Fed Drama and Fresh Tariff Threats Sour Risk Mood – Action Forex

Markets turned risk-averse again overnight, with Wall Street weakness spilling into Asia as political and trade developments rattled sentiment. Expectations that the Fed will cut rates in September remain intact, but investors are struggling to look past threats to central bank independence and a fresh wave of tariff risks.

The flashpoint came Monday when US President Donald Trump announced he had fired Federal Reserve Governor Lisa Cook, citing alleged misconduct related to mortgage applications. Cook immediately rejected the move, saying the president had “no authority” to dismiss her and pledging to remain in her post. The confrontation has cast a cloud over the Fed just as it prepares for a pivotal September policy meeting.

The optics are striking: Cook, the first Black woman to serve on the Fed board, has become the focal point of a legal and political dispute that could test the institution’s autonomy. For markets, the drama only adds to uncertainty at a time when Fed credibility and consistency are paramount.

At the same time, Trump sharpened his trade rhetoric. He warned that countries imposing digital services taxes would face “substantial” new tariffs on exports to the U.S., along with restrictions on U.S. chip supplies. The warning targeted dozens of nations, reopening old disputes that many investors had assumed were on hold.

China was also singled out in particularly blunt terms. Trump threatened that the U.S. would impose another 200% tariff on Chinese exports if Beijing restricted shipments of rare-earth magnets to the U.S. He also boasted that U.S. withholding of Boeing aircraft parts had already grounded hundreds of Chinese planes. The comments risk destabilizing a fragile trade truce between the two economies.

In currency markets, Dollar regained its lead, emerging as the strongest currency so far this week. Aussie and Loonie followed, while the Euro, Yen, and Swiss Franc fell to the bottom of the rankings. Sterling and Kiwi traded mid-pack. Yet, despite heightened rhetoric, most major pairs remain trapped within last week’s ranges. Markets appear unwilling to chase moves until clearer direction emerges, whether from hard data or further political escalation.

In Asia, at the time of writing, Nikkei is down -0.92%. Hong Kong HSI is down -0.22%. China Shanghai SSE is down -0.21%. Singapore Strait Times is down -0.26%. Japan 10-year JGB yield is up 0.002 at 1.623. Overnight, DOW fell -0.77%. S&P 500 fell -0.43%. NASDAQ fell -0.22%. 10-year yield rose 0.015 to 4.275.

RBA minutes: Not yet possible to decide pace of further easing

Minutes of RBA’s August 11–12 meeting showed policymakers unanimously backed the 25bps cut to 3.60%, citing stronger evidence that inflation is heading sustainably toward the midpoint of the 2–3% target range. The Board agreed that full employment can be preserved while inflation continues easing, though members noted risks remain in both directions.

The central bank noted that some further reduction in cash rate likely to be needed “in the coming year”. But it also stressed that the pace of further reductions will be determined “meeting by meeting” as new data emerges. While some indicators still suggest a tight labor market and inflation projected to stay slightly above target in the medium term, private demand is recovering, supporting the case for a “gradual pace”.

At the same time, the minutes noted conditions that could justify a”slightly faster” pace of easing. If the labor market is already “in balance”, or if risks shift more clearly to the downside—whether through weaker global growth or slower employment handover—then a quicker reduction in the cash rate could be warranted to avoid undershooting inflation.

Overall, members concluded it is “not yet possible” to judge whether easing will be gradual or slightly faster. RBA left the door open for both paths, emphasizing that data will drive the speed of policy adjustments in the months ahead.

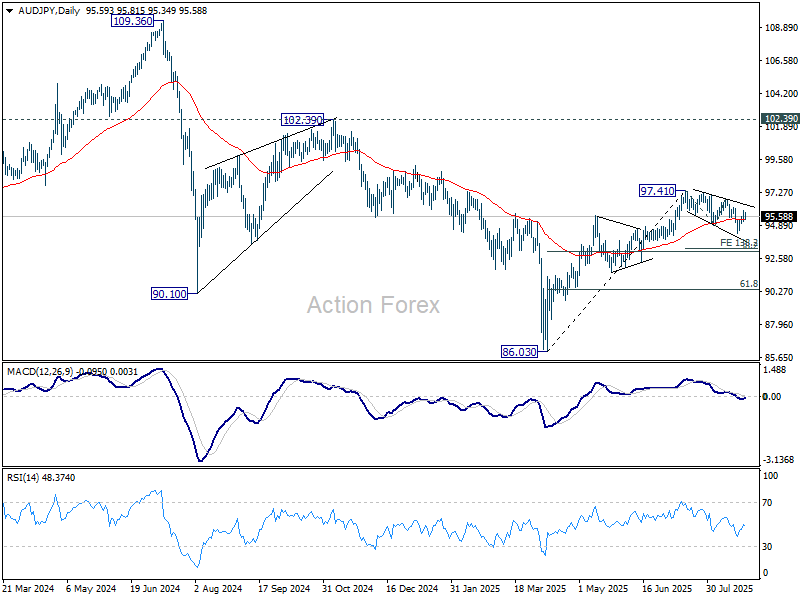

AUD/JPY’s corrective fall intact for another leg through 94.38

AUD/JPY dipped mildly after RBA’s August minutes affirmed that further easing is likely over the coming year. While the Board leaned toward a gradual pace of cuts, it made clear that a faster reduction path is possible if the labor market continues to rebalance.

RBA suggested it would not require material deterioration to quicken the pace; rather, once the job market shifts to a more balanced state, it would be appropriate to cut faster to avoid inflation undershooting target.

Technically, AUD/JPY’s pullback from 97.41, as a correction of the broader rise from 86.03, remains in motion. The rebound from 94.38 has lost momentum after stalling at 95.94, with the falling trend line (now at 96.40) likely to cap further upside attempts.

Break below 95.12 minor would signal the correction entering a fresh leg lower, with 94.38 next support. Breaking that level would extend the correction toward 138.2% projection of 97.41 to 94.88 from 96.81 at 93.31.

Though, strong support should emerge from 38.2% retracement of 86.03 to 97.41 at 93.06 to complete the correction, and bring resumption of rise form 86.03.

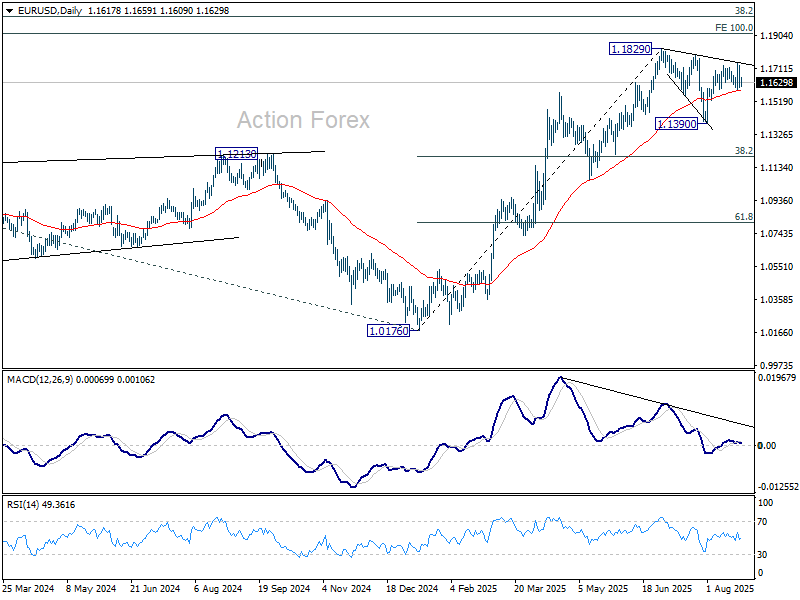

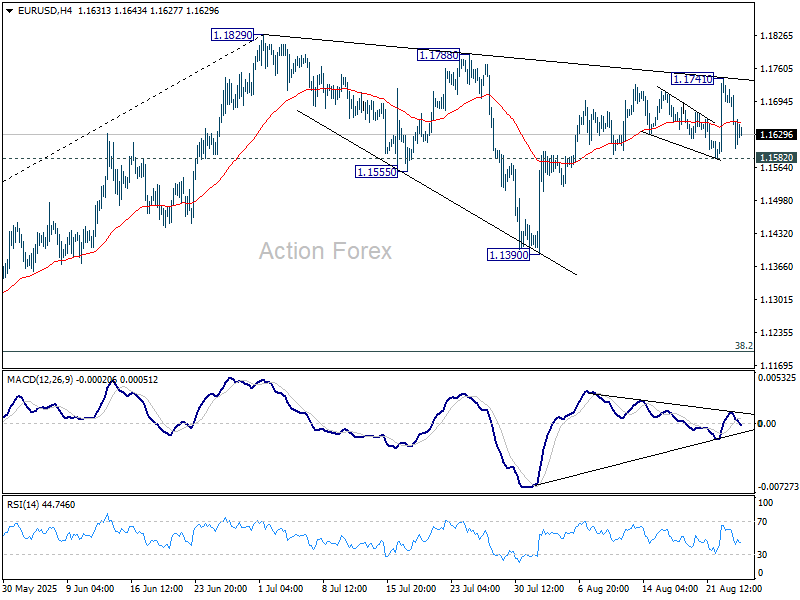

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1572; (P) 1.1650; (R1) 1.1697; More…

Intraday bias in EUR/USD is turned neutral again with current retreat. Further rise is expected as long as 1.1582 support holds. Above 1.1741 will resume the rally from 1.1390 to retest 1.1829 high. Firm break there will extend larger up trend. However, decisive break of 1.1582 will extend the corrective pattern from 1.1829 with another downleg, and target 1.1390.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.