Loonie Dips After CPI Miss, Attention Turns to RBNZ – Action Forex

Canadian Dollar weakened broadly in early US session after inflation came in slightly below expectations. The data miss was modest, but enough to put the Loonie under pressure in otherwise quiet markets. The softer reading is not significant enough to force an immediate policy response from the BoC. Nor does it resolve concerns about sticky underlying inflation, with core measures still elevated.

Still, the lack of any resurgence in inflation allows policymakers to focus more squarely on risks to growth and employment. This backdrop could make it easier for the BoC to deliver another cut in September if incoming data — particularly on the labor market — shows further weakness.

In broader currency market, risk sentiment remains sluggish. Kiwi, Aussie, and Loonie are the weakest performers on the day so far, while Swiss Franc leads gains, followed by Euro and Yen. Sterling and Dollar are mixed in the middle of the pack.

That said, outside of a few Loonie and Aussie crosses, most major pairs remain trapped inside last week’s ranges. Trading conditions are subdued as investors avoid making large bets ahead of the Jackson Hole Symposium later in the week, where Fed commentary is expected to provide direction.

Looking forward, focus will first shifts to RBNZ’s policy decision in the coming Asian session. A 25bps cut to 3.00% is widely expected, but guidance will be key. Markets and economists remain split on whether the easing cycle ends here or if further cuts will follow into 2026. The tone of the statement will be scrutinized for clues on the next steps.

In Europe, at the time of writing, FTSE is up 0.34%. DAX is up 0.30%. CAC is up 1.05%. UK 10-year yield is down -0.007 at 4.736. Germany 10-year yield is up 0.004 at 2.771. Earlier in Asia, Nikkei fell -0.38%. Hong Kong HSI fell -0.21%. China Shanghai SSE fell -0.02%. Singapore Strait Times rose 0.69%. Japan 10-year JGB yield rose 0.026 to 1.597.

Canada CPI slows to 1.7% on gasoline drop, core still elevated

Canada’s headline CPI eased to 1.7% yoy in July, down from 1.9% yoy and below expectations for no change. The decline was driven by a sharp -16.1% yoy drop in gasoline prices, deepening from June’s -13.4% yoy. Excluding gasoline, CPI held steady at 2.5% yoy, in line with the prior two months. On a monthly basis, CPI rose 0.3% mom, matching forecasts.

Core measures delivered a mixed picture. CPI median ticked up to 3.1% yoy, as expected, while CPI trimmed held at 3.0% yoy. CPI common stayed at 2.6% yoy, a touch softer than anticipated rise to 2.7% yoy. Together, the readings show inflation has not accelerated, though underlying pressures remain sticky.

The figures reinforce the view that while headline inflation is cooling, the BoC cannot declare victory yet. Policymakers must weigh the relief from falling energy costs against stubborn core pressures. That balance will be crucial in shaping whether the Bank resumes easing at the September meeting or holds back to assess further data.

Australia’s Westpac consumer sentiment hits 3.5-year high on RBA boost

Australian consumer confidence surged in August, with the Westpac index rising 5.7% mom to 98.5, the strongest reading since early 2022. Westpac attributed the rebound to RBA’s recent rate cuts, noting that a “long period of pessimism” among households may finally be drawing to a close. Consumers are less worried about their finances and more willing to take a cautiously positive view on the economy.

While policy easing is clearly helping, Westpac said the recovery is still fragile. Sustaining gains will likely require further RBA support, though there is no urgency to cut again at the September 29–30 meeting. With inflation well within the target range and unemployment low, the Board has room to wait and respond to incoming data.

On balance, Westpac expects RBA to hold steady in September before delivering another 25bp rate cut in November.

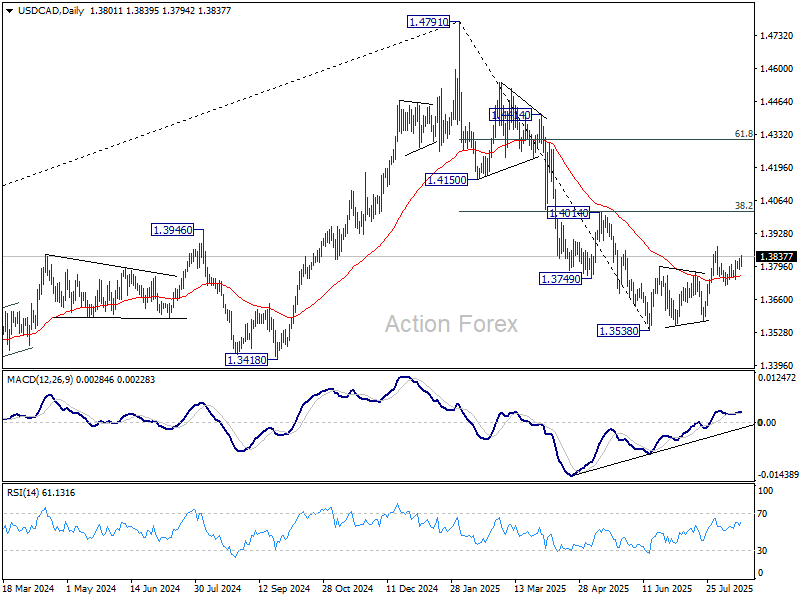

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3780; (P) 1.3806; (R1) 1.3828; More…

USD/CAD rebounds further today but stays below 1.3878 resistance. Intraday bias remains neutral first. On the upside, firm break of 1.3878 will resume the corrective rebound from 1.3538 with another rising leg. Intraday bias will be back to the upside for 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017). On the downside, though, below 1.3781 will turn bias to the downside to extend the fall from 1.3878 through 1.3720 support.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.