Euro Steady as EU Holds Fire After Trump’s 30% Tariff Blow – Action Forex

Risk sentiment turned mildly negative in Asia on Monday following US President Donald Trump’s announcement of 30% tariffs on imports from the EU and Mexico, starting August 1. While US futures turned lower, equity markets in Asia were more muted, digesting the move in context of still-holding EU retaliation.

The 30% tariff rate on EU goods was notably harsher than the 20% flagged during Trump’s Liberation Day speech in April. Mexico, by contrast, appears to have secured a better outcome than Canada, reflecting Washington’s preference for selective confrontation. Still, Trump’s broader campaign has swept in dozens of countries with tariff bands ranging from 20% to 50%, highlights a return to maximalist trade pressure.

Market reaction in FX was largely subdued, though defensive positioning was evident. Yen outperformed for now, followed by Dollar and Loonie. At the other end, Kiwi and Aussie weakened the most. Euro edged lower but avoided steeper losses after the EU confirmed it would delay its suspended retaliation. Sterling and Swiss Franc are positioning in the middle.

The EU’s initial response has been measured. European Commission President Ursula von der Leyen confirmed Sunday that retaliatory tariffs on EUR 21B worth of US goods—previously suspended—would remain on hold until early August. She condemned the new US action as disruptive but emphasized the EU’s commitment to diplomacy and proportionate response.

Beyond the US-EU front, the trade shock comes amid parallel developments. Von der Leyen announced a political agreement with Indonesia to move forward on a long-stalled free trade deal, signaling that the EU is actively diversifying trade partnerships. While this helps hedge against US hostility, it’s unlikely to blunt short-term disruption. Unless trade talks regain traction, investors may need to brace for more volatility heading into August’s tariff deadline.

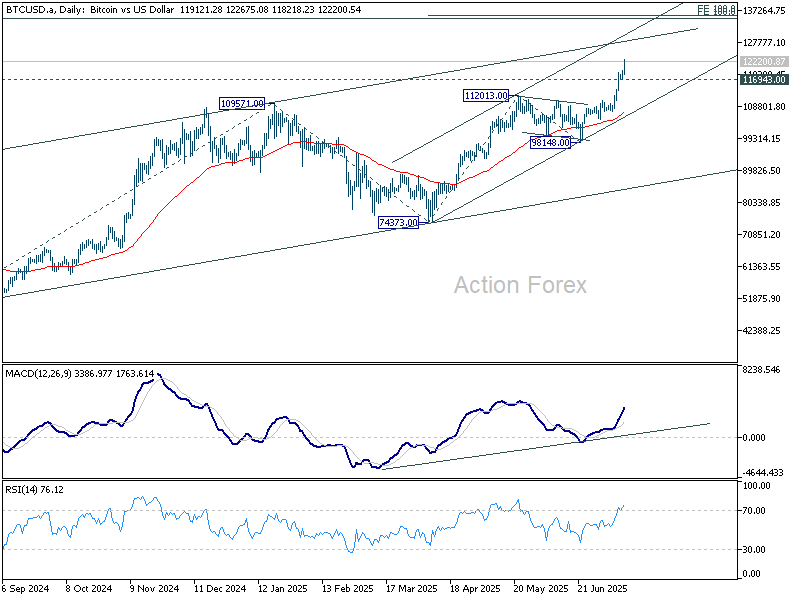

Technically, Bitcoin’s record run continues today and surges through 120k mark. Near term outlook will stay bullish as long as 116943 support holds. Next target is double projection level at around 135k, 100% projection of 49008 to 109571 from 74373 at 134946 and 100% projection of 74373 to 112013 from 98148 at 135788. Overbought condition will likely cap Bitcoin’s upside there.

In Asia, at the time of writing, Nikkei is flat. Hong Kong HSI is up 0.15%. China Shanghai SSE is up 0.33%. Singapore Strait Times is up 0.36%. Japan 10-year JGB yield is up 0.068 at 1.574.

NZ BNZ services rises to 47.3, but outlook remains grim

New Zealand’s services sector showed mild improvement in June, with BusinessNZ Performance of Services Index rising to 47.3 from May’s 44.1. Despite the gain, the index remains well below its long-run average of 52.9 and firmly in contraction territory. Subcomponents showed modest upticks—new orders rose from 43.4 to 48.8, employment edged up from 47.1 to 47.4, and activity/sales climbed to 44.5. Inventories just breached the 50-mark at 50.6.

Still, the broader backdrop remains discouraging. 66.2% of surveyed businesses offered negative comments, citing subdued consumer confidence, elevated living costs, and policy-related uncertainty. Public sector retrenchment, inflation, and rising interest rates continue to bite, while seasonal factors like winter and lower tourist activity weigh on demand. BNZ’s Doug Steel summed it up bluntly: “The timeline for New Zealand’s long-awaited economic recovery just keeps getting pushed further and further out.”

China’s exports growth accelerates to 5.8% yoy in June on tariff truce window

China’s exports rose 5.8% yoy in June, beating expectations of 5.0% yoy and marking a pickup from May’s 4.8% yoy. The improvement comes as exporters moved quickly to take advantage of the 90-day tariff truce with the US, front-loading shipments ahead of anticipated disruptions.

The stronger-than-expected performance helped lift China’s trade surplus to USD 114.8B, slightly above consensus and up from USD 103.2B in May.

Imports rose 1.1% yoy, the first positive reading of the year and a tentative sign of stabilization in domestic demand.

Inflation pulse returns as central banks confront tariff fog

This week brings a renewed test for global central banks as June inflation data from the US, UK, Canada, and Japan takes the spotlight.

After months of progress on disinflation, markets are now asking whether the soft patch has run its course. In the US, headline and core CPI are both expected to tick higher—a shift that could signal the low point in inflation may already be behind us.

Fed, already cautious about premature easing, will be particularly sensitive to any inflation reacceleration. With another round of tariffs set to begin in August, policymakers have little room for missteps. A hotter CPI reading, coupled with incoming PPI and retail sales, could keep the Fed sidelined through summer, especially as recent commentary has leaned toward patience over preemption.

In Canada, after a blowout jobs report, Markets now expect BoC to skip a cut again this month. Unless inflation falls meaningfully below expectations, policymakers may extend the pause into fall. However, with trade risks on the rise, the BoC is unlikely to rule out further cuts altogether.

The UK faces a different dilemma: inflation remains too high, but the economy is weakening. BoE is widely expected to cut rates in August following soft GDP figures. This week’s CPI report is unlikely to derail that plan, but the pace of future cuts could hinge on whether inflation starts to retreat materially. UK labor market data, especially wage growth and unemployment, will also play a key role in shaping expectations.

Japan’s inflation data is unlikely to shake BoJ from its holding stance. Policymakers are much more concerned about the external environment, including the impact of trade frictions on demand and financial flows. Even in the event of a CPI surprise to the upside, BoJ is likely to hold rates steady for the remainder of 2025.

China’s Q2 GDP and trade data, along with Germany’s ZEW sentiment index, round out a week heavy on macro signals.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; Japan machines orders, tertiary industry index; China trade balance; Swiss PPI; Canada wholesale sales.

- Tuesday: Australia Westpac consumer sentiment; China GDP, industrial production, retail sales, fixed asset investment; Germany ZEW economic sentiment; Canada CPI, manufacturing sales; US CPI, Empire State menutacturing.

- Wednesday: UK CPI; Eurozone trade balance; Canada housing starts; US PPI, industrial production, Fed’s Beige Book.

- Thursday: Japan trade balance; Australia employment, NAB quarterly business confidence; Swiss trade balance; UK employment; Eurozone CPI final; US jobless claims, retail sales, Philly Fed survey, import prices, business inventories, NAHB housing index.

- Friday: Japan CPI; GErmany PPI; US housing starts and building permits, U of Michigan consumer sentiment and inflation expectations.

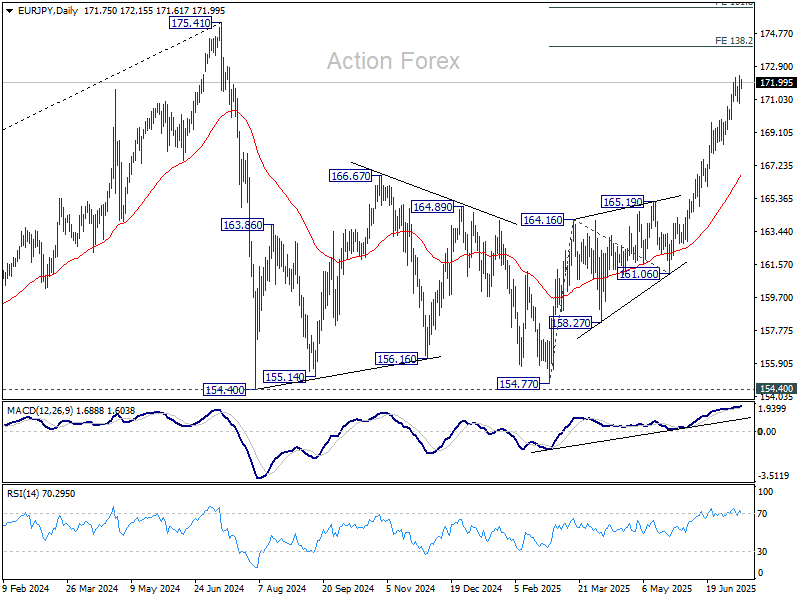

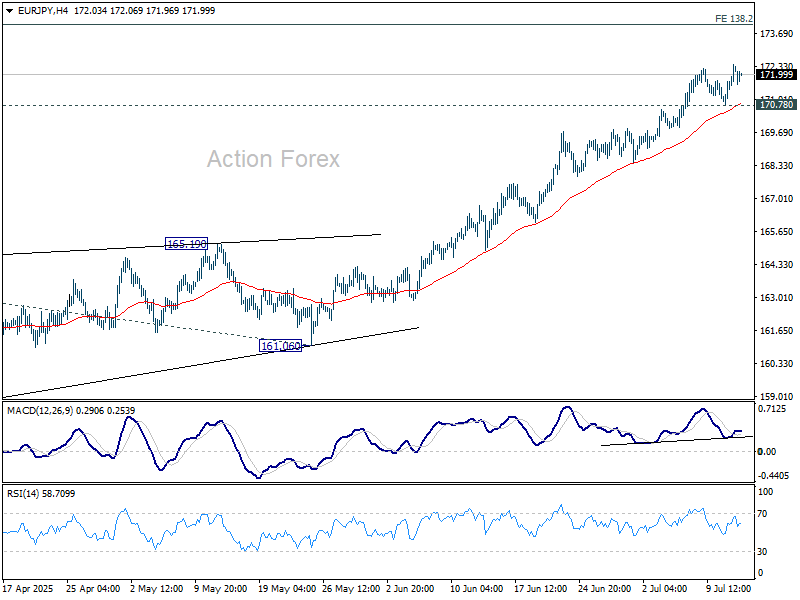

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.25; (P) 171.84; (R1) 172.87; More…

Intraday bias in EUR/JPY remains on the upside for the moment. Current rally from 154.77 should target 138.2% projection of 154.77 to 164.16 from 161.06 at 174.03. On the downside, below 170.78 support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, price actions from 175.41 (2024 high) are seen as correction to up trend from 114.42 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. Meanwhile, decisive break of 175.41 will confirm long term up trend resumption.