Middle East Diplomacy Calms Nerves; Sterling Rises, Loonie Lags – Action Forex

Markets are showing tentative optimism today as signs of potential diplomatic engagement in the Middle East ease investor concerns. European foreign ministers are meeting Iran’s Abbas Araghchi in Geneva—marking the first direct discussions with Western officials since Israel’s strike on Iran last week. This also reflects the highest level of European involvement in the crisis so far, feeding hopes that tensions could de-escalate through dialogue rather than force.

Adding to the calm, the immediate threat of US military action appears to have diminished. President Donald Trump noted that he would defer his decision on whether to proceed “within the next two weeks,” citing a “substantial chance” of negotiations. That pause has helped stabilize global sentiment, at least temporarily, even as underlying geopolitical risks remain elevated.

Currency markets are reacting accordingly. Sterling is outperforming, brushing off weak retail data as risk appetite improves. Aussie and Euro are also gaining modest ground. Meanwhile, Loonie is underperforming, trailing behind Yen and Franc, both of which are also softer as safe-haven flows ease. Dollar and Kiwi are positioning in the middle.

In Europe, at the time of writing, FTSE is up 0.38%. DAX is up 1.48%. CAC is up 1.01%. UK 10-year yield is up 0.011 at 4.544. Germany 10-year yield is up 0.003 at 2.526. Earlier in Asia, Nikkei fell -0.22%. Hong Kong HSI rose 1.26%. China Shanghai SSE fell -0.07%. Singapore Strait Times fell -0.28%. Japan 10-year JGB yield fell -0.009 to 1.403.

Fed’s Waller: Should consider rate cut as early as July

Fed Governor Christopher Waller signaled openness to a rate cut as early as July, citing minimal inflation risks from U.S. tariffs and mounting concerns over the labor market.

In an interview with CNBC, Waller said, “I think we’re in the position that we could do this and as early as July,” while acknowledging it’s uncertain whether the broader committee will align with that view.

Waller emphasized the risks of delaying action, warning against waiting for a clear downturn in employment. “If you’re starting to worry about the downside risk labor market move now don’t wait,” he argued.

Regarding tariffs, Waller dismissed concerns that they would create sustained inflationary pressure, reiterating that the price effects should be limited and one-off.

“Even if the tariffs come in later, the impacts are still the same,” he said, calling for the Fed to “start thinking about cutting the policy rate at the next meeting”, after pausing the easing cycle for six months.

Canada’s retail sales rise 0.3% mom in April, but May outlook weakens on trade tensions

Canada’s retail sales rose 0.3% mom in April to CAD 70.1B, falling short of market expectations of a 0.5% mom rise. Growth was supported by increases in six of nine subsectors, particularly in motor vehicle and parts dealers. However, sales excluding autos and fuel—rose just 0.1% mom. In volume terms, sales rose a healthier 0.5%, but the strength may not carry forward. Statistics Canada’s advance estimate for May suggests a -1.1% mom decline.

Trade tensions between Canada and the US are emerging as a key drag on the retail sector. Statistics Canada reported that 36% of retail businesses were affected in April, citing price increases, shifting demand, and supply chain disruptions. While most subsectors recorded sales growth, all nine reported some degree of negative impact.

UK retail sales plunge -2.7% mom in May, led by sharp drop in food spending

UK retail sales volumes slumped -2.7% mom in May, far worse than expectations of a -0.5% decline, marking the steepest monthly fall since December 2023.

The downturn was driven by a sharp -5.0% mom drop in food store sales, reversing April’s 4.7% mom gain and registering the largest fall in this category since May 2021. Non-food store sales also retreated, down -1.4% mom on the month, as department and household-related purchases weakened amid cautious consumer sentiment.

Despite May’s setback, retail sales volumes rose by 0.8% in the three months to May compared to the prior three-month period ending February.

BoJ’s Ueda eyes future hikes on labor-driven inflation

BoJ Governor Kazuo Ueda said today that Japan’s underlying inflation could “stagnate” in the short term as economic growth slows. But he remains confident it will “accelerate thereafter”.

He pointed to “intensifying labor shortages” as a source of upward pressure on medium- to long-term inflation expectations.

Ueda emphasized that BoJ stands ready to hike rates further, contingent on sustained improvements in the economy.

BoJ minutes reflect extremely high uncertainties, stresses need to judge without preconceptions

BoJ’s May policy meeting minutes reveal a board wary of “extremely high uncertainties” stemming from global trade tensions. While BoJ left its short-term interest rate unchanged at 0.5%, it sharply downgraded its growth and inflation outlooks, largely due to the expected hit on Japan’s economy from higher US tariffs.

Members reiterated that “if the outlook for economic activity and prices was realized,” further rate hikes would still be appropriate, aligning with gradual normalization. However, A key theme was the need to remain flexible and data-dependent, with many members emphasizing the importance of “carefully examining” the evolving outlook before acting.

Many members warned that it was crucial “to judge whether the outlook… would be realized, without any preconceptions.” One policymaker admitted that the probability of the forecast materializing was “not as high as before,” while another stressed that both upward and downward risks must be weighed.

The minutes also captured divergent internal views. One board member said that “while the Bank would enter a phase of pausing,” policy must remain “nimble and more flexible.” Another warned of the risk that simultaneous supply-chain disruptions and inflation spikes would leave Japan in a difficult position, especially given that “inflation expectations were not as anchored as in the United States.”

Japan’s CPI core jumps to 3.7% as rice prices more than double

Japan’s core consumer inflation (ex-fresh food) accelerated from 3.5% yoy to 3.7% yoy in May, beating expectations of 3.6% yoy and marking the fastest pace since January 2023. The gain was driven by soaring rice costs, which jumped over 100% amid supply shortages. The core-core inflation measure, excluding both fresh food and energy, also quickened to 3.3% yoy from 3.0% yoy, reflecting broadening price pressures.

While the headline CPI edged down slightly from 3.6% yoy to 3.5% yoy, underlying inflation trends continue to exceed BoJ’s 2% target, where they have remained since April 2022.

Also, service prices rose 1.4% yoy in May, up from 1.3% yoy in April, with dining and travel costs gaining momentum—an important sign for BoJ, which monitors this segment closely as a proxy for wage-driven inflation.

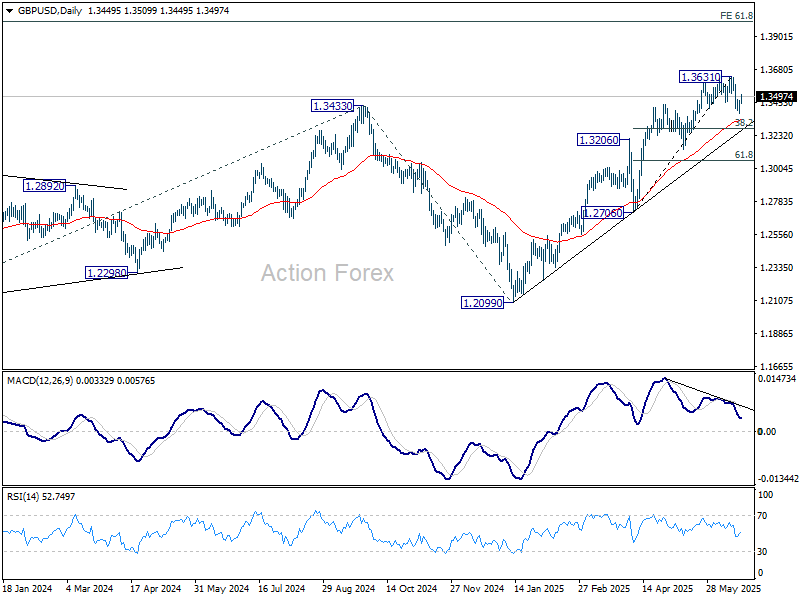

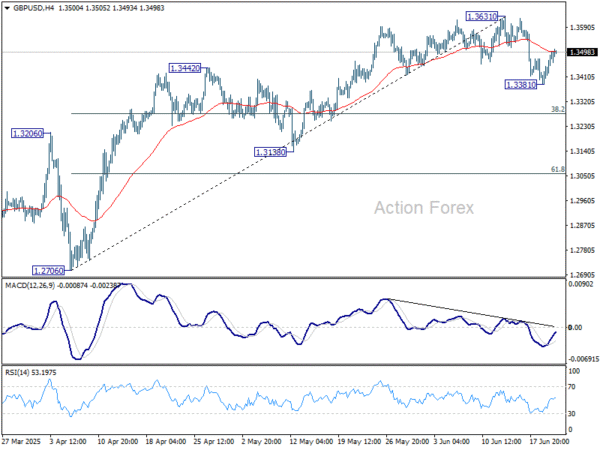

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3411; (P) 1.3440; (R1) 1.3498; More…

GBP/USD’s recovery from 1.3381 extends today, but upside is kept well below 1.3631 resistance. Intraday bias remains neutral first. Correction from 1.3631 short term top could still extend. Break of 1.3381 will bring deeper fall to 38.2% retracement of 1.2076 to 1.3631 at 1.3278. Nevertheless, firm break of 1.3631 will resume larger up trend.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2937) holds, even in case of deep pullback.