Yen Stabilizes Post-Election, But BoJ Hike Could Be Further Away – Action Forex

Yen showed modest gains to start the week, but the broader forex markets stayed quiet with all major pairs and crosses confined to Friday’s ranges. Traders were largely unfazed by Japan’s upper house election, which delivered no shocks. The muted reaction suggests markets had priced in the LDP’s setback and are now shifting focus to what comes next politically and economically.

The LDP’s failure to retain a majority marks the first time since 1955 that the ruling coalition has lost control of the chamber. That further weakened Prime Minister Shigeru Ishiba’s political footing following October’s lower house loss. Despite the setback, Ishiba has expressed his intention to stay in office and govern by seeking limited cooperation from opposition parties. One likely consequence is a move toward looser fiscal policy, as Ishiba courts centrist or left-leaning support. That path would likely pressure to Yen.

Also, historically, periods of political instability in Japan have discouraged the BoJ from taking aggressive policy steps. That tradition is likely to continue, pushing the timeline for any rate hikes further into the future.

On the trade front, US Commerce Secretary Howard Lutnick reiterated Sunday that new tariffs will go into effect on the hard deadline August 1. He added that countries could still engage diplomatically in negotiation, but only after paying the tariffs.

Meanwhile, Lutnick also said that some smaller countries in Latin America, Caribbean, and Africa will have a low baseline tariffs of 10%. However, “the bigger economies will either open themselves up or they’ll pay a fair tariff to America,” he added.

Overall in the currency markets, Yen is currently the strongest for the day, followed by Sterling, and then Euro. Kiwi is the worst after CPI miss, followed by Loonie and Aussie. Dollar and Swiss Franc are in the middle.

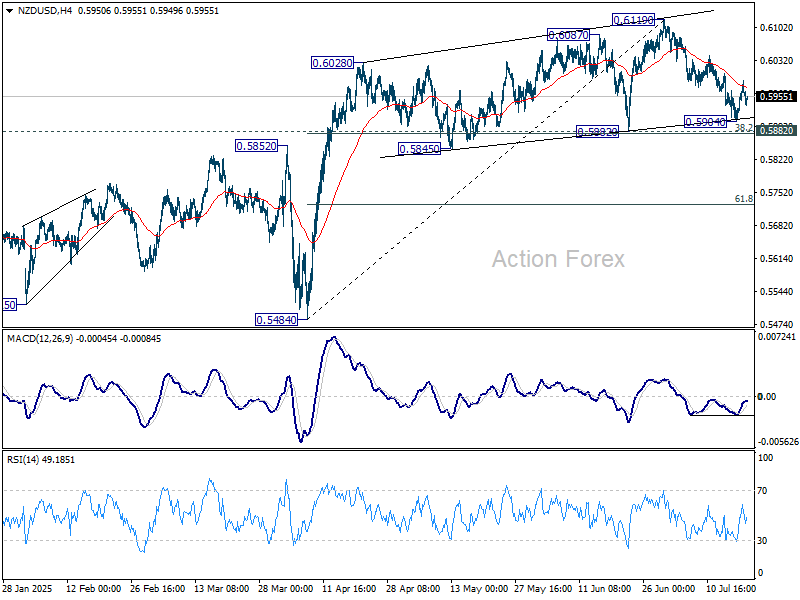

Technically, NSD/USD’s corrective pullback from 0.6119 is losing momentum as seen in 4H MACD. While another fall cannot be ruled out, downside should be contained by 0.5882 cluster support (38.2% retracement of 0.5484 to 0.7119 at 0.5876) and bring rebound. Meanwhile, sustained trading above 55 4H EMA (now at 0.5975) will suggest that the correction has completed, and bring stronger rise back to retest 0.6119 high.

In Asia, at the time of writing, Japan is on holiday. Hong Kong HSI is up 0.23%. China Shanghai SSE is up 0.46%. Singapore Strait Times is up 0.40%.

NZ CPI rises to 2.7% yoy in Q2, tradeabales jump

New Zealand’s CPI rose 0.5% qoq in Q2, slightly below expectations for 0.6% qoq. Annual inflation ticked up to 2.7% yoy from 2.5% yoy but still undershot 2.8% yoy forecast. Headline inflation remained comfortably within the RBNZ’s target range of 1-3%. Tradeables inflation climbed sharply to 1.2% yoy from 0.3% yoy. Non-tradeables eased to 3.7% yoy from 4.0% yoy, indicating moderating domestic pressures.

The quarterly print showed notable increases in cultural services (+9.5% qoq), electricity (+4.9% qoq), and vegetables (+10.0% qoq), which together accounted for over 70% of the total quarterly CPI rise. However, these gains were partially offset by a -4.8% qoq drop in petrol prices and -9.2% qoq decline in domestic accommodation services.

ECB to hold fire, RBA minutes and global PMIs anchor light data week

This week’s spotlight is on the ECB, with little else on the calendar likely to drive significant volatility. The central bank is widely expected to leave the deposit rate unchanged at 2.00%, pausing after a steady sequence of cuts since June 2024. The July meeting is not expected to bring major shifts in tone, but attention will turn to September, where updated projections could set the stage for the final rate move of this cycle.

According to a recent Reuters poll, 58% of economists—49 out of 84 surveyed—expect the ECB to deliver one final 25bp cut in September to complete its easing. Twenty respondents believe the current level is already the floor, while only 15 foresee two or more additional reductions. That slim majority suggests consensus is forming around one more move, but much hinges on developments in global trade and inflation dynamics.

With US tariff policy still evolving and the EU weighing possible retaliation, ECB President Christine Lagarde is unlikely to provide definitive forward guidance this week. September’s decision will depend heavily on how the tariff situation unfolds and what it implies for inflation, growth, and confidence. Those factors will be incorporated into the ECB’s updated macroeconomic projections, which should give more clarity about the path forward.

Meanwhile, the RBA’s July meeting minutes are also due and could offer some clarification on the central bank’s surprise decision to hold rates at 3.85%. With the vote split 6-3, the minutes might reveal whether the pause was tactical—a brief wait for more data before an August cut—or part of a deeper internal disagreement. Still, the broader tone is expected to remain cautiously dovish.

The rest of the week features July PMIs from the US, Eurozone, UK, and Japan—key data to assess how global economies are absorbing the impact of tariffs. Retail sales from Canada and the UK will offer insights into consumer resilience, while Germany’s Ifo business climate and Japan’s Tokyo CPI provide a check on sentiment and inflation.

Here are some highlights for the week:

- Monday: New Zealand CPI; China rate decision; Canada IPPI and RMPI, BoC business outlook survey.

- Tuesday: New Zealand trade balance; RBA minutes; UK public sector net borrowing.

- Wednesday: Canada new housing price index; US existing home sales.

- Thursday: Australia PMIs; Japan PMIs; Germany Gfk consumer climate; Eurozone PMIs, ECB rate decision; UK PMIs; Canada retail sales; US jonless claims, PMIs, new home sales.

- Friday: UK Gfk consumer sentiment; Japan Tokyo CPI; UK retail sales; Germany Ifo business climate; US durable goods orders.

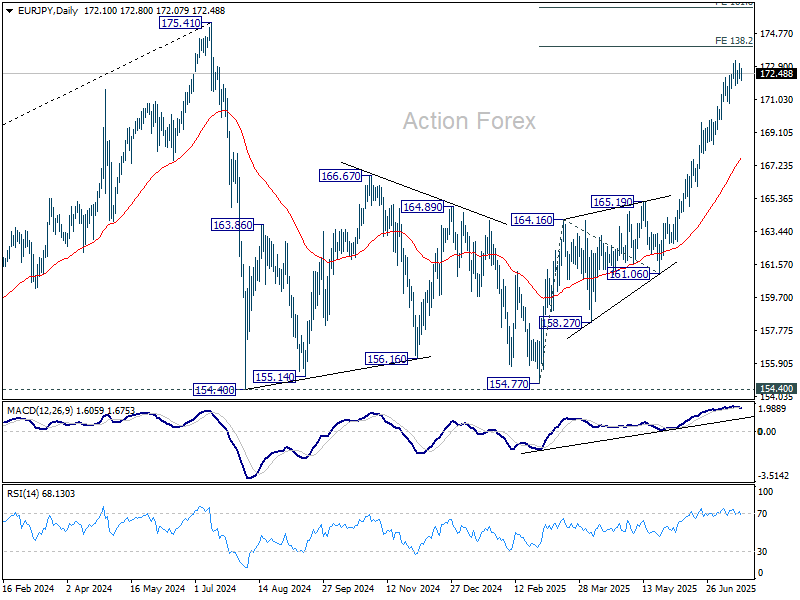

EUR/JPY Daily Outlook

Daily Pivots: (S1) 172.26; (P) 172.69; (R1) 173.39; More…

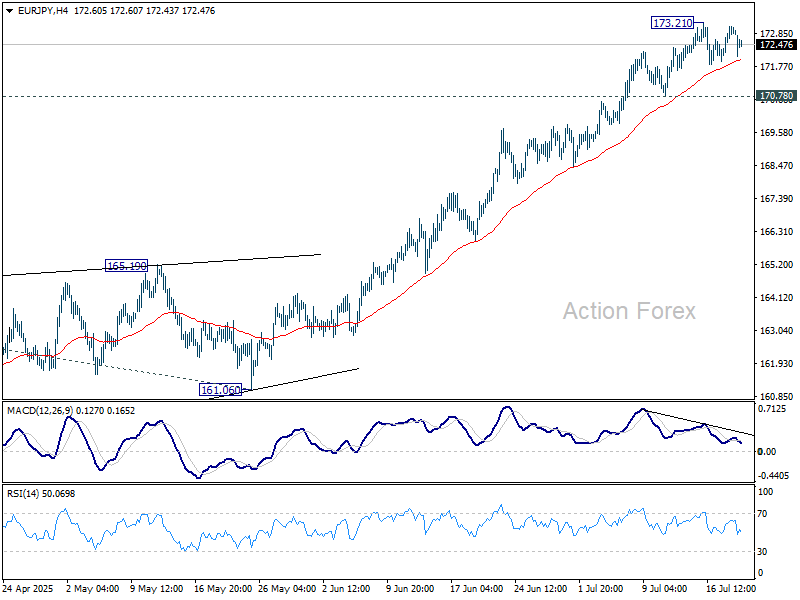

EUR/JPY dips mildly today as consolidations from 173.21 extends. Intraday bias stays neutral for the moment. Further rise is expected as long as 170.78 support holds. On the upside, break of 173.21 will target 138.2% projection of 154.77 to 164.16 from 161.06 at 174.03. Break there will bring retest of 175.41 high. Nevertheless, considering bearish divergence condition in 4H MACD, break of 170.78 will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, price actions from 175.41 (2024 high) are seen as correction to up trend from 114.42 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. Meanwhile, decisive break of 175.41 will confirm long term up trend resumption.