Cautious Start as US-China Trade Deadline Nears; RBA Cut, US CPI Ahead – Action Forex

Markets began the week in tight ranges, with traders reluctant to take big positions. The August 12 deadline for a US–China trade deal is a major headline risk. For now, markets are betting heavily on an extension, with another 90-day truce seen as the most probable outcome.

Still, the threat of escalation lingers. US President Donald Trump has floated the idea of higher tariffs on Chinese goods linked to Beijing’s purchases of Russian oil — mirroring his 25% additional tariffs on India for similar ties. Such measures would raise the stakes in the talks, though most expect them to stay on hold this week.

Diplomacy may play a role in that calculation. A meeting between Trump and Russian President Vladimir Putin is set for Friday in Alaska, where efforts to broker a Russia–Ukraine ceasefire will be in focus. Trump could hold off on targeting China until after gauging the outcome of that meeting.

On the economic front, traders face a packed schedule: an RBA rate cut on Tuesday, US inflation readings, UK GDP, and jobs data. The overlap of geopolitical and macro drivers creates a backdrop where range trading could give way to sharp moves if headlines surprise.

FX performance this month reflects a cautious tone. Dollar sits at the bottom of the leaderboard but remains above last month’s lows, followed by Swiss Franc and Loonie. Euro is the top performer, ahead of Yen and Sterling, with Aussie and Kiwi stuck n the middle. Nevertheless, outside of EUR/CHF, all major pairs and crosses are still trapped in last month’s ranges.

In Asia, Japan is on holiday. Hong Kong HSI is up 0.12%. China Shanghai SSE is up 0.45%. Singapore Strait Times is down -0.15%.

Fed’s Bowman urges proactive rate cuts, sees three reductions this year

Fed Governor Michelle Bowman signaled strong support for beginning interest rate cuts soon, saying in a speech over the weekend that tariff-driven price increases are a “one-time effect” and should fade without derailing the path back to 2% inflation. She argued that policy should “look through” temporary inflation spikes to avoid damaging the labor market.

She called for a gradual move toward the neutral rate, warning that delaying action risks a sharper deterioration in employment and slower economic growth. Bowman stressed that a “proactive approach” now would help avoid the need for larger policy corrections later if labor conditions worsen.

Bowman’s own Summary of Economic Projections still calls for three rate cuts this year, a view she has held since December. She noted that recent labor market data reinforce this stance, while reiterating that policy is not on a preset path. Bowman was one of two Fed governors to dissent last month against holding rates at 4.25%–4.50%, along with Christopher Waller.

China’s CPI flat in July, Core at 17-month high

China’s headline CPI registered 0.0% yoy in July, slipping from June’s 0.1% yoy but avoiding the small -0.1% yoy decline economists had forecast. Core inflation picked up to 0.8% yoy, the highest since February 2023, driven largely by firmer service prices which went up 0.5% yoy. Food prices fell -1.6% yoy.

On a monthly basis, CPI rose 0.4% mom, with the statistics bureau noting visible results from measures to expand domestic demand.

PPI stayed deep in deflation at -3.6% yoy for a second month, extending its contraction streak to 34 months. The NBS attributed the weakness to seasonal factors and global trade uncertainties. On a monthly basis, PPI slipped -0.2% mom.

Bitcoin pushes for record high, fifth-wave rally faces 130k cap

Bitcoin surges past 120,000 today and is closing in on new record. Market dynamics points to a powerful short squeeze as a large liquidity pool near current levels is forcing traders with bearish bets to buy back at higher prices, adding fuel to an already rapid climb. Short sellers appear increasingly vulnerable as momentum accelerates.

Behind the rally is a significant policy shift from Washington. Last Thursday, US President Donald Trump signed an executive order permitting cryptocurrencies and other alternative assets in 401(k) retirement accounts. The decision could, in theory, unlock trillions in retirement capital for Bitcoin and other digital assets, bolstering the longer-term demand outlook.

Technically, Bitcoin is on track to break through 123,231 and extend toward the 61.8% projection of 98,418 to 123,231 from 111,889 at 127,390.

However, the current advance from 111,889 could be the fifth wave of the entire rally from 74,373. In Elliott Wave theory, wave three is almost always the strongest and cannot be the shortest of the three upward waves. That places a logical cap on upside below 100% projection at 136,927.

Medium-term channel resistance near 131,580 reinforces this potential ceiling. The 130k zone will be a critical inflection point that could limit the current rally.

RBA to cut again – finally; Heavy weight US and UK data in focus

The RBA is widely expected to trim the cash rate by 25bps to 3.60% on Tuesday, reversing last month’s surprise hold. At the July meeting, policymakers argued for a pause to assess Q2 inflation, which later showed the disinflation trend intact. Meanwhile, the sharp rise in unemployment to 4.3% in June — a three-year high — has erased lingering doubts about the need for fresh easing.

The key question now is how much more easing lies ahead. Reuters polling indicates a strong consensus for a second 25bps cut in November, taking the cash rate to 3.35% by year-end. Australia’s big four banks offer a range of forecasts. CBA and ANZ expect two cuts — August and November — to 3.35%. NAB projects three cuts extending to February, to 3.10%. Westpac foresees four by May, to 2.85%. This divergence reflects different views on how quickly unemployment will rise and how persistent inflation risks will remain.

Thursday’s July Australian employment data will be closely watched. Consensus looks for a 25.3k rise in jobs and unemployment steady at 4.3%. Any deeper labor market deterioration could shift market sentiment toward more aggressive easing expectations, though the RBA is unlikely to accelerate beyond its “measured” approach without several months of soft data.

Globally, a heavy US data calendar will dominate mid-week, with CPI, PPI, retail sales, and the University of Michigan sentiment survey. For the Fed, expectations are locked in for two 25bps cuts this year — in September and December — in line with the June dot plot. Barring a major upside surprise in this week’s CPI, there is little to stop the Fed from delivering in September.

That said, there will be one more CPI and nonfarm payrolls report before the September FOMC meeting. Those readings will capture the early economic effects of the August tariff escalation, making them pivotal in shaping the Fed’s updated projections and its rate path into 2026. For now, speculation beyond a September cut risks running ahead of the data.

In the UK, the BoE’s latest 5–4 vote to cut to 4.00% underlined the depth of division on the MPC. The interplay between growth resilience and inflation persistence will continue to dominate the BoE debate. A stronger June UK GDP and firm labor market data this week could reinforce the case for maintaining the existing pace, even as doves argue for faster cuts to counter stagnation.

Other events to watch this week include , Germany ZEW, Japan GDP, BoC’s summary of deliberation, and a batch growth data from China.

Here are some highlights for the week:

- Tuesday: Australia NAB business confidence, RBA rate decision; UK employment; Germany ZEW economic sentiment; US CPI.

- Wednesday: Japan PPI; Australia wage price index; Germany CPI final; BoC summary of deliberations.

- Thursday: Australia employment; UK GDP; Swiss PPI; Eurozone GDP revision, industrial production; US PPI, jobless claims.

- Friday: New Zealand BNZ manufacturing; Japan GDP; China industrial production, retail sales, fixed asset investment; Canada manufacturing and wholesale sales; US retail sales, Empire state manufacturing, import prices, industrial production, UoM consumer sentiment.

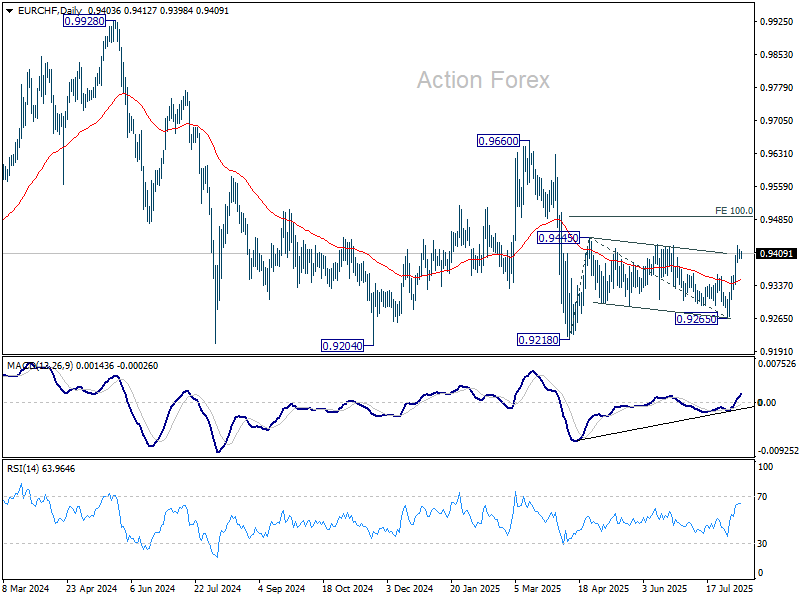

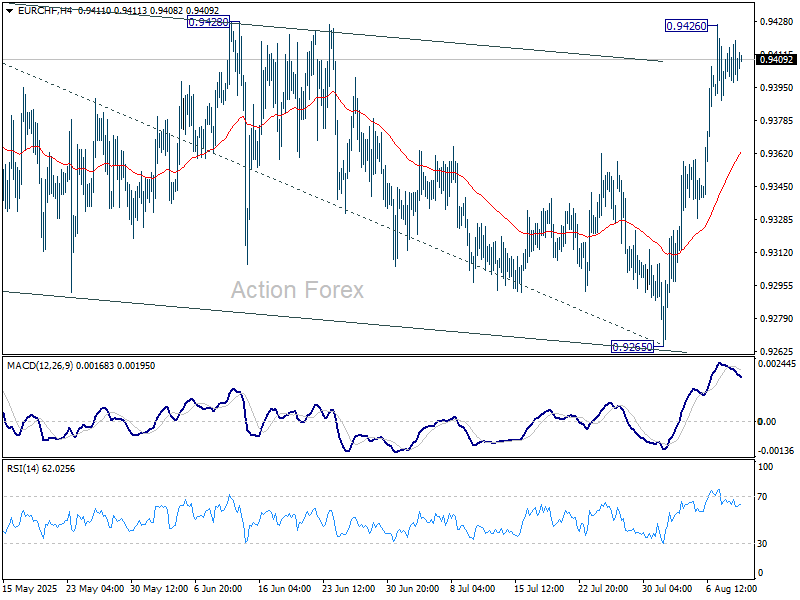

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9397; (P) 0.9409; (R1) 0.9423; More….

Intraday bias in EUR/CHF remains neutral and more consolidations could be seen below 0.9426 temporary top. As noted before, corrective pattern from 0.9445 should have completed with three waves to 0.9265. Firm break of 0.9428 should confirm this bullish case, and target 0.9445 and then 100% projection of 0.9218 to 0.9445 from 0.9265 at 0.9492. However, sustained trading below 55 4H EMA (now at 0.9362) with extend the corrective pattern with another falling leg.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside position should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.