Trade War Fears Pressure Euro Stocks as EU Retaliation Risks Grow – Action Forex

European Markets are increasingly uneasy over signs that the EU is preparing serious retaliatory measures ahead of the August 1 US tariff deadline. The Anti-Coercion Instrument is increasingly in the spotlight, as EU leaders weigh how to respond to US President Donald Trump’s threat of sweeping 30% import tariffs. European equities are firmly in the red, with DAX and CAC losses amplified by soft earnings, while US futures remain relatively stable.

According to reports, the EU is open to negotiating a tariff framework that resembles the UK’s deal—swallowing a 10% base rate while preserving core industries such as autos and aerospace. However, anything above 15% could prompt a forceful response, especially given the political sensitivity of industrial exports in member states like Germany and France.

Brussels is now openly discussing activating the ACI, which grants the EU power to impose a wide range of retaliatory measures. These could target public procurement, limit access for US companies in agriculture and chemicals, and extend to services where the US runs surpluses. While seen as a last resort, sentiment is shifting toward actual deployment if Trump follows through. The ACI is increasingly viewed as more than a symbolic threat.

In currency markets, the risk-off mood is visible. Aussie and Kiwi are underperforming, joined by a weaker British Pound. Yen is the top performerm with Loonie and Swiss Franc close behind. Euro and Dollar are positioning in the middle.

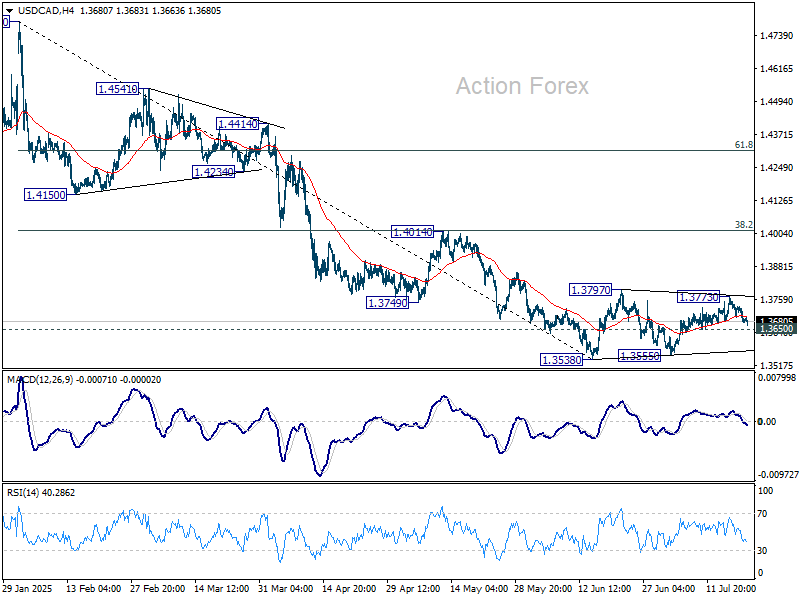

Technically, USD/CAD is worth a watch as the fall from 1.3772 extends today. Break of 1.3650 support will argue that corrective pattern from 1.3538 might have completed already. Larger fall from 1.4791 might then be ready to resume through 1.3538 low.

In Europe, at the time of writing, FTSE is down -0.08%. DAX is down -1.16%. CAC is down -0.82%. UK 10-year yield is up 0.006 at 4.613. Germany 10-year yield down -0.007 at 2.612. Earlier in Asia, Nikkei fell -0.11%. Hong Kong HSI rose 0.54%. China Shanghai SSE rose 0.62%. Singapore Strait Times rose 0.03%. Japan 10-year JGB yield fell -0.025 to 1.507.

Fed’s Bowman: Independence also requires listening, transparency

Fed Vice Chair for Supervision Michelle Bowman reaffirmed the central bank’s commitment to policy independence during an interview with CNBC, stating that “it’s very important… that we maintain our independence with respect to monetary policy.”

Meanwhile, she stressed that this autonomy must be matched by a commitment to openness. “We have an obligation for transparency and accountability as well,” she noted.

Bowman also stressed the importance of listening to a wide range of voices in forming monetary policy. Since joining the Board in 2018, she said the Fed has consistently engaged with diverse viewpoints to better understand how different segments of the economy are affected.

“That should influence our decisions in monetary policymaking,” she said.

BoE’s Bailey: Rising gilt yields part of global trade and fiscal uncertainty

BoE Governor Andrew Bailey told the Treasury Committee that the recent rise in long-term borrowing costs reflects global trends rather than UK-specific issues. Responding to questions on the growing cost of government debt, Bailey emphasized that similar, or even steeper, yield increases have occurred in other advanced economies.

He attributed the shift to heightened uncertainty on two key fronts: “one is uncertainty around what is going on in trade policy at the moment. The second thing is uncertainty globally around fiscal policy he said.

Bailey noted that unpredictable tariff strategies and widening fiscal deficits are contributing to volatility in fixed income markets worldwide, driving up yields across the curve. “It is greater uncertainty, clearly,” he said.

RBA minutes: Case for easing intact, but timing still debated

Minutes from the RBA’s July 7–8 meeting reveal a Board broadly aligned on the view that there will be “some additional reduction in interest rates over time”. Yet, the board is divided on the “appropriate timing and extent of further easing”. The majority ultimately judged it prudent to keep the cash rate steady at 3.85%.

The decision to hold reflected stronger-than-expected recent data, including “a little stronger than expected” private demand in Q1 and resilient labor market that ” has not eased as anticipated”. Monthly inflation readings had also been “marginally higher” than staff projections. Additionally, Members noted that reduced global risks allowed greater confidence in the RBA’s baseline forecasts, rather than the worst-case scenario.

Still, the minutes make clear that the RBA remains on an easing path. Some members argued there was already enough evidence to justify a cut now, but the Board as a whole leaned toward keeping a cautious, gradual approach, which is inconsistent with a third rate cut within the space of four meetings at that time.

New Zealand imports jump 19% yoy in June, while exports rise 10% yoy

New Zealand posted a trade surplus of NZD 142m in June, falling well short of market expectations for NZD 1.02B. The softer balance came despite solid annual growth in both exports and imports. Goods exports rose 10% yoy to NZD 6.6B and imports surging 19% to NZD 6.5B.

Regionally, exports to the EU jumped 38% yoy, followed by gains to China (11% yoy) and Australia (16% yoy). However, exports to the US and Japan declined -8.8% yoy and -4.7% yoy respectively.

The strength in exports was not enough to offset the broader pressure from surging imports, particularly as US ( 21% yoy) and South Korean (40% yoy) shipments rose sharply. Imports from EU (0.8% yoy), Australia (6.8% yoy) and China (9.1% yoy) also grew.

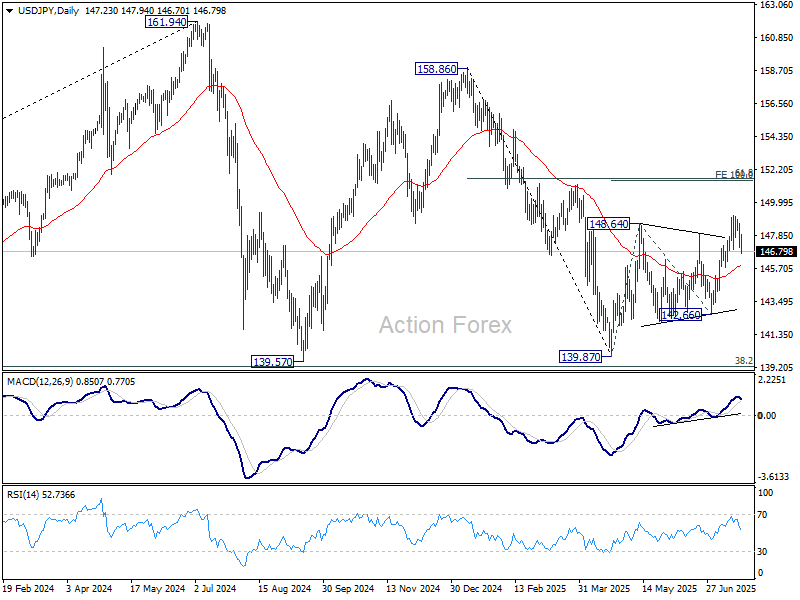

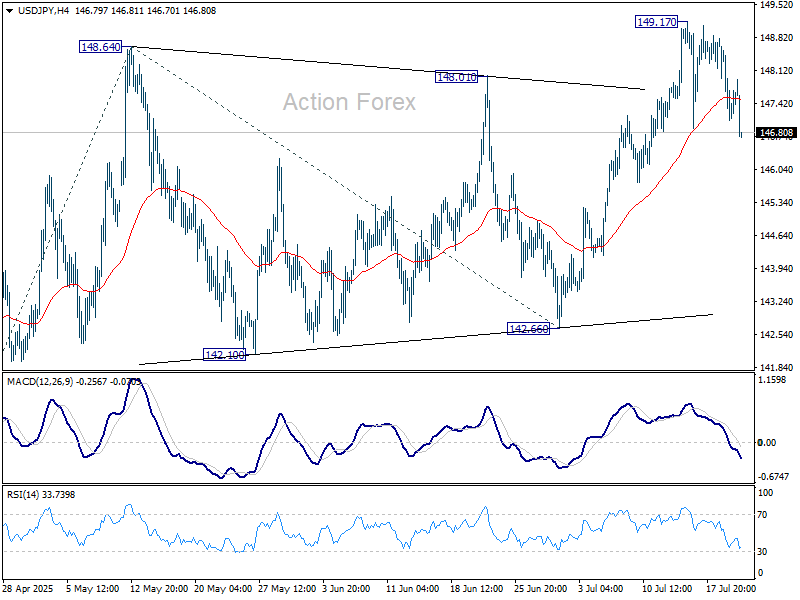

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.72; (P) 147.70; (R1) 148.31; More…

USD/JPY’s fall from 149.17 extends lower today, but it’s still viewed as a correction to rise from 142.66 only. Intraday bias remains neutral and further rally is expected as long as 55 D EMA (now at 145.91) holds. On the upside, break of 149.17 will target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22. However, sustained trading below 55 D EMA will argue that the whole rebound from 139.87 might have completed and target 142.66 support for confirmation.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. in case of another fall.