RBA Signals More Cuts, Trade Risk Looms Across Asia – Action Forex

Aussie edged lower in Tuesday’s Asian session after minutes from the RBA’s July meeting confirmed a dovish bias, despite the surprise interest rate hold. The Board remains inclined to ease further, with the debate centered around timing rather than direction. Markets are leaning heavily toward an August rate cut, especially if Q2 CPI doesn’t deliver any upside surprises. Meanwhile, Kiwi underperformed despite robust trade data, while post-election short covering in the Yen appears to be fading. Swiss Franc leads on the day, followed by Dollar and Loonie, while Euro and Sterling stay in the middle.

On the trade front, U.S. Treasury Secretary Scott Bessent confirmed that August 1 remains the activation date for sweeping new tariffs. Though he characterized the move more as a negotiating lever than a final deadline. In an interview with CNBC, Bessent said, “The important thing here is the quality of the deal,” reinforcing the Trump administration’s position that the tariffs are primarily about leverage, not timing.

In South Korea, the newly appointed economic leadership is scrambling to respond. Finance Minister Koo Yun-cheol and Trade Minister Yeo Han-koo will meet top US officials in Washington this week, as Seoul seeks to contain the damage from tariffs. President Lee Jae Myung’s administration is under pressure to deliver quickly, with multiple cabinet-level visits planned for the coming days to shape a coordinated trade response.

Japan, too, is back at the negotiating table. Chief trade envoy Akazawa Ryosei has returned to Washington for the eighth time, seeking to restart stalled talks following a bruising election result for the ruling coalition. Japan is hoping to secure an agreement that will avert 25% auto tariffs by Trump’s August 1 deadline. Officials are signaling flexibility, but insist that any deal must protect core Japanese interests.

India, on the other hand, appears stuck. Sources say the latest talks in Washington failed to resolve differences on auto parts, steel, and agricultural tariffs. With no breakthrough and the US delegation not expected in Delhi until mid-August, India faces the very real possibility of being hit with a 26% blanket tariff. That puts additional pressure on Prime Minister Narendra Modi’s economic team as the clock ticks down.

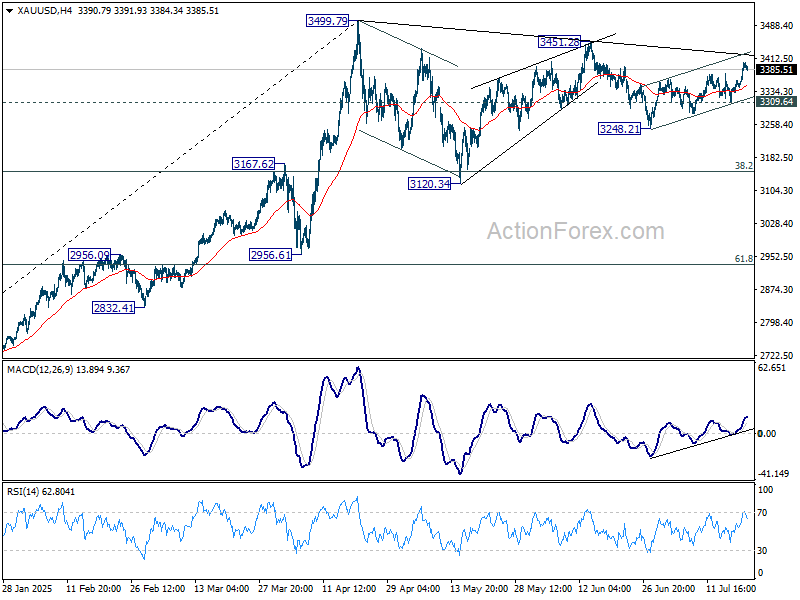

Technically, Gold’s rebound from 3248.21 resumed this week and breached 3400 handle briefly. Still, overall price actions suggest that it’s still extending the corrective pattern from 3499.79 high. There is no clear momentum for an imminent breakout. As for the current rebound, strong resistance should emerge around 3451.28 to limit upside. Break of 3309.64 support will start another downleg in the pattern and target 3248.21 and below.

In Asia, at the time of writing, Nikkei is down -0.27%. Hong Kong HSI is up 0.36%. China Shanghai SSE is up 0.59%. Singapore Strait Times is down -0.18%. Japan 10-year JGB yield is down -0.026 at 1.507. Overnight, DOW fell -0.04%. S&P 500 rose 0.14%. NASDAQ rose 0.38%. 10-year yield fell -0.060 to 4.372.

RBA minutes: Case for easing intact, but timing still debated

Minutes from the RBA’s July 7–8 meeting reveal a Board broadly aligned on the view that there will be “some additional reduction in interest rates over time”. Yet, the board is divided on the “appropriate timing and extent of further easing”. The majority ultimately judged it prudent to keep the cash rate steady at 3.85%.

The decision to hold reflected stronger-than-expected recent data, including “a little stronger than expected” private demand in Q1 and resilient labor market that ” has not eased as anticipated”. Monthly inflation readings had also been “marginally higher” than staff projections. Additionally, Members noted that reduced global risks allowed greater confidence in the RBA’s baseline forecasts, rather than the worst-case scenario.

Still, the minutes make clear that the RBA remains on an easing path. Some members argued there was already enough evidence to justify a cut now, but the Board as a whole leaned toward keeping a cautious, gradual approach, which is inconsistent with a third rate cut within the space of four meetings at that time.

New Zealand imports jump 19% yoy in June, while exports rise 10% yoy

New Zealand posted a trade surplus of NZD 142m in June, falling well short of market expectations for NZD 1.02B. The softer balance came despite solid annual growth in both exports and imports. Goods exports rose 10% yoy to NZD 6.6B and imports surging 19% to NZD 6.5B.

Regionally, exports to the EU jumped 38% yoy, followed by gains to China (11% yoy) and Australia (16% yoy). However, exports to the US and Japan declined -8.8% yoy and -4.7% yoy respectively.

The strength in exports was not enough to offset the broader pressure from surging imports, particularly as US ( 21% yoy) and South Korean (40% yoy) shipments rose sharply. Imports from EU (0.8% yoy), Australia (6.8% yoy) and China (9.1% yoy) also grew.

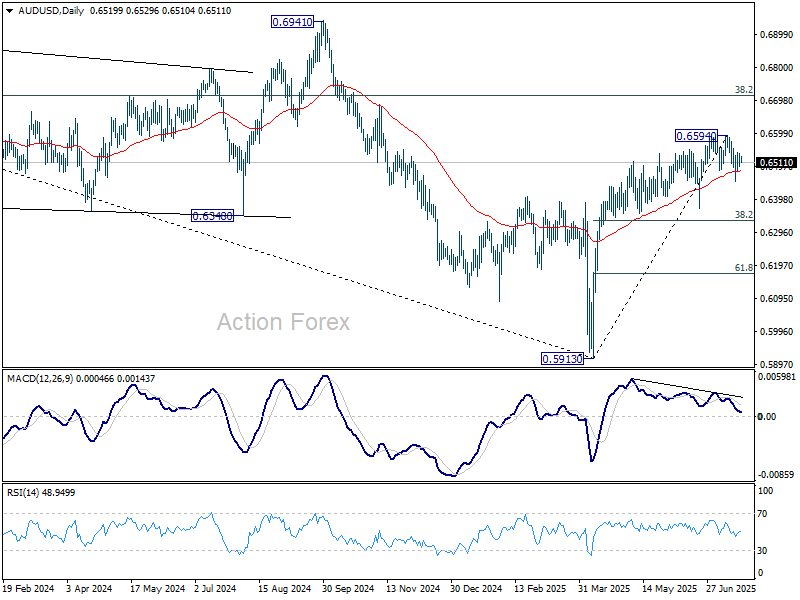

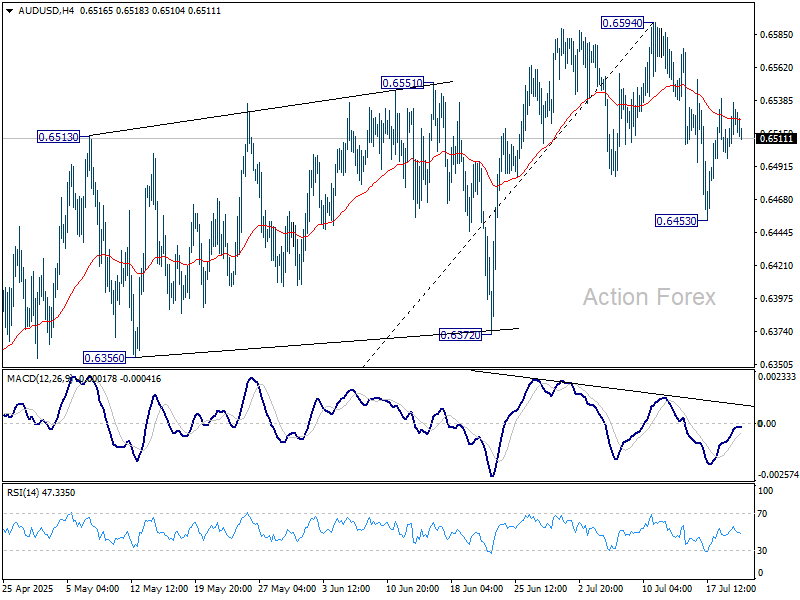

AUD/USD Daily Report

Daily Pivots: (S1) 0.6478; (P) 0.6509; (R1) 0.6539; More...

AUD/USD’s dips mildly after failing to break through 55 4H EMA (now at 0.6524) decisively. Intraday bias remains neutral first. The corrective fall from 0.6594 short term top could extend lower. On the downside, break of 0.6453 will target 38.2% retracement of 0.5913 to 0.6594 at 0.6334, as a correction to the whole rally from 0.5913. Risk will stay mildly on the downside for now as long as 0.6594 resistance holds, in case of stronger recovery.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).