Bond Market Signals Deepening Japan Risk , But Yen Finds No Lift from Surging Yields – Action Forex

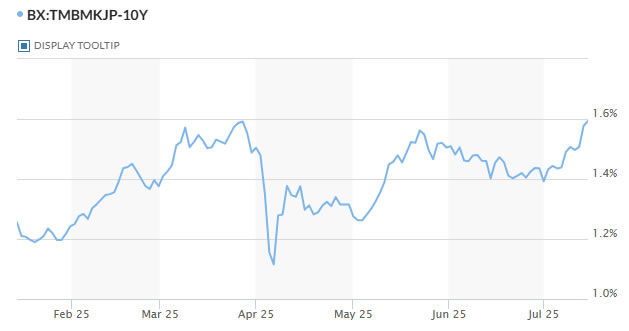

Japanese bond markets are flashing warning signs ahead of a politically uncertain weekend. The 10-year JGB yield surged to its highest level since March and is on the cusp of breaking 1.6% for the first time since 2007. Long-dated yields have moved even more aggressively: the 30-year hit a record 3.21%, while 20-year yields spiked to their highest since 1999. The sell-off reflects growing concern over Japan’s fiscal direction and political stability as the upper house election looms.

Polls suggest Prime Minister Ishiba’s ruling coalition may fall short of even modest expectations. A new NHK survey shows the LDP at its weakest since returning to power more than a decade ago. Investors are worried that a weaker mandate or outright power shift could unleash a wave of populist fiscal proposals—chief among them, sweeping consumption tax cuts or even VAT elimination, as proposed by the right-wing Sanseito party.

Fears of fiscal slippage are not new. In late May, similar concerns drove a steep sell-off in the super-long end, prompting the Ministry of Finance to announce cuts to bond issuance across the 20-, 30-, and 40-year tenors. But that intervention only provided temporary relief. With opposition parties openly campaigning on fiscal expansion, investors are once again questioning Japan’s ability to maintain fiscal discipline.

Despite the surge in yields, Yen has failed to capitalize. The disconnect highlights how fiscal risk may be outweighing any potential monetary policy adjustments. There is some speculation that rising fiscal stimulus could push the BoJ to upgrade its inflation forecasts and consider hiking rates sooner. But for now, that view remains a secondary consideration to market worries about uncontrolled debt issuance.

On the global trade front, tensions between the US and EU are heating up again. Brussels accused Washington of resisting a trade resolution and warned of countermeasures if US President Donald Trump’s 30% tariffs are imposed on August 1. EU ministers signaled growing frustration, with Trade Chief Maros Sefcovic warning that while negotiations may continue, retaliation is now firmly on the table if talks fail to progress.

In FX, risk currencies are currently lagging. Aussie leads losses this week, followed by Kiwi and Sterling. Swiss Franc is the top performer, with Dollar and Loonie also holding firm. Euro and Yen are trading mid-pack.

Technically, CHF/JPY’s up trend continues this week and hit as high as 185.30 so far. Near term outlook will stay bullish as long as 183.19 support holds. Next target is 138.2% projection of 165.83 to 176.45 from 173.06 at 187.73. But overbought condition is likely to cap upside at 161.8% projection at 190.24.

In Asia, at the time of writing, Nikkei is up 0.37%. Hong Kong HSI is up 0.73%. China Shanghai SSE is down -0.61%. Singapore Strait Times is up 0.25%. Japan 10-year JGB yield is up 0.015 at 1.592. Overnight, DOW rose 0.20%. S&P 500 rose 0.14%. NASDAQ rose 0.27%. 10-year yield rose 0.004 to 4.427.

Looking ahead, German ZEW economic sentiment is the main focus in European session. Later in the day, Canada CPI and US CPI are the main events.

Australia Westpac consumer sentiment edges up to 93.1, RBA hold damps household optimism

Australia’s Westpac Consumer Sentiment index edged up 0.6% mom to 93.1 in July, but the modest gain masked a clear sense of disappointment among households.

Westpac noted that sentiment was noticeably stronger before the RBA’s July meeting, with those surveyed prior to the decision reporting a reading of 95.6. That slipped to 92 among those surveyed after the RBA unexpectedly held rates steady, suggesting the decision dashed hopes for relief.

As a result, consumer confidence remains stuck at what Westpac called “cautiously pessimistic” levels.

Looking ahead, markets are eyeing the RBA’s next meeting on August 11–12. While the central bank may pause again if Q2 inflation overshoots, the more likely scenario is a confirmation that inflation stays inside the 2–3% target range. That would pave the way for a 25bps rate cut in August, with another expected in November.

China Q2 GDP growth slows to 5.2%, but beats expectations

China’s economy expanded 5.2% yoy in Q2, slightly above expectations of 5.1% yoy but down from 5.4% yoy in Q1. Sector data showed balanced growth across industries—primary output rose 3.7%, secondary 5.3%, and tertiary 5.5%. The National Bureau of Statistics noted that macroeconomic policies have supported stability, but also flagged persistent weakness in domestic demand and external headwinds.

June’s data painted a mixed picture. Industrial production accelerated from 5.8% yoy to 6.8% yoy, beating forecasts of 5.6% yoy and suggesting continued strength in export-facing sectors and manufacturing. However, retail sales cooled to 4.8% yoy, down sharply from May’s 6.4% yoy and missed expectation of 5.2% yoy.

Fixed asset investment year-to-date slowed to 2.8%, well below expectations of 3.7%. The decline in property investment deepened, falling -11.2% in H1, and private investment contracted -0.6%.

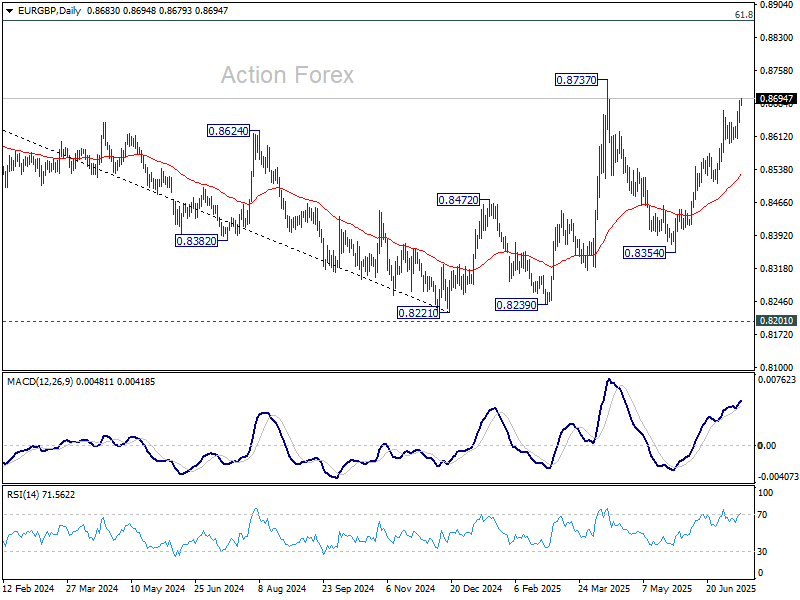

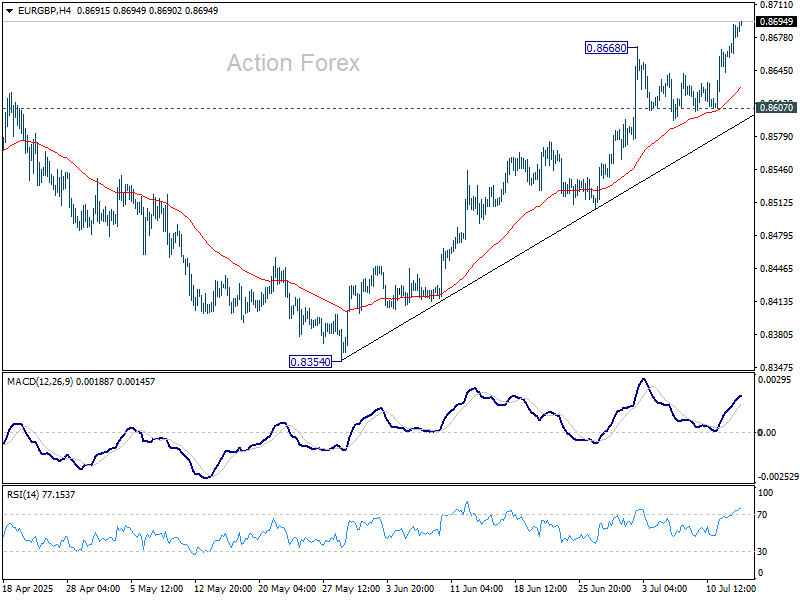

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8658; (P) 0.8675; (R1) 0.8707; More…

EUR/GBP’s rally from 0.8354 resumed by breaking through 0.8668. Intraday bias is back on the upside for 0.8737 high. Decisive break there will resume the whole rise from 0.8221 low, and target 0.8867 fibonacci level. For now, near term outlook will remains bullish as long as 0.8607 support holds.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it’s reversing the down trend from 0.9267 (2022 high). But even if it’s a correction, firm break of 0.8737 will still pave the way to 61.8% retracement of 0.9267 to 0.8221 at 0.8867.