BoE’s Hawkish Cut Sparks Sterling Rally – Action Forex

Sterling surged across the board after the BoE delivered a widely expected rate cut to 4.00%, but with a much tighter vote split than markets anticipated. Four of the nine Monetary Policy Committee members voted to keep rates unchanged, signaling persistent concerns about upside inflation risks. This hawkish undercurrent, paired with Governor Andrew Bailey’s cautious tone, undercut expectations for an accelerated easing cycle and helped Sterling lead currency gains on the day.

The hawkish composition of the vote suggests that a follow-up cut in September can be basically ruled out. Odds for a November reduction remain slightly in play, but confidence has diminished. Much will hinge on whether inflation indeed peaks at 4% in September as projected, and if it visibly starts to retreat in October. Until then, investors may treat incoming inflation and wage data as binary catalysts for the next policy move.

Bailey reiterated in the press conference that while the policy path remains downward, it is now clouded by uncertainty. “We do not cut too quickly or by too much,” he warned, highlighting energy and food prices as short-term distortions. His response to questions about the policy direction was telling: while still confident about the eventual path, the Governor acknowledged that the timing and scale of future moves are more uncertain than before.

In the currency markets, Sterling is currently the day’s top performer. Kiwi and Aussie followed in strength, reflecting an underlying risk-on tilt in sentiment. At the other end, Swiss Franc lagged broadly, followed by Euro and Loonie. Dollar and Yen were mixed as they consolidated recent losses.

In Japan, the government downgraded its GDP growth outlook for the fiscal year to 0.7% from 1.2%, citing US tariffs’ drag on capital spending and inflation’s toll on private consumption. Despite the downgrade, the government maintained hope that wage growth would overtake inflation in 2026, supporting a modest recovery in domestic demand-led growth.

In India, Prime Minister Narendra Modi responded forcefully to President Trump’s imposition of a 50% tariff on Indian goods, insisting that his government would not compromise on the welfare of farmers. The message came as Indian and Russian officials met in Moscow to reaffirm their strategic partnership, a sign that geopolitical alignment may further complicate the tariff dispute.

In Europe, at the time of writing, FTSE is down -0.75%. DAX is up 1.65%. CAC is up 1.13%. UK 10-year yield is up 0.027 at 4.56. Germany 10-year yield is down -0.001 at 2.649. Earlier in Asia, Nikkei rose 0.65%. Hong Kong HSI rose 0.69%. China Shanghai SSE rose 0.16%. Singapore Strait Times rose 0.72%. Japan 10-year JGB Yield fell -0.016 to 1.486.

US initial jobless claims rise to 226k, continuing claims highest since late 2021

US initial jobless claims rose 7k to 226k in the week ending August 2, above expectation of 220k. Four-week moving average of initial claims fell -500 to 221k.

Continuing claims rose 38k to 1974k in the week ending July 26, highest since November 6 2021. Four-week moving average of continuing claims rose 5k to 1952k.

BoE cuts to 4.00%, hawkish 5-4 vote lifts Sterling

BoE delivered a widely expected 25 basis point rate cut, lowering the Bank Rate to 4.00% and continuing its cautious easing cycle. However, a hawkish four-member minority, including Chief Economist Huw Pill, Megan Greene, Clare Lombardelli, and Catherine Mann voted to hold rates steady, reflecting continued concern over lingering inflation pressures.

Governor Andrew Bailey led the five-member majority in favor of the reduction, and no member supported a larger reduction (Alan Taylor voted to cut bank rate by 50 bps in first round but changed to 25 bps in second round to avoid hold).. This signals that while easing continues, the BoE is far from embracing a more aggressive cutting path.

The BoE’s updated projections show inflation expected to rise temporarily, peaking around 4.0% in September before falling back toward the 2% target. However, the MPC noted that upside risks to medium-term inflation “have moved slightly higher” since May, citing concerns that temporary price increases could entrench wage and pricing behaviors. This inflation vigilance likely explains the hawkish vote split and continued pushback against front-loading cuts.

On the growth side, the MPC noted that underlying GDP “remains subdued”, with slack emerging in the labor market. While domestic and global uncertainties persist, the committee acknowledged that trade policy risk has “diminished somewhat”—a nod to easing tensions after recent UK-U.S. tariff agreements.

Even with economic momentum fading, the MPC maintained that policy is “not on a pre-set path,” emphasizing a “gradual and careful approach” to further easing.

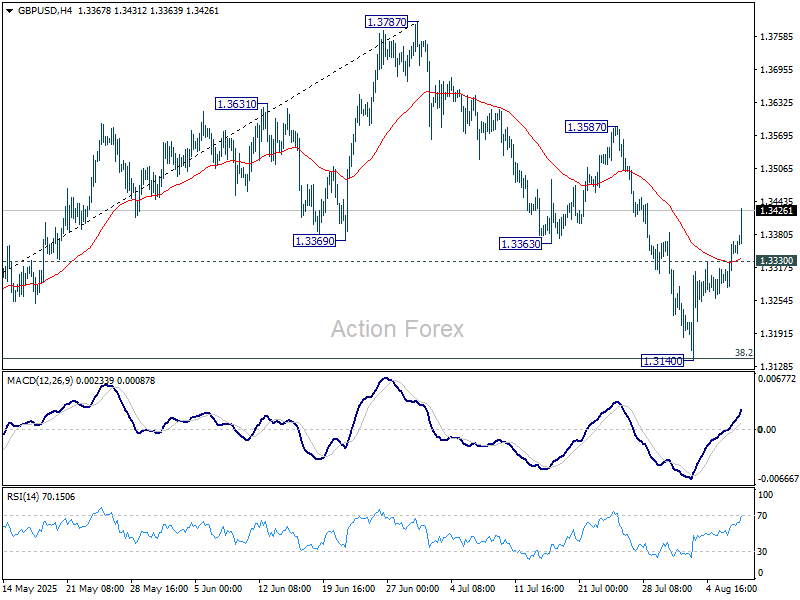

Sterling responded positively to the rate cut and the hawkish tilt in the vote. GBP/USD’s rally from 1.3140 accelerates after the announcement. Current development further affirms the case that correction from 1.3787 has completed with three waves down to 1.3140. Further rise should be seen to 1.3587 resistance first. Firm break there will target a retest on 1.3787 high.

RBNZ survey signals one more cut, then long pause ahead

RBNZ’s August Survey of Expectations suggests the central bank will likely cut rates only once more in 2025, but the outlook beyond that remains cautious. The OCR is forecast to decline from 3.25% to 3.02% by September 2025 — consistent with a single 25bps move, likely in this month’s meeting. By June 2026, it’s seen at 2.86%, implying a second cut is possible in H1 2026, but far from assured.

Inflation expectations continue to ease gradually. One-year-ahead CPI forecasts slipped from 2.41% to 2.37%, while two-year-ahead projections fell marginally from 2.29% to 2.28%. Wage inflation expectations were mixed, with one-year views dropping to 2.61% while two-year expectations rose to 2.88%, implying confidence that wage pressures will not reignite inflation risks over the medium term.

The unemployment outlook also improved slightly, with expectations for joblessness falling across all time horizons. Despite soft growth conditions, respondents see GDP rising 1.66% over the next year and 2.16% the year after. Taken together, the survey points to a slow-moving easing cycle ahead, starting with one cut likely later this year, followed by a potentially long pause.

Strong oil, soybean demand drives China import spike, cuts surplus

China’s July trade data surprised to the upside, with exports rising 7.2% yoy and imports jumping 4.1% yoy — the largest annual gain in over a year. Strong commodity demand underpinned the figures, as soybean imports surged 18.5% yoy and crude oil shipments rose 11.5% yoy.

The trade surplus came in at USD 98.2 B, narrower than the expected USD 107.9B, suggesting stronger domestic demand helped balance trade flows.

While the numbers offer a positive signal for global demand, investors remain focused on the looming August 12 deadline to finalize a lasting trade agreement with the US. The strong data may give Beijing some negotiating leverage, but uncertainty remains high.

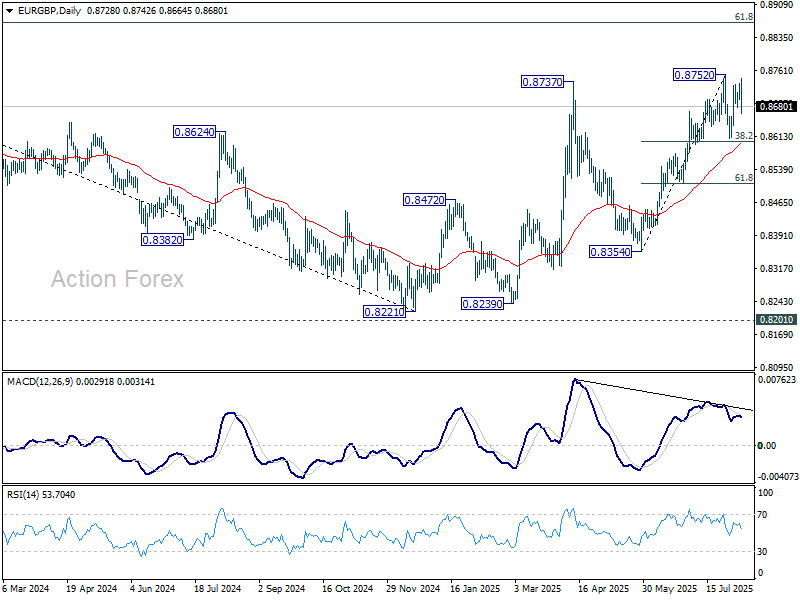

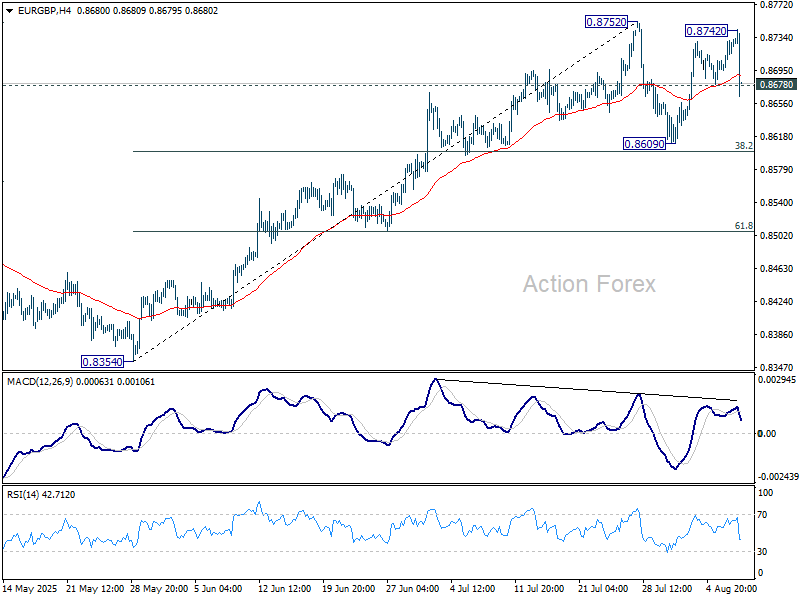

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8707; (P) 0.8720; (R1) 0.8742; More…

EUR/GBP’s steep decline and break of 0.8678 support suggests that consolidation pattern from 0.8752 is extending with another falling leg. Deeper decline might be seen but downside should be contained by 38.2% retracement of 0.8354 to 0.8752 at 0.8600. On the upside, firm break of 0.8752 will resume the rise from 0.8354 towards 0.8867 fibonacci level.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it’s reversing the down trend from 0.9267 (2022 high). But even if it’s a correction, further rise is expected to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. This will remain the favored case as long as 55 W EMA (now at 0.8493) holds.