains. With investor confidence fraying, global indexes may soon face deeper corrections.

Amid the cautious mood, Dollar took the lead, buoyed by Fed’s policy hold and slower projected easing. Yet beneath the surface, Euro is gaining traction on improving confidence in the Eurozone economy, and divergence of ECB policy and other central banks.

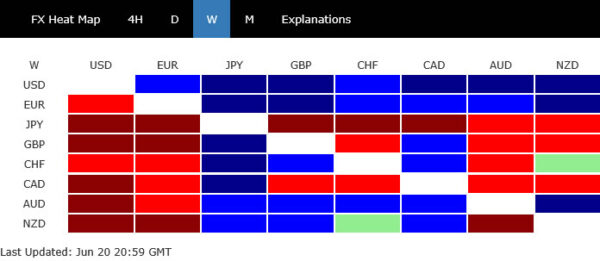

In the week’s performance table, Euro and Aussie followed the greenback near the top. At the other end, Yen underperformed the most as doubts on BoJ rate hike grew. Sterling struggled on soft UK data, while Loonie also underwhelmed. Swiss Franc and Kiwi held to the middle of the pack.

Dual Pressures of Tariff Uncertainty and Middle East Conflict Continue

Global markets struggled for direction last week, as trade and geopolitical tensions weighed heavily on investor sentiment. Despite some optimism around diplomatic overtures, the outlook remains clouded by slow-moving negotiations and unresolved flashpoints. S&P 500, like many global indices, continued to show signs of fatigue amid the rising uncertainty.

On the geopolitical side, the highly anticipated meeting in Geneva between European foreign ministers and Iran’s Abbas Araqchi yielded little progress. Iran reiterated its refusal to negotiate under threat and demanded that Israel cease its attacks and face accountability. While Tehran expressed openness to discussing uranium enrichment limits, it drew a firm red line against a full ban.

The fragile optimism quickly also faded as Israel and Iran exchanged fresh missile attacks on Saturday. The renewed violence signals that tensions are likely to persist into the coming week and beyond. While direct US intervention remains on hold, the risk of escalation remains ever-present and continues to cast a shadow over markets.

Meanwhile, there was scant progress on the trade front. It’s reported that the EU is now pushing for a 10% reciprocal tariff framework to align with the US-UK deal, but no breakthrough has been reported. Canada’s Prime Minister Mark Carney has threatened retaliatory tariffs by late July on US steel and aluminum imports. Meanwhile, Japan canceled a key bilateral security dialogue with Washington, as disputes over defense spending and trade policy intensified. The cancellation is a symbolic setback, revealing just how strained relations have become.

The most pressing concern for markets is the ticking clock on the 90-day tariff truce. With less than three weeks remaining, there’s growing anxiety that US President Donald Trump may soon issue unilateral tariff letters to multiple trading partners. A unilateral tariff escalation could trigger sharp market reactions, especially given how sensitively investors have been pricing trade-related risk into both equities and currencies.

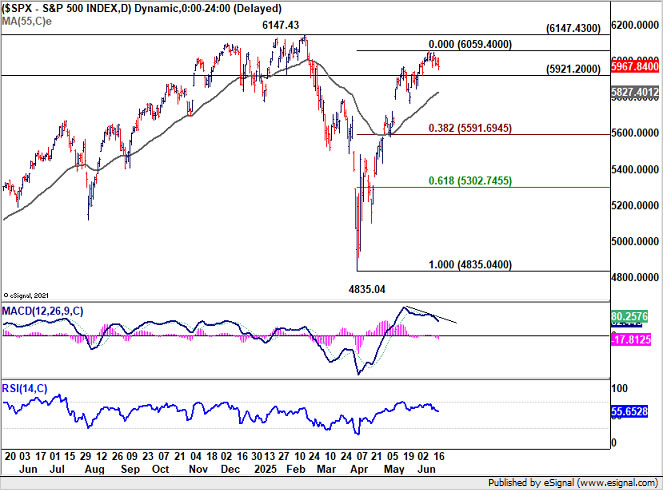

Technically, S&P 500 continued to lose upside momentum as seen in D MACD. While further rise cannot be ruled out, considering bearish divergence condition, strong resistance should emerge from 6147.43 high to limit upside. On the downside, break of 5921.20 support will be the first sign of short term topping, and bring deeper pullback to 55 D EMA (now at 5827.40). Further break there will target 38.2% retracement of 4835.04 to 6059.40 at 5991.69, with risk of near term bearish reversal.

Dollar Holds Ground on Fed Caution, While Waller Breaks Ranks

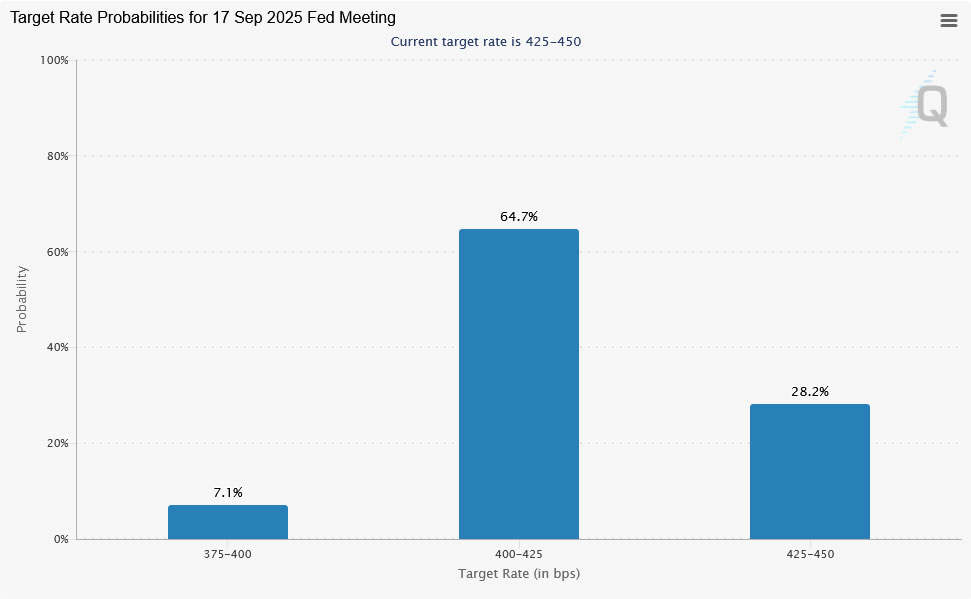

Dollar found a degree of footing last week as expectations around Fed policy injected some near-term stability. As anticipated, Fed kept its target range unchanged at 4.25–4.50%. The updated dot plot revealed a slower-than-expected easing path. While two rate cuts are still projected for 2025, the median forecast now sees just one cut per year in both 2026 and 2027, lifting the year-end federal funds rate forecasts to 3.6% and 3.4%, respectively.

Yet Fed Chair Jerome Powell was forthright in tempering the significance of these projections, saying no policymakers held their rate path “with a great deal of conviction.” The central bank’s Monetary Policy Report to Congress followed up with similar caution, noting that while tariff-induced inflation may be showing up in goods prices, it remains too early to assess the overall impact.

Nevertheless, Fed Governor Christopher Waller broke ranks slightly, floating the possibility of a rate cut as soon as July. Waller argued that the inflation impact from tariffs would likely be one-off and non-persistent. More concerning to him was the potential for labor market deterioration.

Waller’s divergence from other Fed colleagues comes at a sensitive time politically. Powell’s current term expires in May 2026, and the likelihood of Trump installing a new Fed Chair—potentially someone more aligned with his view on interest rates—is growing. Waller, a 2020 Trump appointee to Fed Board, may be in the running. While no formal shortlist has emerged, markets may grow increasingly sensitive to such succession politics in coming months.

Despite Waller’s comments, market expectations for a July cut remain subdued, with fed fund futures still assigning a nearly 90% probability to a hold. September remains the market’s favored timeline for the next move, with over 70% chance.

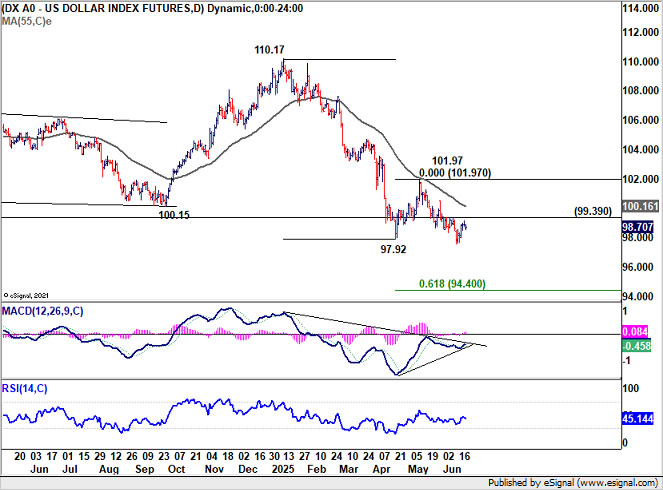

Technically, there is no clear sign of bottoming in Dollar Index yet with 99.39 resistance intact. Recent decline from 110.17 is still in favor to continue towards 61.8% projection of 110.17 to 97.92 from 101.97 at 94.40.

However, momentum could further diminish on the next fall. Selloff in Dollar is unlikely to be as one-sided as seen earlier in the year. At least, Yen would stay pressured due to diminishing hope of another BoJ rate hike this year. Commodity currencies and Sterling could be pressured if risk sentiment turned sour.

Meanwhile, firm break of 99.39 will confirm short term bottoming, and bring rebound through 55 D EMA (now at 100.16).

Euro Set to Outperform Again on Economic Optimism and Diverging Policy Paths

While the Dollar ended the week as the top performer, it’s Euro that is quietly showing greater underlying strength. EUR/USD’s late-week jump suggests the pair may soon breakout of range, with Euro outperforming the greenback again. Supporting this outlook is a clear improvement in economic sentiment, most notably in Germany, the Eurozone’s growth engine.

The June ZEW survey showed a remarkable 22.3-point jump in economic sentiment to 47.5. Current conditions improved by 10 points—the strongest rise in over a year. Growing investment and consumer demand are behind the pickup, helped by fiscal measures from the new German government. This policy mix, together with ECB’s earlier rate cuts, could finally lift Germany out of the stagnation that’s persisted for nearly three years.

Additionally, ECB’s easing cycle is certainly nearing its conclusion, possibly with just one recalibration cut remaining. That sets it apart from central banks like BoE, which is still on a “gradual and cautious” rate reduction path, and SNB, which may be forced into negative rates again. Even Fed, which has been on pause since late 2024, may soon re-join the global easing trend once tariff-driven inflation uncertainties clear.

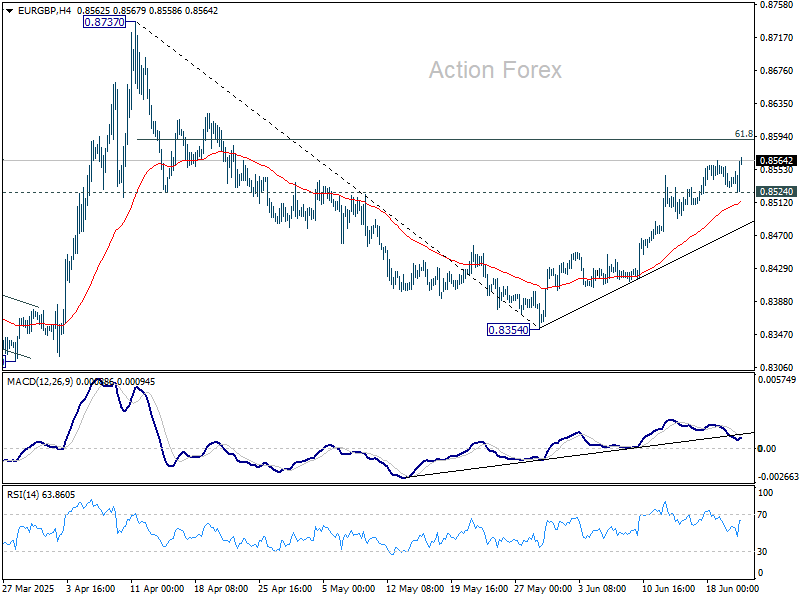

The technical picture supports Euro strength across the board too. EUR/GBP’s rebound from 0.8354 extended higher last week. Further rise is expected to 61.8% retracement of 0.8737 to 0.8354 at 0.8591. Firm break there will pave the way to 0.8373 resistance.

EUR/AUD’s late rally suggests that retreat from 1.7880 might have completed at 1.7626 already. Break of 1.7880 will target 61.8% retracement of 1.8554 to 1.7245 at 1.8054. Firm break there will pave the way to 1.8554.

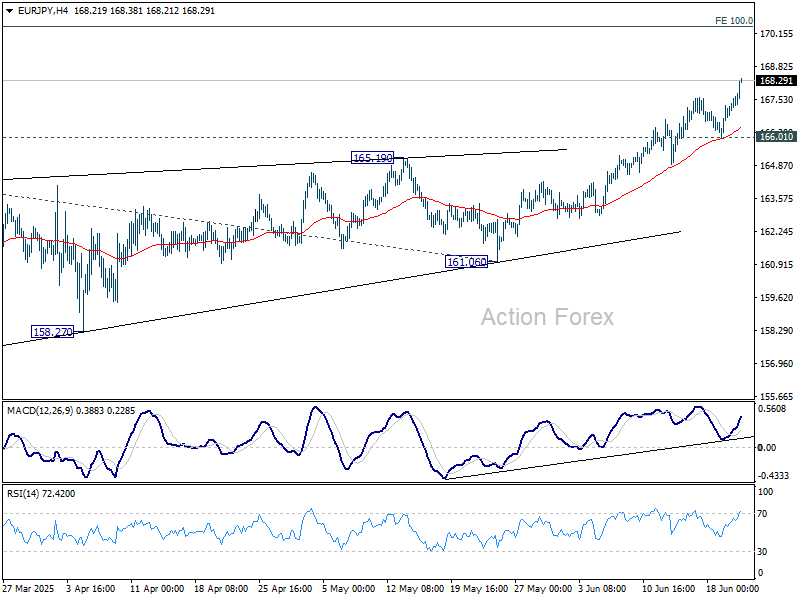

EUR/JPY’s near term rise also continued last week, and it’s on track to 100% projection of 154.77 to 164.16 from 161.06 at 170.45 next.

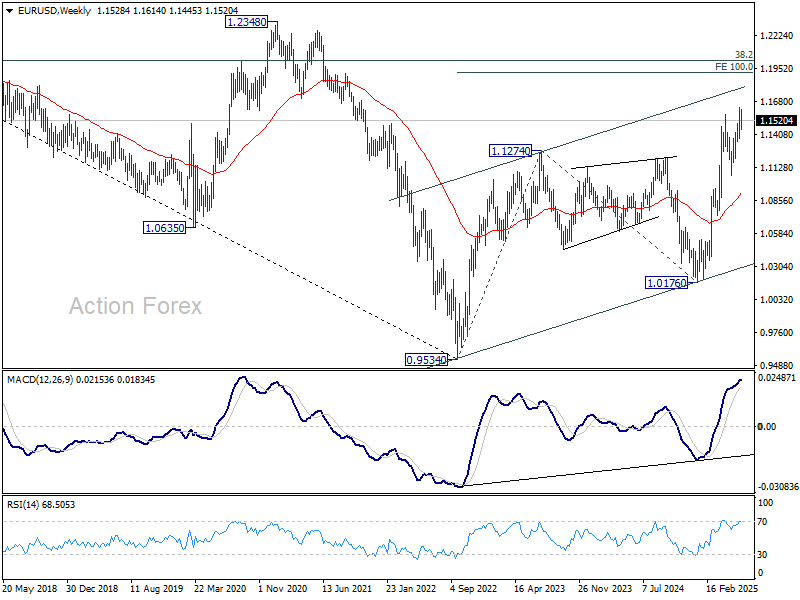

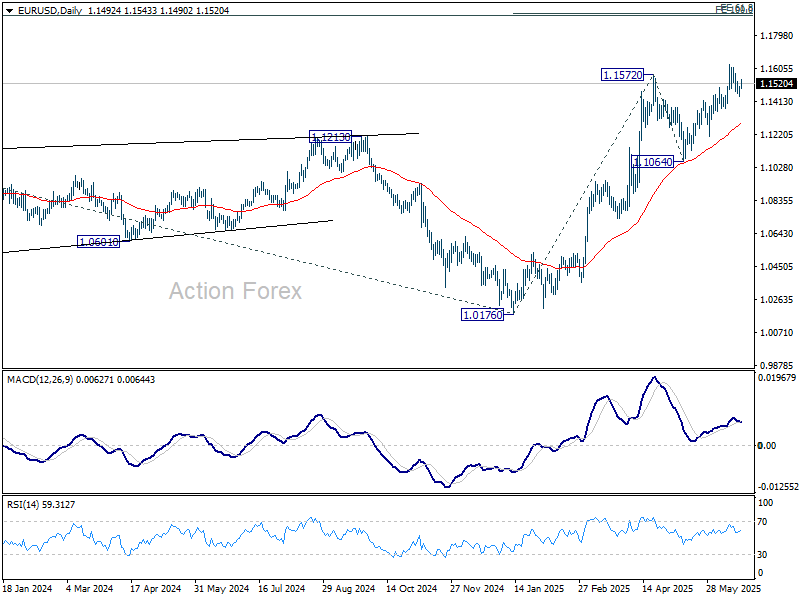

EUR/USD Weekly Outlook

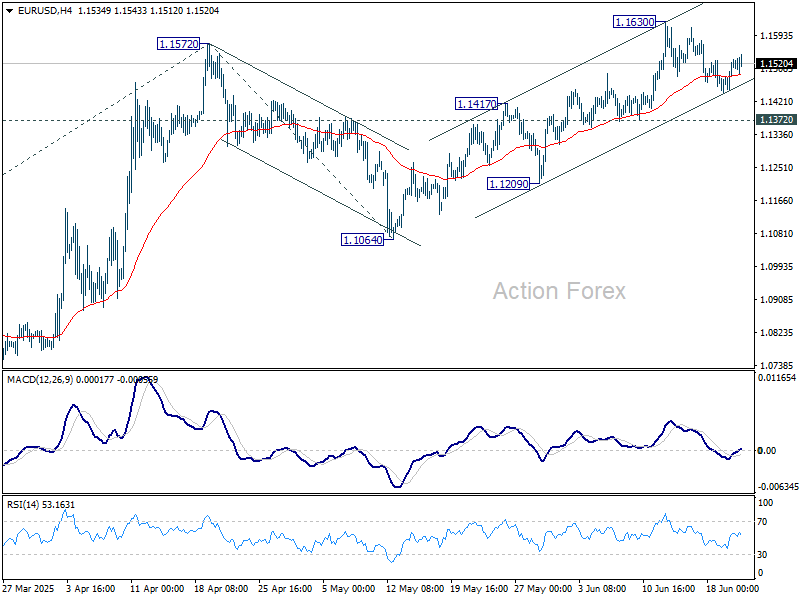

EUR/USD stayed in consolidations below 1.6300 last week and outlook is unchanged. Initial bias remains neutral this week first. Further rise is expected as long as 1.1372 support holds. Firm break of 1.1630 will resume the rise from 1.1076 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

In the long term picture, a long term bottom should be in place already at 0.9534, on bullish convergence condition in M MACD. Rise from there could be a corrective bounce or the start of an up trend. In either case, next target is 38.2% retracement of 1.6039 to 0.9534 at 1.2019.