Markets Cautious But Not Panicked, Hope for US-EU Deal Remains – Action Forex

The reaction to US President Donald Trump’s latest tariff salvo has been relatively muted so far. Germany’s DAX and France’s CAC opened mildly lower, but losses remain limited. In currency markets, Euro is holding steady, trading largely inside Friday’s ranges without triggering major downside momentum. The market appears to be bracing for drawn-out negotiations rather than immediate escalation.

Optimism is underpinned by Trump’s negotiation history—often characterized by bold opening demands followed by compromise. The fact that the 30% tariff on EU imports is scheduled to take effect in August, not immediately, reinforces the view that space remains for a diplomatic resolution. The final rate will likely land well below 30%, even though above the UK’s 10% benchmark.

European Trade Commissioner Maros Sefcovic warned Monday that the 30% tariff would severely disrupt transatlantic trade, but voiced hope that a resolution could still be achieved. “We have to do everything we can to prevent this super-negative scenario,” he said. Talks between the EU and Washington are ongoing, and the EU has not yet announced any retaliatory measures, which has helped temper market nerves.

Elsewhere, South Korea is also looking for a way out of the tariff web. Trade Minister Yeo Han-koo said an in-principle agreement might be achievable before August 1. Speaking to local media, he hinted Seoul may open up its agricultural markets while protecting strategic industrial sectors. “Twenty days are not enough to come up with a perfect treaty,” he acknowledged, but reiterated the urgency of preventing damaging tariffs on Korean exports.

In currency markets, the Canadian Dollar is leading gains, while Swiss Franc and Yen are benefitting from mild safe-haven demand. New Zealand and Australian Dollars remain under pressure, despite China’s better-than-expected trade numbers. Sterling is weak as well. Dollar and Euro are trading near mid-pack.

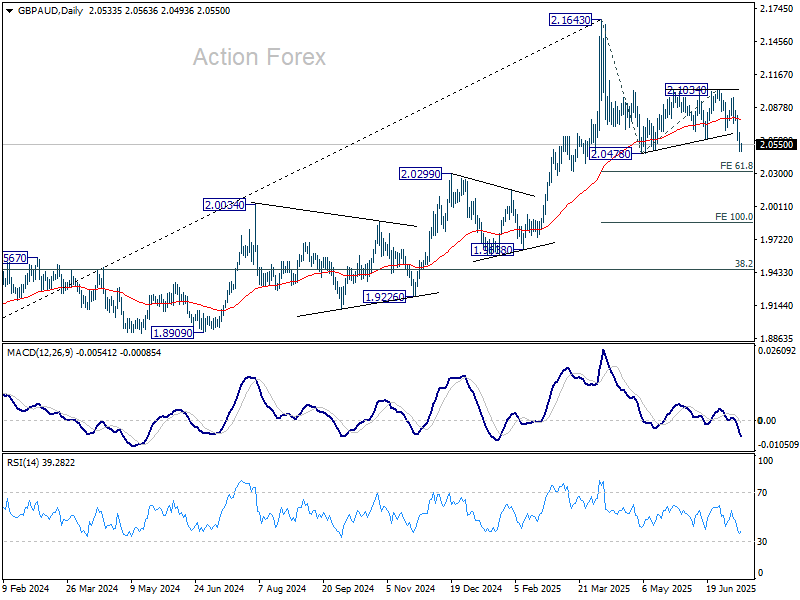

Technically, one pair to watch is GBP/AUD. After last week’s extended decline, it’s now pressing 2.0478 support. Firm break there will resume whole fall from 2.1643, and target 61.8% projection of 2.1643 to 2.0478 from 2.1034 at 2.0314. Decisive break there could prompt further acceleration to 100% projection at 1.9869.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is down -0.89%. CAC is down -0.42%. UK 10-year yield is down -0.009 at 4.620. Germany 10-year yield is up 0.01 at 2.735. Earlier in Asia, Nikkei fell -0.28%. Hong Kong HSI rose 0.26%. China Shanghai SSE rose 0.27%. Singapore Strait Times rose 0.52%. Japan 10-year JGB yield rose 0.07 to 1.577.

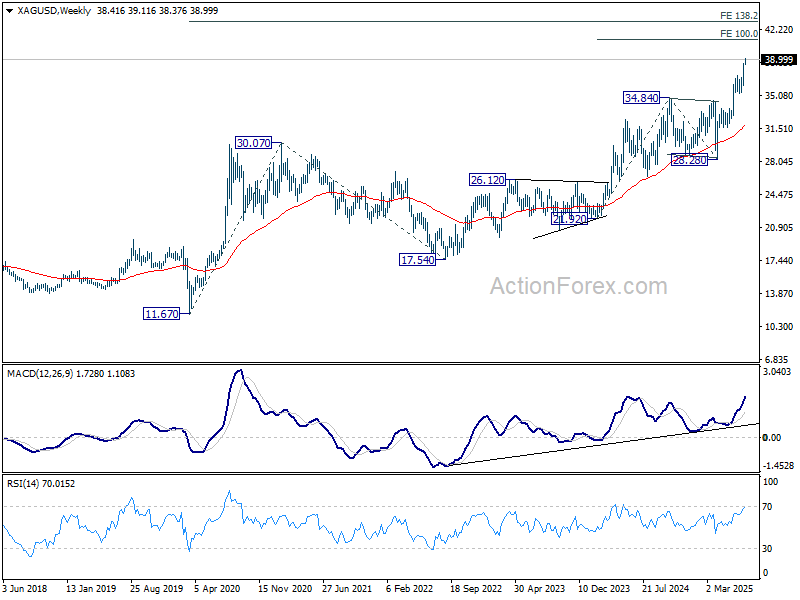

Silver hits near 14-year high and targest 40 as global flows accelerate

Silver’s rally picked up pace on Monday, hitting its highest level since late 2011 after last week’s decisive upside breakout. The metal has surged alongside broad-based strength in precious metals, with Palladium reaching its highest since October 2024 and Gold rebounding to a three-week high. Renewed investor interest across the complex suggests increasing demand for portfolio diversification amid geopolitical and trade policy risks.

One notable driver has been rising demand out of India, where investors are shifting from Gold to Silver as a catch-up trade after years of underperformance. Silver is also seeing structural demand growth tied to industrial applications—especially in solar energy and electric vehicles—which is outpacing domestic production. This dual push from both speculative and real-economy buyers is adding fuel to the current run.

Technically, Silver is on track to 61.8% projection of 31.65 to 37.28 from 36.24 at 39.71, or even further to 40 pscyholgical level. However, upside could be capped by medium term level of 100% projection of 21.92 to 34.83 from 28.28 at 41.20 on first attempt.

NZ BNZ services rises to 47.3, but outlook remains grim

New Zealand’s services sector showed mild improvement in June, with BusinessNZ Performance of Services Index rising to 47.3 from May’s 44.1. Despite the gain, the index remains well below its long-run average of 52.9 and firmly in contraction territory. Subcomponents showed modest upticks—new orders rose from 43.4 to 48.8, employment edged up from 47.1 to 47.4, and activity/sales climbed to 44.5. Inventories just breached the 50-mark at 50.6.

Still, the broader backdrop remains discouraging. 66.2% of surveyed businesses offered negative comments, citing subdued consumer confidence, elevated living costs, and policy-related uncertainty. Public sector retrenchment, inflation, and rising interest rates continue to bite, while seasonal factors like winter and lower tourist activity weigh on demand. BNZ’s Doug Steel summed it up bluntly: “The timeline for New Zealand’s long-awaited economic recovery just keeps getting pushed further and further out.”

China’s exports growth accelerates to 5.8% yoy in June on tariff truce window

China’s exports rose 5.8% yoy in June, beating expectations of 5.0% yoy and marking a pickup from May’s 4.8% yoy. The improvement comes as exporters moved quickly to take advantage of the 90-day tariff truce with the US, front-loading shipments ahead of anticipated disruptions.

The stronger-than-expected performance helped lift China’s trade surplus to USD 114.8B, slightly above consensus and up from USD 103.2B in May.

Imports rose 1.1% yoy, the first positive reading of the year and a tentative sign of stabilization in domestic demand.

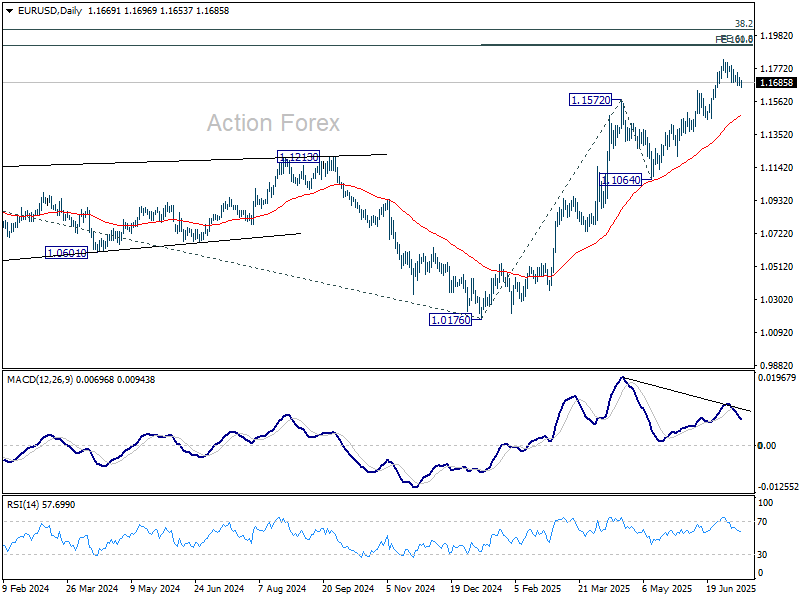

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1665; (P) 1.1690; (R1) 1.1714; More…

EUR/USD is still extending the correction from 1.1829 and intraday bias remains neutral for the moment. Downside should be 1.1630 resistance turned support to bring rebound. Firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, sustained break of 1.1630 will bring deeper fall to 55 D EMA (now at 1.1474) instead.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.