Trump-Zelenskyy Meeting Shrugged Off, Canada CPI May Break Lull – Action Forex

The forex market continues to trade without conviction, with major pairs confined to last week’s ranges. Traders are largely in wait-and-see mode, with the Jackson Hole Symposium at the end of the week expected to provide the next significant catalyst as Fed officials weigh in on the September policy outlook.

Still, brief bursts of volatility could emerge from data in the interim. Today’s Canada CPI release is one such event. Headline inflation is expected to hold steady, but core measures may firm. The outcome will be crucial for BoC, which has paused after seven consecutive cuts but remains split on whether more easing is needed in September.

On the geopolitical front, attention has been high but market reaction muted. US President Donald Trump hosted Ukrainian President Volodymyr Zelenskyy and European leaders at the White House in an effort to build momentum toward ending the war in Ukraine. Yet financial markets have largely shrugged off the developments.

Trump revealed he has begun arranging a meeting between Russian President Vladimir Putin and Zelenskyy, with a trilateral summit involving himself to follow. He described the initiative as an “early step” in a war now nearing its fourth year. Expectations are modest, but the symbolic breakthrough has been noted.

Zelenskyy added that a package of security guarantees for Ukraine is being prepared, likely including significant U.S. weapons purchases, and should be formalized within 10 days. Trump confirmed that guarantees would be provided by European countries in coordination with Washington.

In Asia, at the time of writing, Nikkei is down -0.03%. Hong Kong HSI is up 0.19%. China Shanghai SSE is up 0.30%. Singapore Strait Times is up 0.55%. China Shanghai SSE is up 0.028 at 1.600. Overnight, DOW fell -0.08%. S&P 500 fell -0.01%. NASDAQ rose 0.03%. 10-year yield rose 0.013 to 4.341.

Australia’s Westpac consumer sentiment hits 3.5-year high on RBA boost

Australian consumer confidence surged in August, with the Westpac index rising 5.7% mom to 98.5, the strongest reading since early 2022. Westpac attributed the rebound to RBA’s recent rate cuts, noting that a “long period of pessimism” among households may finally be drawing to a close. Consumers are less worried about their finances and more willing to take a cautiously positive view on the economy.

While policy easing is clearly helping, Westpac said the recovery is still fragile. Sustaining gains will likely require further RBA support, though there is no urgency to cut again at the September 29–30 meeting. With inflation well within the target range and unemployment low, the Board has room to wait and respond to incoming data.

On balance, Westpac expects RBA to hold steady in September before delivering another 25bp rate cut in November.

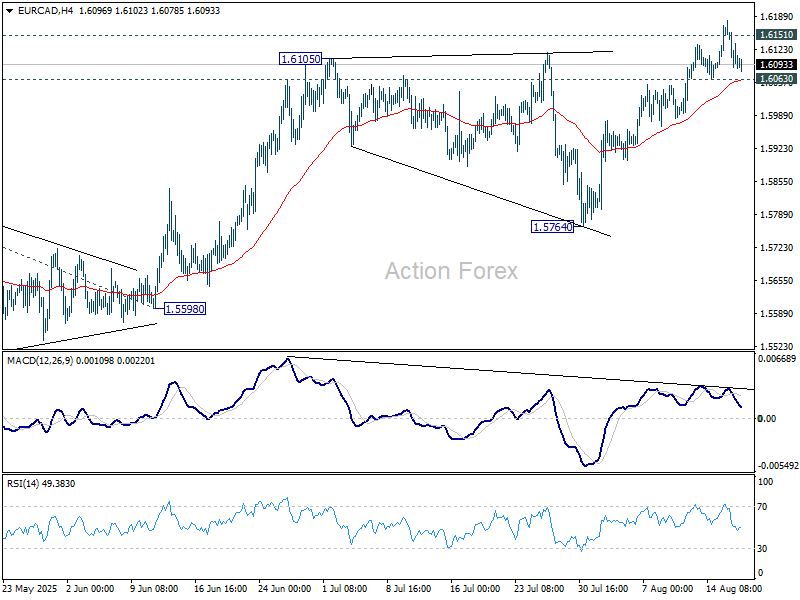

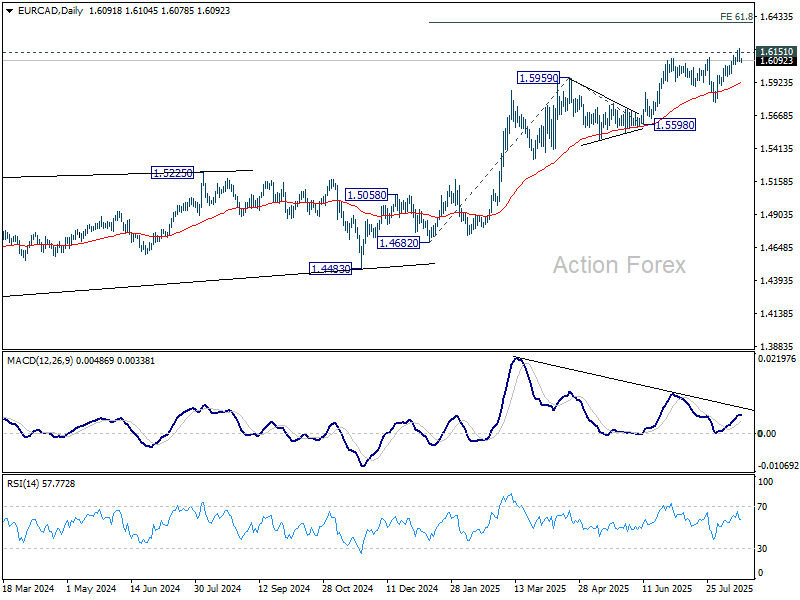

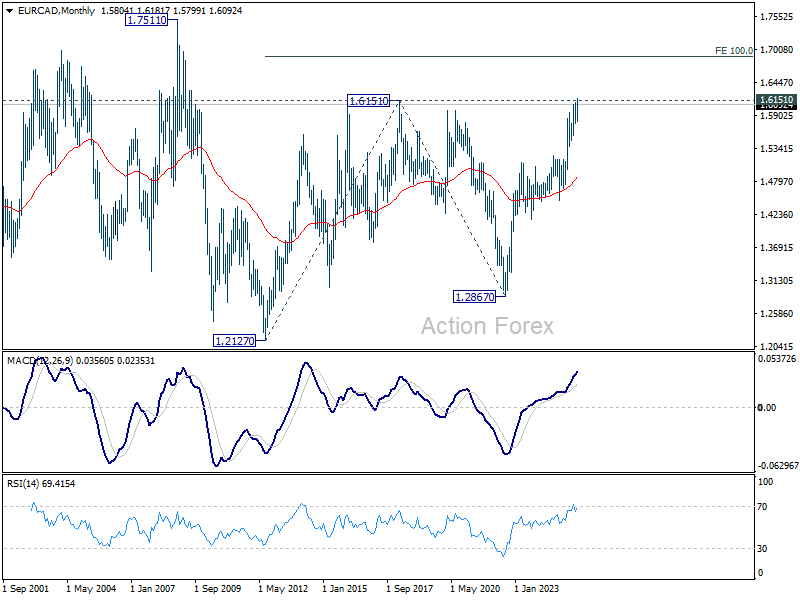

Canada CPI to steer BoC next cut? EUR/CAD risks correction

Canadian inflation data is today’s key release, with headline CPI expected at 1.9% yoy in July, unchanged from June. More attention may fall on core measures, with CPI common forecast to tick up to 2.7% yoy from 2.6% yoy. The figures arrive at a delicate juncture for BoC, which has cut rates seven times since June 2024 but held steady at 2.75% in its last three meetings.

Expectations for a September rate cut remain divided. The BoC’s July summary of deliberations revealed a split council: some members argued that enough easing has already been delivered, while others highlighted economic slack and warned further support may be needed if labor market conditions soften. The uncertainty has left markets reluctant to price in an imminent move with conviction.

Tariff risks complicate the picture. Policymakers noted in July that U.S. tariffs and the rewiring of global trade are directly influencing inflation and broader growth dynamics. The latest decision to hold rates came just before Trump ratcheted Canadian tariffs up to 35%, though with exemptions for CUSMA-compliant goods.

Despite headwinds, BoC acknowledged some resilience in the domestic economy. Yet policymakers remain wary of timing: additional easing might only take hold as demand begins to recover, raising the risk of fueling price pressures rather than cushioning growth.

For now, inflation remains close to target and the economy has shown pockets of resilience, but the balance of risks is still fragile. Whether today’s CPI confirms contained price growth or points to renewed pressures could influence whether BoC holds steady again in September.

Technically, EUR/CAD is starting to lose momentum as it’s struggling to sustain above 1.6151 key resistance (2018 high). Immediate focus is on 1.6063 minor support. Firm break there will indicate short term topping and bring deeper pullback to 55 D EMA (now at 1.5910).

But the overall outlook will stay bullish as long as 1.5764 support holds. The larger up trend is expected to resume sooner or later. Once the 1.6151 resistance is cleared decisively, next target is 61.8% projection of 1.4682 to 1.5959 from 1.5598 at 1.6387.

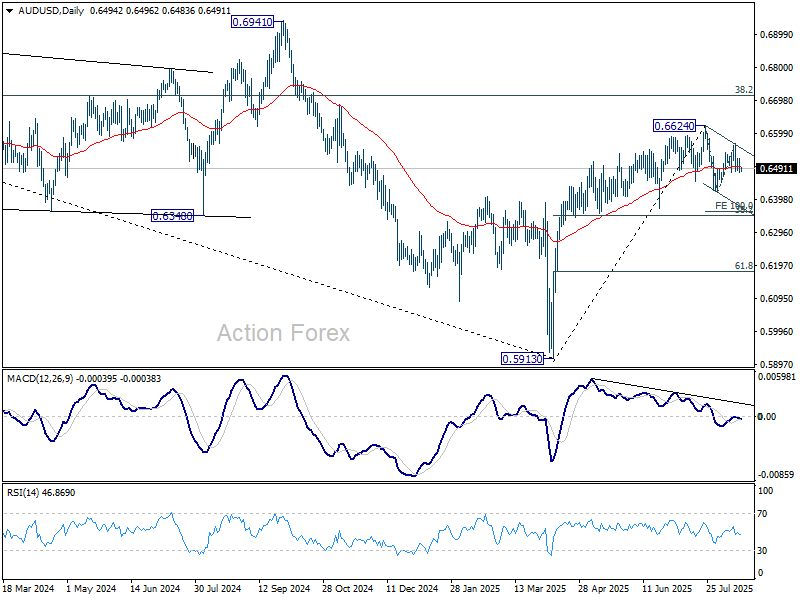

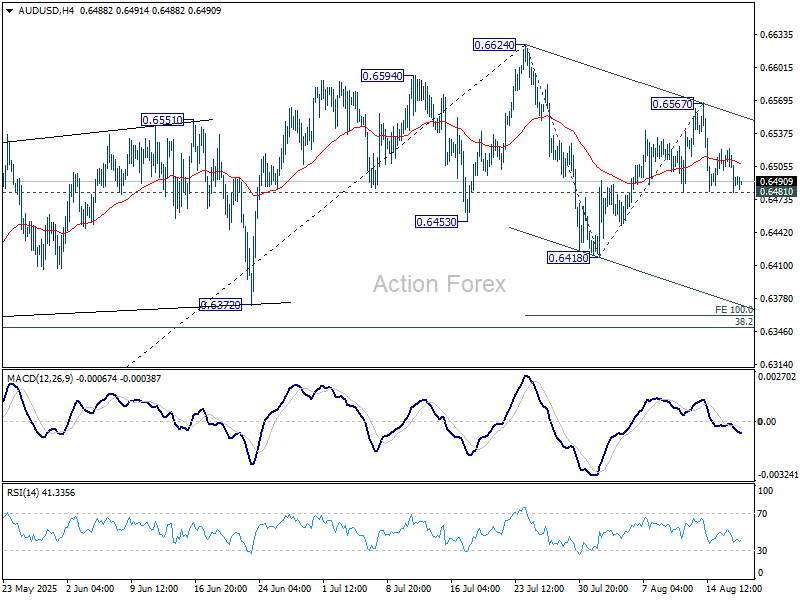

AUD/USD Daily Report

Daily Pivots: (S1) 0.6475; (P) 0.6499; (R1) 0.6517; More...

Intraday bias in AUD/USD stays neutral, and focus is back on 0.6841 support with current dip. Firm break there will suggest that corrective pattern from 0.6624 is already extending with a third leg. Intraday bias will be back on the downside for 0.6418 support first, and then 38.2% retracement of 0.5913 to 0.6624 at 0.6352. On the upside, though, above 0.6567 will resume the rebound from 0.6418 to 0.6624 high.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).