Yen Dips in Sluggish Markets, Eyes on Trump-Zelenskyy Talks – Action Forex

Trading across global markets is subdued today, with Asia and the West pulling in different directions. Japan’s Nikkei hit a fresh record high, but European equities and US futures slipped modestly, leaving overall sentiment sluggish.

Some attention is turning to Washington, where US President Donald Trump hosts Ukrainian President Volodymyr Zelenskyy, followed by joint talks with European leaders. The effort is framed as a bid to advance toward ending the war in Ukraine, but expectations remain muted. Observers stress that negotiations involving Russia, Ukraine, Europe, and the US are still in their infancy. Trump’s recent meeting with Putin showed how entrenched positions remain, making it clear that the road to even a ceasefire will be long and fraught. Markets are tempering hopes accordingly.

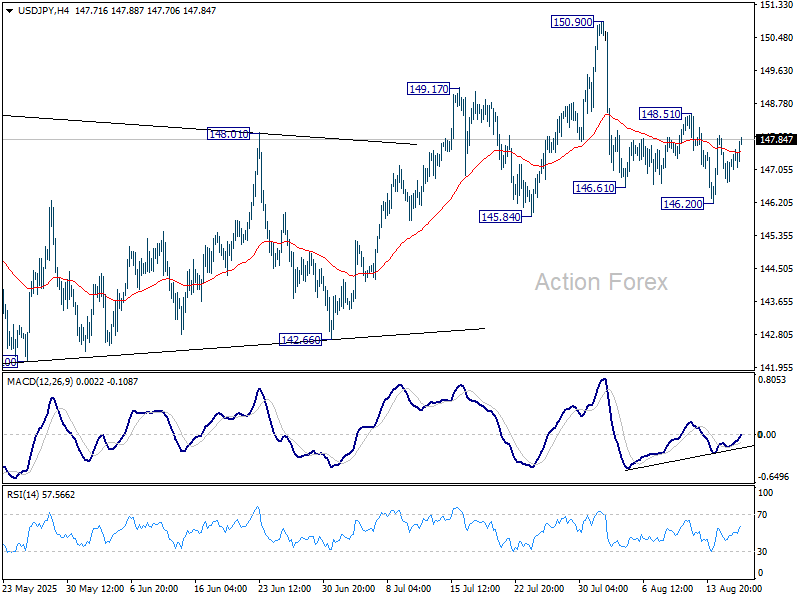

In FX, Yen came under renewed selling pressure as the US session commences, making it the day’s weakest performer, followed by Euro and Sterling. A focus is on whether USD/JPY can break above 148.51 resistance, which would confirm the pullback from 150.90 has ended and open the way for a broader Yen decline. By contrast, Loonie is leading gains, followed by Kiwi and Aussie. Dollar and Swiss Franc are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is down -0.32%. CAC is down -0.80%. UK 10-year yield is up 0.002 at 4.698. Germany 10-year yield is down -0.029 at 2.761. Earlier in Asia, Nikkei rose 0.77%. Hong Kong HSI fell -0.37%. China Shanghai SSE rose 0.85%. Singapore Strait Times fell -1.02%. Japan 10-year JGB yield rose 0.006 to 1.572.

EU exports stagnate as US, China imports surge

Eurozone recorded a EUR 7.0B surplus in goods trade in June, as modest export growth was outpaced by stronger imports. Exports ticked up 0.4% yoy to EUR 237.2B, while imports jumped 6.8% yoy to EUR 230.2B.

Across the EU as a whole, goods surplus narrowed to EUR 8.0B. Exports held steady at EUR 213.7B, but imports rose 6.4% yoy to EUR 205.7B.

Trade with major partners showed contrasting trends. EU exports to the US and China dropped sharply, down -10.3% yoy and -12.7% yoy, while exports to the UK grew 7.4% yoy.

At the same time, imports from the US and China surged by 16.4% yoy and 167% yoy respectively, while UK shipments into the EU declined -3.6% yoy.

NZ BNZ services uptick to 48.9, contraction persists

New Zealand’s BusinessNZ Performance of Services Index improved slightly in July, rising from 47.6 to 48.9. But the sector remained in contraction for the sixth consecutive month. Also, the latest reading is still well below the long-run survey average of 52.9.

Details showed mixed conditions. Activity/Sales stayed in contraction at 47.5, and New Orders stalled at 50.0. On the positive side, Inventories expanded for the second month at 51.4. Employment component slid to 47.1, extending its losing streak to 20 months.

Business sentiment, while slightly less negative, continued to reflect difficult conditions. Around 58.5% of comments were pessimistic, down from 66.2% in June. Firms pointed to declining sales, reduced spending, and persistent cost-of-living pressures. Inflation, high interest rates, weather disruptions, staffing shortages, and global uncertainty all weighed on confidence.

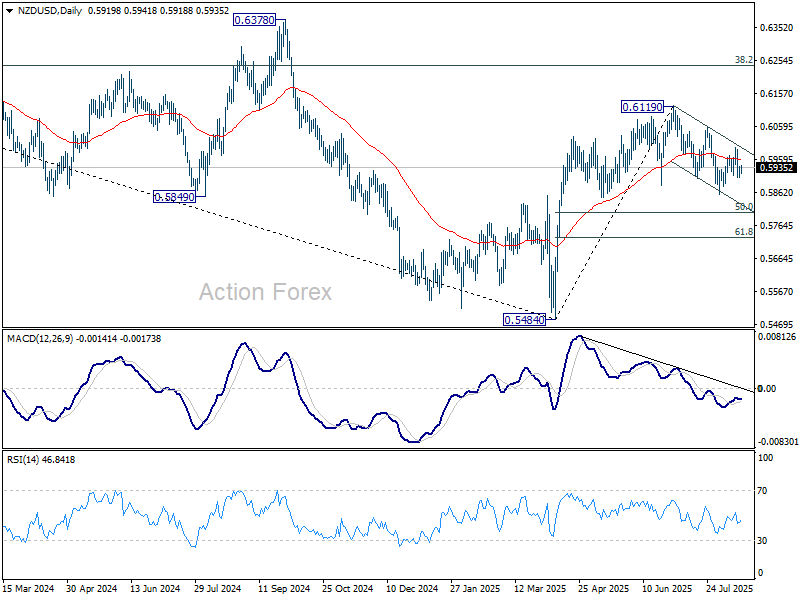

NZD/USD stuck in falling channel as RBNZ shadow board splits

NZD/USD is trading quietly within range, with investors cautious ahead of RBNZ’s policy decision this Wednesday. Market consensus is for a 25bps cut, though the NZIER Shadow Board revealed a broad spread of opinions, from a 50bps reduction to no move at all. The diversity highlights some uncertainty surrounding the policy outlook.

According to the Shadow Board, the case for a cut is backed by persistent slack in the labor market and subdued domestic activity. Still, near-term inflation pressures complicate the picture. While one board member argued for a more aggressive 50bps cut to support growth, two stressed the risks of loosening again with price pressures still elevated.

Looking further ahead, views on the OCR in 12 months are diverse, from no additional easing to further cuts required. One member sees strong commodity prices and lower rates supporting activity, with inflation potentially rising toward the top of the RBNZ’s 1–3% target band. That backdrop suggests patience may be prudent. Though, two members maintain the economy will still need further stimulus beyond August.

Technically, NZD/USD remains mildly bearish as its stays confined within the near-term falling channel. Rebound from 0.5855 appears to have topped out at 0.5995. Fall from there is seen as another leg of the decline from 0.6119.

Structurally, while the pullback from 0.6119 looks corrective, risks are skewed toward another dip. A slide to 50% retracement of 0.5484 to 0.6119 at 0.5802 is in favor before NZD/USD finds a firmer base.

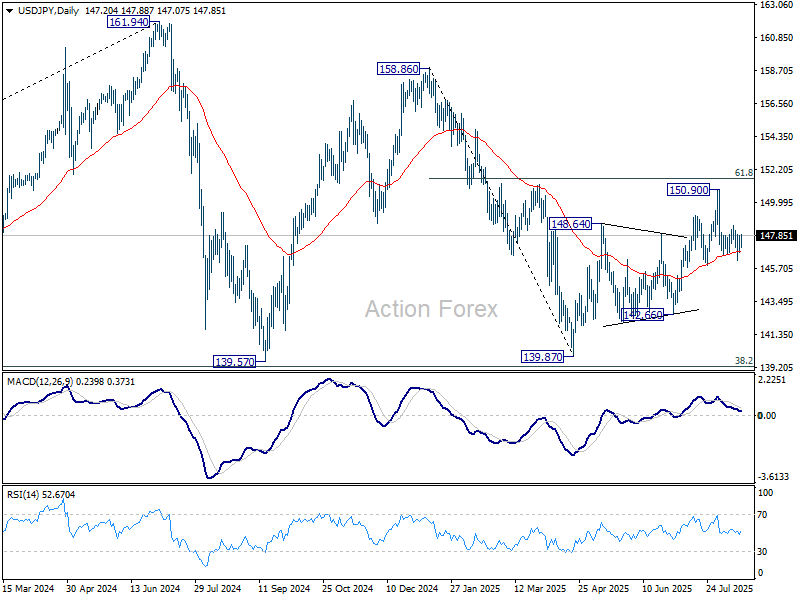

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.61; (P) 147.29; (R1) 147.83; More…

USD/JPY recovers notably in early US session but stays well inside range of 146.20/148.51. Intraday bias remains neutral. On the upside, break of 148.51 will indicate that the pullback from 150.90 has completed, and bring retest of this high. This will also keep the whole rise from 139.87 alive. However, firm break of 145.84 support will argue that the rebound from 139.87 has completed, and turn near term outlook bearish.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.