Greenback Leads Ahead of Trump’s China Tariff Call, RBA Cut in Focus – Action Forex

Dollar rebounded strongly as US session begins, despite a day largely devoid of fresh headlines or major data. Traders are looking ahead to a week dominated by trade, geopolitical, and central bank risks, particular with the August 12 US–China tariff deadline now in sharp focus.

So far, US President Donald Trump has offered little clarity on whether he will extend the current truce. Following the latest bilateral meeting in Stockholm in July, Beijing struck an optimistic tone, signalling that both sides were working toward a 90-day extension. US negotiators, however, have left the decision squarely in Trump’s hands.

A potential deal could see China committing to increase purchases of US goods — particularly energy, agricultural products, and, if permitted, semiconductors and chipmaking equipment. Trump, in a Sunday post, pressed for China to “quickly quadruple its soybean orders.”

One sticking point remains China’s purchases of Russian oil, which Trump has threatened to punish with additional tariffs. Whether he acts on that threat may hinge on the outcome of his summit with Russian President Vladimir Putin in Alaska later this week, where a possible Russia–Ukraine ceasefire is the main focus.

Attention is also on the widely expected RBA rate cut in the upcoming Asian session. The central bank left rates unchanged last month, with Governor Michele Bullock framing the decision as a matter of “timing rather than direction,” pending more evidence that inflation was falling.

The latest quarterly data from the ABS showed headline inflation easing to 2.1% from 2.4%, and trimmed mean inflation slipping to 2.7% from 2.9% — both within the 2–3% target band. The conditions should be well set for RBA to resume policy easing.

Yet policy calls are complicated by the RBA’s restructured Monetary Policy Board, which since April has comprised nine members: three internal (Bullock, Deputy Governor Andrew Hauser, and Treasury Secretary Steve Kennedy) and six external members.

With external members holding the majority and few making public remarks, consensus-building is opaque. That lack of visibility contributed to last month’s surprise 6–3 vote to hold rates steady. While inflation data now give the RBA room to cut, the internal–external split adds an element of uncertainty to Tuesday’s decision.

For the day so far, Dollar leads the major currency pack, followed by Yen and Euro. Kiwi is the weakest performer, ahead of the Swiss Franc and Aussie. Sterling and Loonie are trading in the middle.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is down -0.17%. CAC is down -0.24%. UK 10-year yield is down -0.039 at 4.565. Germany 10-year yield is up 0.004 at 2.693. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.19%. China Shanghai SSE rose 0.34%. Singapore Strait Times fell -0.17%.

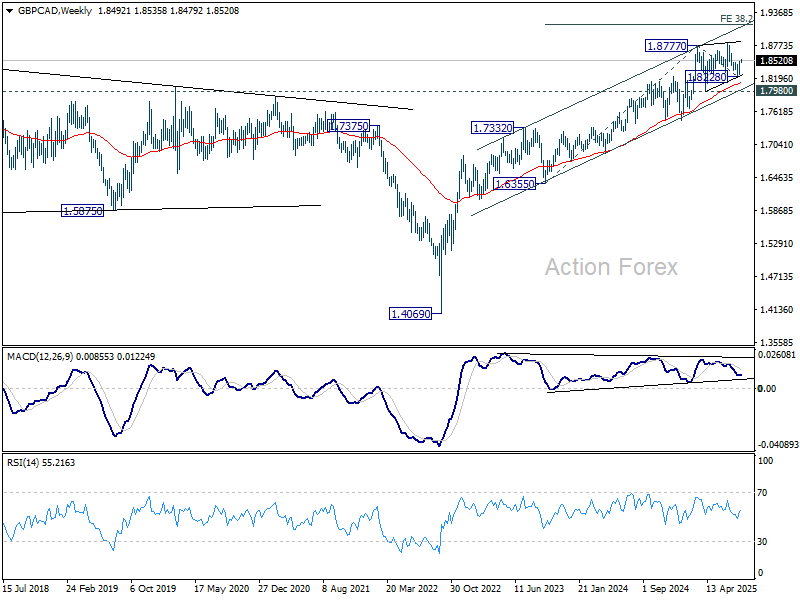

GBP/CAD rising towards 1.8830 as UK jobs and GDP awaited

GBP/CAD built on last week’s strong rebound as trading opened this week, with technical signals pointing to a retest of the recent high at 1.8830 as next step. The near-term direction will hinge partly on UK data, with employment figures due Tuesday and June GDP on Thursday.

Last week’s narrow 5–4 BoE vote to cut the Bank Rate to 4.00% highlighted the divide within the MPC, and the interplay between economic resilience and sticky inflation will remain the key driver.

Market consensus still favors a gradual “one cut per quarter” easing path from the BoE. A solid GDP print combined with firm labor market data — especially upside surprises in wage growth — could strengthen the hawkish camp’s argument to keep the pace steady, if not slower.

Technically, GBP/CAD’s break of 1.8484 resistance confirms that the fall from 1.8830 bottomed at 1.8228. The corrective pattern from 1.8777 also appears to have completed a three-wave correction at that low. Further rise should be seen to retest 1.8830 next. Firm break there will resume larger up trend to 38.2% projection of 1.6355 to 1.1877 from 1.8228 at 1.9153.

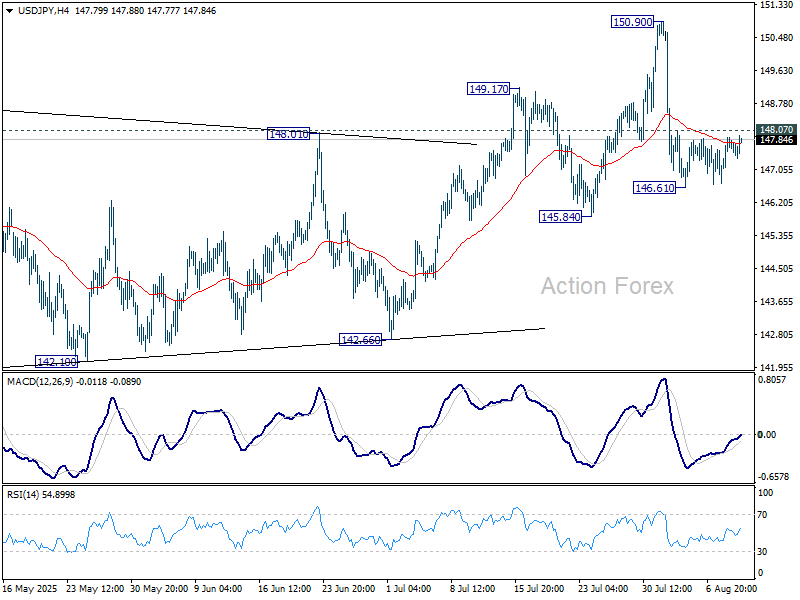

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.00; (P) 147.45; (R1) 148.18; More…

USD/JPY recovers mildly today but stays below 148.07 minor resistance. Intraday bias remains neutral at this point. Intraday bias in USD/JPY stays neutral and outlook is unchanged. As long as 145.84 support holds, larger rebound from 139.87 is still expected to continue. On the upside, above 148.07 minor resistance will bring retest of 150.90 high first. However, decisive break of 145.84 will indicate near term bearish reversal and target 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.