Volatile Day as Yen Rebounds, Sterling Holds Firm, Kiwi Slumps – Action Forex

There are three themes dominating currency markets today: a stronger rebound in the Yen, firming Sterling, and a sharp tumble in Kiwi. Moves are being shaped by local economic drivers as well as shifting central bank expectations, setting the stage for a cautious but active session.

Yen’s rally came alongside a steep pullback in Japanese equities, with Nikkei falling more than -1.4%. The selloff partly reflected profit-taking after the index hit fresh record highs earlier this week. Weak trade data added pressure, as exports contracted at the steepest pace since early 2021.

Autos were at the center of the decline, with shipments to the U.S. slumping heavily. There may be hope for a rebound later this year thanks to the U.S.–Japan trade deal that lowered reciprocal tariffs. But for now, investors are wary. The combination of equity weakness and poor trade data has fueled safe-haven demand for Yen.

Sterling, meanwhile, is holding firm after another upside surprise on inflation. July’s data showed both goods and services prices accelerating, suggesting that tariffs are still feeding through to consumers while domestic pressures intensify. Coupled with last week’s solid GDP numbers, the backdrop leans toward the hawks within the BoE.

Markets are beginning to doubt the likelihood of another BoE cut in November if inflation continues to surprise on the upside. Policymakers may be forced to slow their already gradual easing cycle, particularly if price momentum proves sticky heading into the autumn.

In contrast, Kiwi has dropped sharply after RBNZ cut the OCR to 3.00% with a dovish bias. Updated forecasts point to scope for one more cut this year and another in early 2026. The decision was also notable for its split: two members favored a 50bp cut, highlighting a shift toward deeper easing if growth weakens further.

Overall, Yen is the strongest performer so far today, followed by Dollar and Sterling. Kiwi is the weakest, trailed by Euro and Aussie, with Swiss Franc and Loonie in the middle.

Looking ahead, attention turns to FOMC minutes, which may reveal whether more Fed officials were sympathetic to the dovish camp after Governor Christopher Waller and Michelle Bowman dissented in July in favor of an immediate cut.

In Asia, Nikkei fell -1.49%. Hong Kong HSI is down -0.09%. China Shanghai SSE is up 0.62%. Singapore Strait Times is up 0.28%. Japan 10-year JGB yield is up 0.012 at 1.610. Overnight, DOW rose 0.02%. S&P 500 fell -0.59%. NASDAQ fell -1.46%. 10-year yield fell -0.039 to 4.302.

UK CPI jumps to 3.8%, services inflation stays hot at 5%

UK inflation accelerated more than expected in July, with headline CPI rising to 3.8% yoy from 3.6% yoy, surpassing forecasts of 3.7% yoy and marking the highest level since early 2024. The biggest driver was transport costs, particularly higher airfares, which made the largest contribution to the monthly rise in annual rates.

Breakdown data showed broad-based strength. CPI goods inflation climbed to 2.7% yoy from 2.4% yoy, while CPI services surged to 5.0% yoy from 4.7% yoy. Meanwhile, core CPI edged up from 3.7% yoy to 3.8% yoy, topping expectations and matching the headline pace, highlighting persistent underlying pressures.

For BoE, the data poses a challenge. The uptick in both headline and core inflation risks slowing the recent easing cycle, as policymakers balance still-high inflation against weaker economic growth momentum. Markets may scale back expectations for near-term cuts if the stickiness persists.

RBNZ cuts, opens door to more, NZD/USD diving towards 0.58

RBNZ delivered a 25bps cut to the Official Cash Rate, lowering it to 3.00% as widely expected. A more sizeable 50bps rate cut was discussed during the meeting. Policymakers maintained an easing bias, noting that “if medium-term inflation pressures continue to ease as expected, there is scope to lower the OCR further.”

The new projections point to the OCR dropping to 2.7% by Q4 2025, then settling between 2.5% and 2.6% in 2026 before edging back toward 2.7–2.8% in 2027. This outlook effectively signals room for one additional cut this year and another in early 2026.

The Bank highlighted ongoing slack in the economy and easing domestic inflation, projecting headline inflation to return to the 2% midpoint of target by mid-2026. However, New Zealand’s recovery has stalled, with household and business spending constrained by global policy uncertainty, weaker employment, higher costs for essentials, and falling house prices.

NZD/USD dives through 0.5855 support after the announcement to resume the decline from 0.6119. Next target is 50% retracement of 0.5484 to 0.6119 at 0.5802. As the decline is currently seen as a corrective move, there might be some support form 0.5802 to bring rebound. However, firm break of 0.5906 support turned resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

Also, decisive break of 0.5802, coupled with downside acceleration through the near term falling channel, will suggest that NZD/USD is indeed reversing the whole rise from 0.5484. That could pave the way through 61.8% retracement of 0.5727 to wards 0.5484 low.

Japan exports slump -2.6% yoy in July, U.S. auto shipments hit hard

Japan’s exports fell -2.6% yoy in July to JPY 9.36 trillion, the sharpest drop since February 2021, driven by weaker demand from its two largest markets, the U.S. and China. Exports to the U.S. slid -10.1% yoy, with auto shipments plunging -28.4% yoy, a steeper decline than June’s -26.7%. Shipments to China also contracted -3.5% yoy, though exports to Hong Kong surged nearly 18% yoy.

The latest weakness highlights how external headwinds continue to weigh on Japan’s trade sector. While Tokyo reached a deal with Washington on July 22 to reduce reciprocal tariffs to 15% from 25%, the benefits will not be reflected until the August trade data. For now, auto exports remain a key drag on overall performance.

Imports fell -7.5% yoy to JPY 9.48 trillion, leaving Japan with a JPY 118 billion deficit. In seasonally adjusted terms, exports slipped -0.2% mom, while imports rose 0.4% mom, pushing the deficit wider to JPY 303 billion.

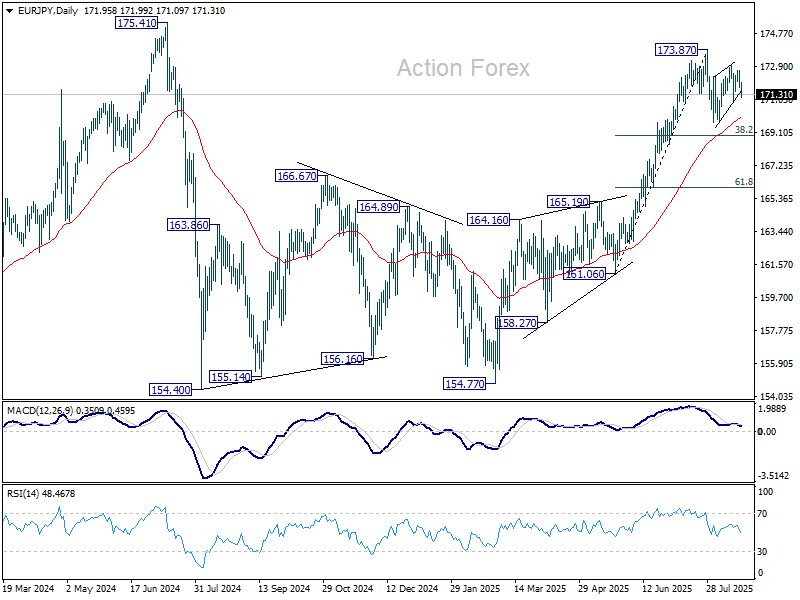

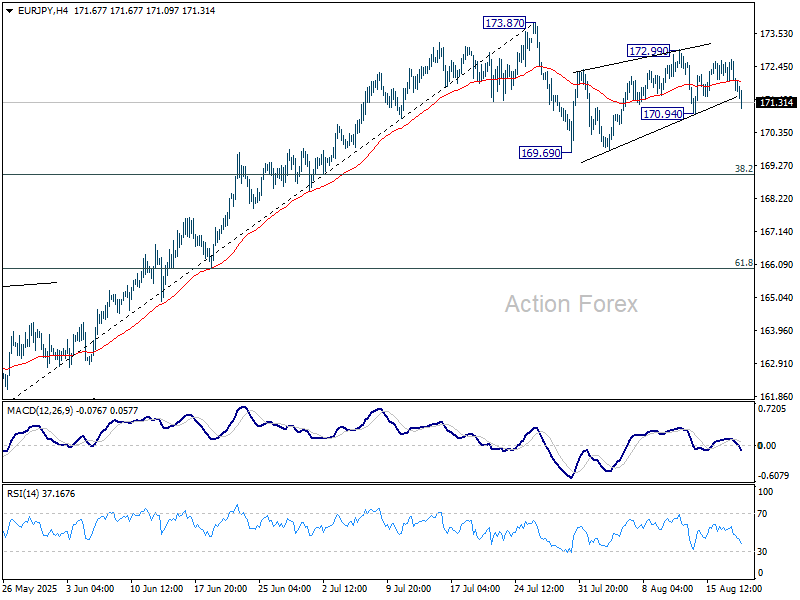

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.56; (P) 172.14; (R1) 172.57; More…

Immediate focus is now on 170.94 support in EUR/JPY with today’s decline. Firm break there will suggest that the corrective pattern from 173.87 has started the third leg. Intraday bias will be turned back to the downside for 169.69 support, and possibly below. But downside should be contained by 38.2% retracement of 161.06 to 173.87 at 168.97 to bring rebound. On the upside, above 172.99 will bring retest of 173.87.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break of 154.77 will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 169.95) will delay this bullish case.