Risk-On Tone Lifts Aussie, Pressures Yen and Franc – Action Forex

Asian investors kicked off the week on a positive note, with equities advancing after Fed Chair Jerome Powell struck a dovish tone at Jackson Hole. Gains were particularly strong in Hong Kong, though most regional markets saw upward momentum, reflecting belief that the Fed appears ready to ease again soon.

Still, market expectations have essentially reverted to where they stood before last week’s volatility. Fed fund futures are currently pricing an 87% probability of a September rate cut. Odds of a follow-up move in October stand at just 42%, while December is seen carrying more than an 80% chance of another cut.

Taken together, traders now see a high probability of two rate cuts this year—precisely the scenario already sketched out in the Fed’s June dot plot. In that sense, Powell’s speech has not materially shifted the outlook, but it has restored confidence that the central bank remains aligned with its own projections.

In currency trading, risk appetite is evident. Aussie is leading Kiwi and Loonie higher, while traditional havens—the Swiss Franc and Japanese Yen—are under pressure, followed by Euro. Sterling and Dollar sit mid-pack.

Looking ahead, the data calendar is relatively light this week. U.S. PCE inflation, Japan’s Tokyo CPI, and other price reports will offer some direction but are unlikely to shift expectations for September. The real test comes next week, when U.S. nonfarm payrolls are released. That will be the key input, alongside CPI on September 11, for the Fed’s policy decision at the September 16–17 meeting. Until then, markets may continue to trade on sentiment rather than fresh conviction.

In Asia, Nikkei rose 0.37%. Hong Kong HSI is up 2.06%. China Shanghai SSE is up 0.95%. Singapore Strait Times is up 0.17%. Japan 10-year JGB yield is flat at 1.619.

ECB’s Lagarde highlights migrant labor as key Eurozone growth support

At Jackson Hole on Saturday, ECB President Christine Lagarde credited foreign workers with playing a vital role in supporting the eurozone economy. She said migration inflows have helped counterbalance reduced working hours and weaker living standards, providing stability during a period of subdued real wage growth.

Lagarde pointed out that although foreign workers represented just 9% of the bloc’s labor force in 2022, they contributed fully half of its growth over the previous three years. “Without this contribution, labor market conditions could be tighter and output lower,” she added.

BoE’s Bailey cites falling labor participation rate as UK’s “sad story”

BoE Governor Andrew Bailey warned at Jackson Hole on Saturday that the UK faces an “acute challenge” of weak underlying growth compounded by reduced Labor force participation. He stressed that with ageing demographics unlikely to reverse, raising productivity growth must become a priority to offset the economy’s structural drag.

Bailey said the BoE has shifted its focus from long-term unemployment trends to participation rates, noting that the proportion of working-age Britons active in the Labor market remains lower than before the pandemic, unlike in most advanced economies. While he cautioned that survey data contains caveats, he argued they do not fully explain the shortfall.

Calling it a “pretty sad story for the UK,” Bailey said diminished participation leaves the UK at the bottom of global rankings. This structural weakness is also feeding into inflation concerns, with some policymakers fearing that limited Labor supply is one reason why UK inflation, at 3.8% in July, remains the highest in the G7.

BoJ’s Ueda sees tight labor market sustaining wage growth

BoJ Governor Kazuo Ueda told a Jackson Hole panel on Saturday that Japan’s labor shortages are becoming “one of our most pressing economic issues.” He highlighted that wage growth, once concentrated in large enterprises, is now spreading to smaller firms.

Ueda said that barring a major negative demand shock, “the labor market is expected to remain tight and continue to exert upward pressure on wages”. He noted that the demographic shifts set in motion since the 1980s are now driving both “acute labor shortages and persistent upward pressure on wages”

According to Ueda, these shifts are forcing supply-side adjustments, including higher participation rates, greater labor mobility, and increased capital-labor substitution. He pledged the BoJ will “continue to monitor these developments closely and incorporate our assessment of evolving supply-side conditions into the conduct of monetary policy.”

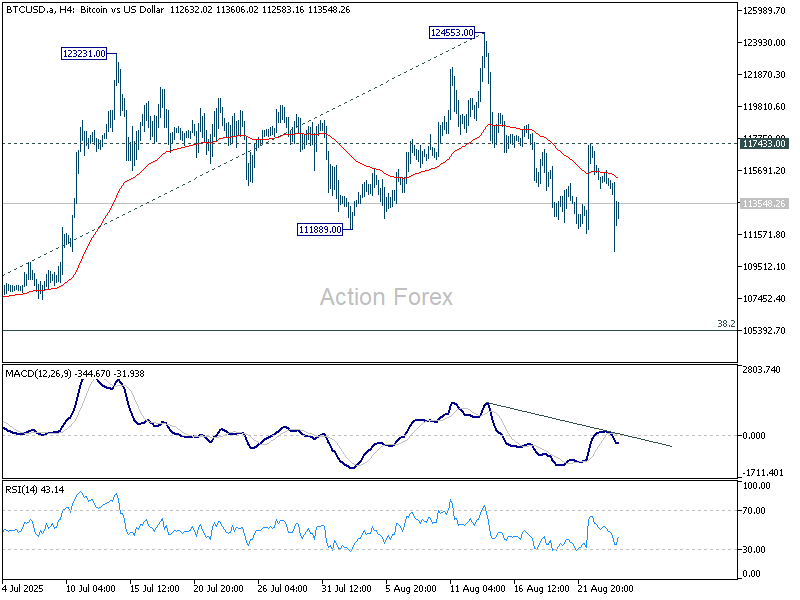

Exhausted Ethereum stalls below 5,000, risk of pullback builds

Ethereum briefly surged to a new record above 4,900 over the weekend but has struggled to sustain momentum just shy of the 5,000 psychological barrier. While ETH has outpaced Bitcoin in recent weeks on the view that BTC was overextended, momentum signals indicate Ethereum may now be equally exhausted.

Besides, historically, oversized weekend surges often retrace once liquidity returns early in the week. That dynamic, coupled with stretched momentum, leaves Ethereum exposed to a near-term correction.

Technically, while further rise cannot be ruled out yet, bearish divergence condition in 4H MACD suggests that Ethereum’s upside will likely be capped by 200% projection of 1,382.55 to 2,879.27 from 2,110.58 at 5,104.02. This makes the 5,000–5,100 area a formidable resistance zone.

On the downside, firm break of 55 4H EMA (now at 4,508.16) will confirm short term topping. In this case, Ethereum should then be correcting the rise from 2,110.58, which is seen as the third leg of the whole up trend from 1,382.55. Deeper correction should be seen to 4,060.93 support, or even further to 55 D EMA (now at 3,806.63) before resuming the up trend again with the final leg.

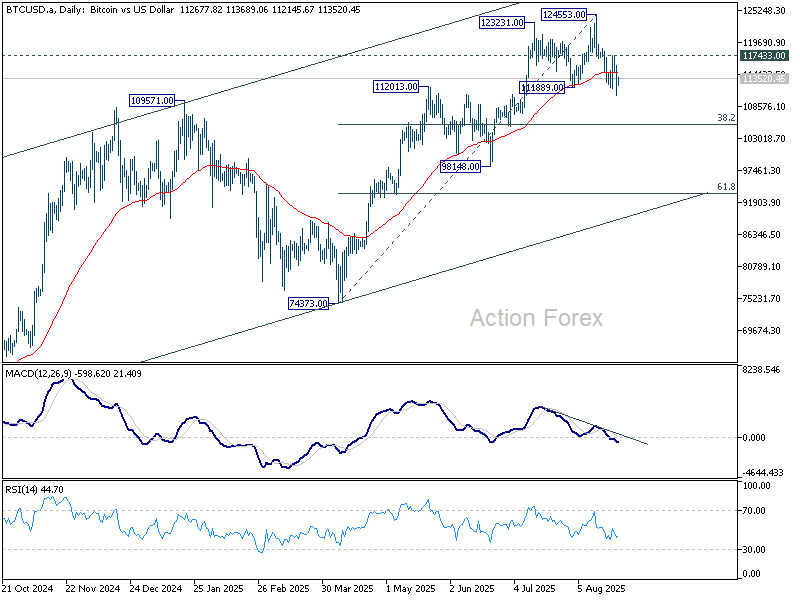

As for Bitcoin, the break of 111,889 support suggests that it’s already correcting the rise from 74,373. Near term risk will stay on the downside as long as 117,433 resistance holds. Deeper correction should be seen to 38.2% retracement of 74,373 to 124,553 at 105,384.

This leaves the near-term outlook more cautious across the crypto space, with both BTC and ETH vulnerable to profit-taking before attempting fresh highs later in the cycle.

US PCE, Tokyo CPI and RBA minutes set tone for data-light week

The final full week of August brings a relatively light calendar, but still enough to keep markets engaged as investors look beyond to September’s critical events. While inflation data from the U.S., Japan, and Australia will dominate, traders know the real turning points lie in early September with U.S. jobs and CPI.

The main focus in the U.S. will be July PCE inflation on Friday. Consensus points to headline PCE holding steady at 2.6% yoy, while core PCE edges up slightly to 2.9% yoy. Normally, such a reading would command market attention. But Fed Chair Jerome Powell’s dovish tilt at Jackson Hole has softened the impact of marginal surprises. Only a sharp deviation would challenge the market’s conviction that a September rate cut is the base case.

The real determinants will come in early September. Nonfarm payrolls on September 5 and CPI on September 11 are seen as the data points that will ultimately seal the Fed’s course for the September 16–17 meeting. Still, growth readings this week will matter. Personal spending and durable goods orders are expected to shed light on how consumers and businesses are coping with Trump’s tariff regime. Any signs of strain could reinforce the Fed’s case for policy easing.

Japan’s Tokyo CPI on Friday will be another focal point. Core inflation in the capital is expected to fall to 2.6% yoy, a meaningful step down from 2.9% yoy. BoJ policymakers will be looking for evidence that elevated food prices, especially rice, are finally cooling, while also watching whether services inflation remains firm. Alongside Tokyo CPI, Japan’s industrial production and retail sales will be important for assessing growth resilience.

Australia’s monthly CPI, due Wednesday, is forecast to accelerate sharply from 1.9% yoy to 2.3% yoy in July. The outsize move, however, is largely statistical—reflecting the fading of electricity rebate effects. Traders will also parse the RBA’s August meeting minutes, which could confirm the bank’s reluctance to act again in September. Money markets currently price less than a one-third chance of a 25bps cut next month, with November seen as more realistic.

European data are also due, with Germany’s Ifo and GfK surveys and Swiss GDP adding context. Still, the dominant themes are U.S. easing expectations, Japan’s inflation path, and whether Australia’s policymakers are comfortable staying patient for now.

Here are some highlights for the week:

- Monday: New Zealand retail sales; Germany Ifo business climate; US new home sales.

- Tuesday: RBA minutes; US durable goods orders, consumer confidence.

- Wednesday: Australia monthly CPI; Germany Gfk consumer sentiment.

- Thursday: New Zealand ANZ business confidence; Swiss GDP; US GDP revision, jobless claims, pending home sales.

- Friday: Japan Tokyo CPI; industrial production, retail sales; Germany retail sales, CPI flash, import prices, unemployment; Swiss KOF economic barometer; Canada GDP; US personal income and spending, PCE inflation, goods trade balance, Chicago PMI.

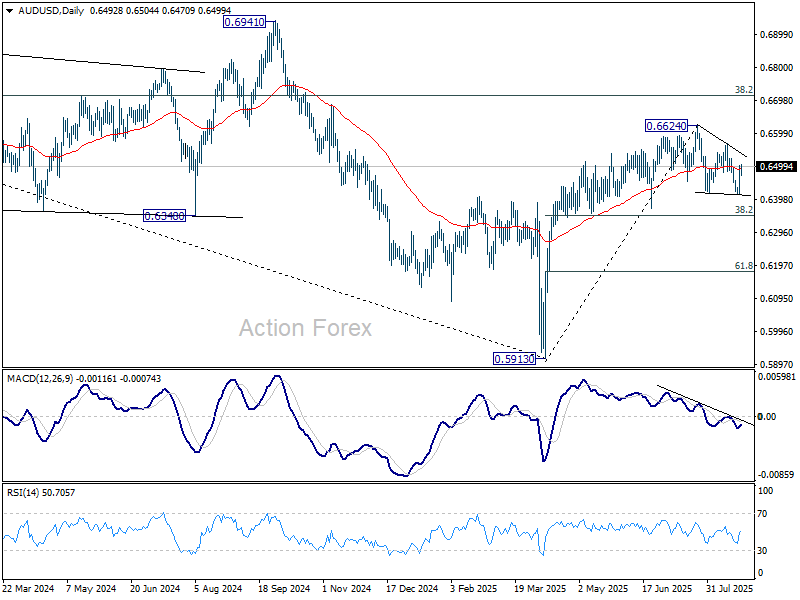

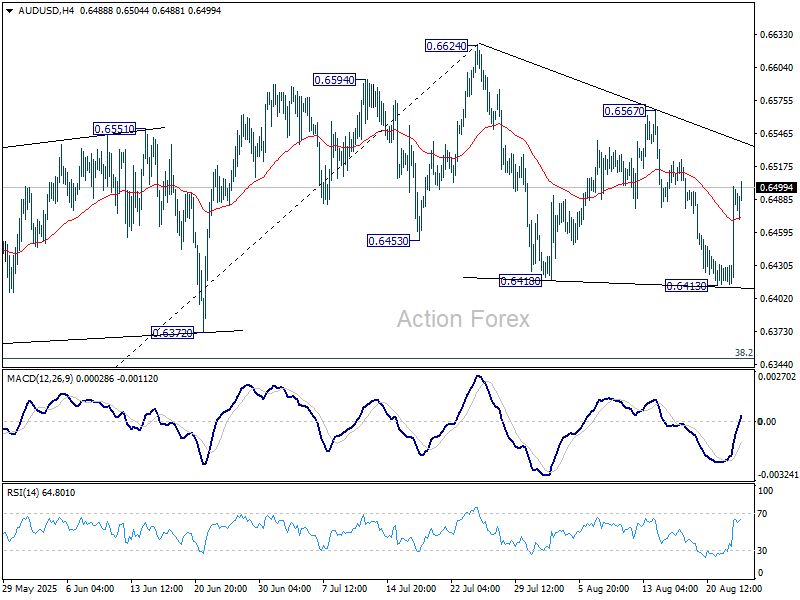

AUD/USD Daily Report

Daily Pivots: (S1) 0.6438; (P) 0.6469; (R1) 0.6524; More...

AUD/USD extends the rebound from 0.6413 but stays well below 0.6567 resistance. Intraday bias remains neutral first. Corrective pattern from 0.6624 could extend further sideway. On the upside, firm break of 0.6567 will argue that the correction has completed and bring retest of 0.6624 high. However, break of 0.6413 will extend the correction lower towards 38.2% retracement of 0.5913 to 0.6624 at 0.6352.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).