Dollar Slips Post-CPI, Sterling Gains on Mixed UK Jobs Data – Action Forex

Dollar came under renewed selling pressure in early US session following the release of July’s CPI report. Equity markets responded positively, with stock futures pushing higher as investors focused on the softer-than-expected headline reading, largely downplaying the firmer core figure. Market reaction suggests the report does little to disrupt expectations for the Fed to deliver its anticipated September rate cut.

Futures pricing in fed funds markets even firmed slightly for a follow-up move in October. However, the policy outlook beyond September remains highly uncertain, as the impact of recent US tariff increases is expected to start filtering into the data later in the year.

In the UK, labor market data offered little to bridge the divide on the BoE’s Monetary Policy Committee. Payrolled employment has been declining steadily since late 2024. At the same time, wage growth remains well above pre-pandemic norms.

For BoE’s hawks, still-strong pay growth outweighs the risks of a weaker jobs market, while doves argue that continued payroll declines should take precedence. Complicating matters is the possibility that falling employment is not entirely demand-driven, but partly a response to rising labor costs. Either way, elevated wage growth remains a key contributor to domestic price pressures.

For Sterling, the figures were mildly supportive, as wage resilience keeps the case for a slower easing cycle alive. Market attention now turns to Thursday’s UK GDP release, which could add some decisive information to the BoE policy debate if growth data surprises in either direction.

Elsewhere, Aussie extended losses during the European session after RBA’s expected 25bps rate cut. Governor Michele Bullock acknowledged that “the cash rate might need to be a bit lower” to ensure low inflation and steady employment but emphasized the high degree of uncertainty and reiterated the Bank’s data-dependent approach. RBA appears in no hurry to cut again before the Q3 CPI release in late October, keeping November as the most likely timing for another move.

By the time of writing, Sterling is leading the majors, followed by Swiss Franc and Euro. Aussie sat at the bottom, ahead of Loonie and the greenback. Kiwi and Yen traded mixed in the middle.

US core CPI jumps to 3.1% in July, headline unchanged at 2.7%

July CPI figures showed headline inflation unchanged at 2.7% yoy, missing expectations for a rise to 2.8% yoy. Core CPI accelerated to 3.1% yoy from 2.9% yoy, topping the 3.0% yoy forecast. The annual energy index dropped -1.6% yoy, offsetting a 2.9% yoy rise in food prices.

Month-on-month, CPI increased 0.2% and core CPI rose 0.3%, both matching consensus. Shelter prices gained 0.2% and was the largest contributor to the monthly increase, while the food index was flat and energy prices declined -1.1%.

The pickup in core pressures may keep the Fed cautious. While markets still expect a September rate cut, the uptick in core CPI could limit the pace of policy easing beyond that meeting.

German, Eurozone ZEW sentiment slides sharply in August

German investor sentiment weakened sharply in August, with the ZEW Economic Sentiment Index falling from 52.7 to 34.7, well below expectations of 40.0. Current Situation Index deteriorated further from -59.5 to -68.6, also missing forecasts of -63.0.

For the Eurozone as a whole, ZEW Economic Sentiment Index dropped from 36.1 to 25.1, missing the expected 28.4. The Current Situation Index fell by -7 points to -31.2.

ZEW President Achim Wambach said the decline was partly due to disappointment over the recently announced EU–US trade deal and Germany’s poor Q2 performance. He noted that the chemical, pharmaceutical, mechanical engineering, metal, and automotive industries are facing particular strain, worsening the forward-looking view.

UK payrolled employment falls again by -8k, pay growth eases slightly

UK labor market data for July showed a slight deterioration in employment alongside a modest easing in pay growth. Payrolled employment fell by -8k, or -0.0% m/m, marking a -0.5% yoy drop compared to the same period last year. The number of payrolled employees has been trending lower since peaking in 2024, highlighting a gradual cooling in hiring momentum. Median monthly pay growth slowed marginally to 5.7% yoy from 5.8% yoy, while the claimant count dropped by -6.2k, sharply better than expectations of a 20.8k increase.

In the three months to June, unemployment rate held steady at 4.7%, in line with forecasts. Wage growth metrics were mixed. Average earnings including bonuses slowed from 5.0% to 4.6% yoy, falling short of expectations for 4.7%. Earnings excluding bonuses were unchanged at 5.0% yoy, matching forecasts.

RBA cuts to 3.60%, rate track points to one more this year

RBA lowered the cash rate by 25bps to 3.60% as widely expected, with the decision passed on a unanimous vote. The new forecasts signaled room for one more cut this year, two in 2026, and a hike in 2027.

Updated economic projections showed inflation forecasts unchanged, with year-end CPI at 3.0% in 2025, 3.1% in 2026, and 2.5% in 2027. Trimmed mean inflation was also left steady at 2.6% for 2025 and 2026, easing to 2.5% in 2027.

The growth outlook, however, was revised notably lower. Year-average GDP growth for 2025 was cut from 1.9% to 1.6%, and for 2026 from 2.2% to 2.1%, with 2027 projected at 2.0%.

The forecasts are based on interest rate assumptions of 3.4% in 2025, 2.9% in 2026, and 3.1% in 2027 — implying scope for one more cut this year, two in 2026, followed a hike in 2027.

In its statement, RBA noted that uncertainty in the global economy remains elevated. While recent developments have brought “a little more clarity” on the scope of US tariffs and the policy responses from other countries, the Bank expects that “more extreme outcomes are likely to be avoided.”

Even so, trade policy uncertainty is still expected to weigh on global activity and inflation, with the risk that households and firms delay spending until there is greater clarity. The RBA said these effects will likely continue to drag on the Australian economy “for a period”.

NAB survey shows rising Australian business confidence, pockets of inflation pressure

Australia’s NAB Business Confidence index rose from 5 to 7 in July, and moving just above the long-run average of 5. NAB noted that confidence has been trending higher despite elevated global uncertainty.

Business Conditions slipped from 7 to 5, with weakness seen across all subcomponents. Trading conditions fell from 14 to 11, profitability from 4 to 2, and employment from 4 to 1. While the pullback follows strong gains in June, NAB noted conditions have retained much of last month’s improvement.

Price indicators highlighted ongoing inflationary pressures in pockets of the economy. Labor cost growth accelerated from 1.3% to 2.1% in quarterly equivalent terms. Purchase costs edged up from 1.3% to 1.5%. Final product price growth strengthened from 0.5% to 0.9%, and retail price growth climbed from 0.5% to 1.1%.

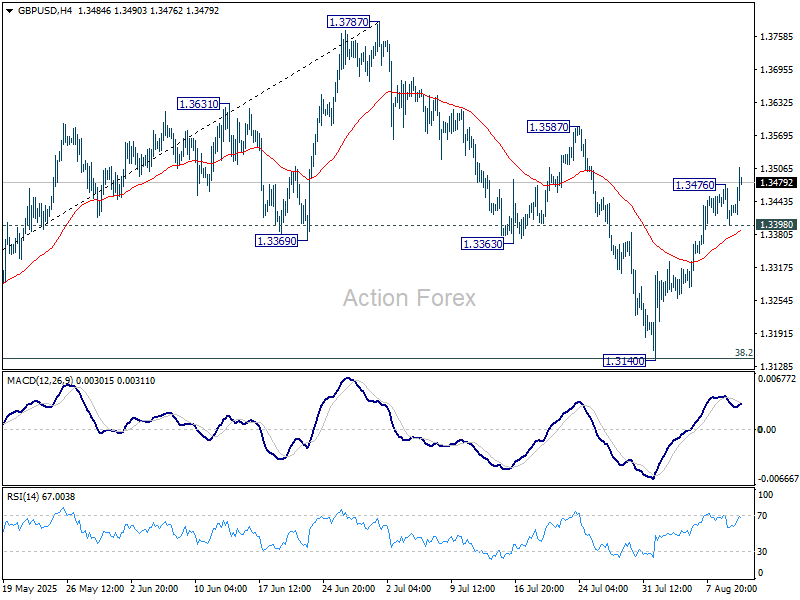

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3396; (P) 1.3436; (R1) 1.3473; More…

GBP/USD’s rise from 1.3140 resumed after brief retreat and intraday bias is back on the upside for 1.3587 resistance. Correction from 1.3787 should have completed with three waves down to 1.3140. Firm break of 1.3587 will bring retest of 1.3787 high. On the downside, below 1.3398 minor support will turn intraday bias neutral and dampen the bullish case.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3068) holds, even in case of deep pullback.