Fed’s Cook Prepares Lawsuit, India Tariffs Kick in, Markets Quiet – Action Forex

Currency markets were largely subdued in Asian session, with majors holding tight ranges despite some volatility in equities. U.S. stocks attempted a rebound overnight but momentum was weak, while Asian bourses traded softer. The absence of major economic data left political and policy headlines to set the tone.

At the center of focus remains the ongoing drama surrounding the Fed. Governor Lisa Cook is preparing to file a lawsuit to challenge U.S. President Donald Trump’s attempt to remove her from the Board. Cook’s lawyer described the action as illegal and lacking any factual or legal basis, pledging to fight it in court.

The Fed issued a statement reinforcing its institutional independence, stressing that governors serve 14-year terms and cannot be dismissed easily. The structure, it said, exists to ensure monetary policy is made in the “long-term interests of the American people.”

Trump, however, insisted he has a replacement in mind for Cook, saying he expects to secure a majority on the Fed Board “very shortly.” The comments have only intensified concerns about political influence over monetary policy, casting a cloud over the Fed as it heads into its September 16–17 meeting.

On the trade front, Trump’s doubling of tariffs on Indian imports took effect as scheduled. Duties on a wide range of goods — from garments and footwear to gems, furniture and chemicals — now reach as high as 50%, among the steepest levies imposed by Washington. The move reflects penalties tied to India’s continued purchase of Russian oil.

India’s Commerce Ministry has yet to issue a formal response. But a ministry official said exporters affected by the tariffs would receive financial assistance and be encouraged to diversify into other markets including China, Latin America, and the Middle East.

Against this backdrop, Dollar is currently the strongest performer. Aussie is the second best, underpinned by stronger-than-expected inflation data, while Loonie followed. On the downside, Euro lagged, trailed by Yen and Swiss Franc, while Sterling and Kiwi traded in the middle of the pack.

In Asia, Nikkei rose 0.30%. Hong Kong HSI is down -1.17%. China Shanghai SSE is down -1.13%. Singapore Strait Times is down -0.10%. Japan 10-year JGB yield rose 0.008 to 1.633. Overnight, DOW rose 0.30%. S&P 500 rose 0.41%. NASDAQ rose 0.44%. 10-year yield fell -0.017 to 4.258.

German Gfk consumer confidence falls to -23.6 on job fears

Germany’s GfK Consumer Sentiment index for September dropped to -23.6 from -21.7, falling short of expectations at -21.2. It was the third consecutive monthly decline, with NIM’s Rolf Bürkl describing sentiment as “definitely in the summer slump.”

The key driver was a sharp fall in income expectations as worries about job security intensified. Registered unemployment remained just below three million in July, but analysts expect that mark to be breached in August. Consumers’ expectations of rising unemployment have reached their highest level of the year.

Australia CPI jumps to 2.8%, highest in a year, rules out September RBA cut

Australia’s monthly CPI spiked to 2.8% yoy in July, well above expectations of 2.3% yoy and up sharply from 1.9% yoy in June. It was the highest annual inflation rate since July 2024, breaking several months of easing price pressures. Core measures also firmed, with CPI excluding volatile items rising from 2.5% yoy to 3.2% yoy and trimmed mean jumping back from 2.1% yoy to 2.7% yoy, a pace last seen three months ago.

The result adds to concern that inflation is proving sticky, though July’s data, as the first month of the quarter, is skewed toward goods and offers less insight into services inflation than subsequent months.

For the RBA, the print is a warning sign but not a trigger for panic. Policymakers will want to wait for the full quarterly inflation update before adjusting course. Today’s data nonetheless rules out a September cut.

Barring a significant deterioration in the labor market or other downside shocks, the more realistic timeline for the next rate move remains November.

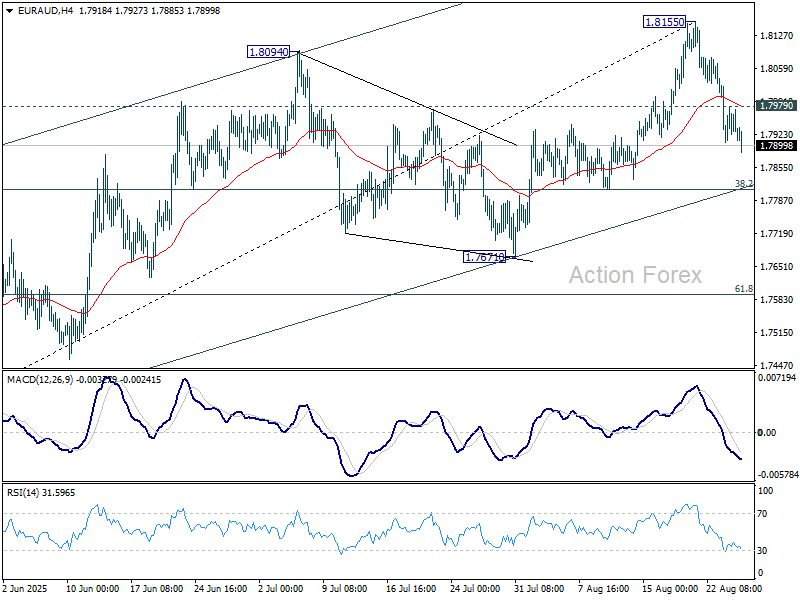

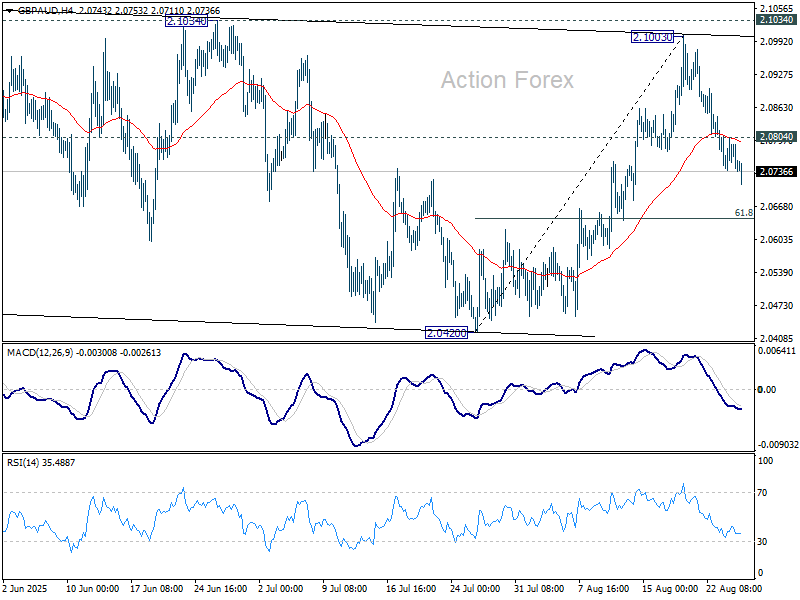

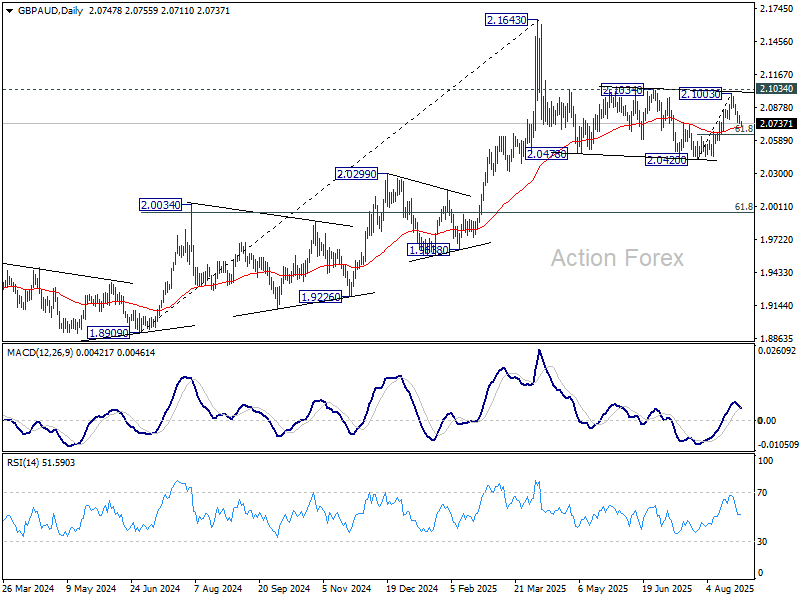

EUR/AUD and GBP/AUD extend declines, deeper losses in view

Aussie firmed notably after July’s CPI data came in much stronger than expected. The print reinforces the case for the RBA to maintain its gradual easing pace, removing any immediate scope for a faster round of rate cuts. Aussie’s gains were evident against the Euro and Sterling, with both crosses under renewed downside pressure.

EUR/AUD’s fall from 1.8155 short term top extends lower. Intraday bias remains on the downside for 38.2% retracement of 1.7245 to 1.8155 at 1.7807. That is close to channel support (now at 1.7816), and 55 D EMA (now at 1.7841).

Sustained break of this cluster support zone should confirm that whole rise from 1.7245 has completed. Corrective pattern from 1.8554 should then be in its third leg. In this case, bring deeper fall to 61.8% retracement at 1.7593.

GBP/AUD’s extended fall indicates short term topping at 2.1003 after rejection by 2.1034 resistance. The development suggests that corrective pattern from 2.1643 is still extending.

Deeper decline should be seen to 61.8% retracement of 2.0420 to 2.1003 at 2.0643 in the near term. Firm break there will target 2.0420 support and possible below.

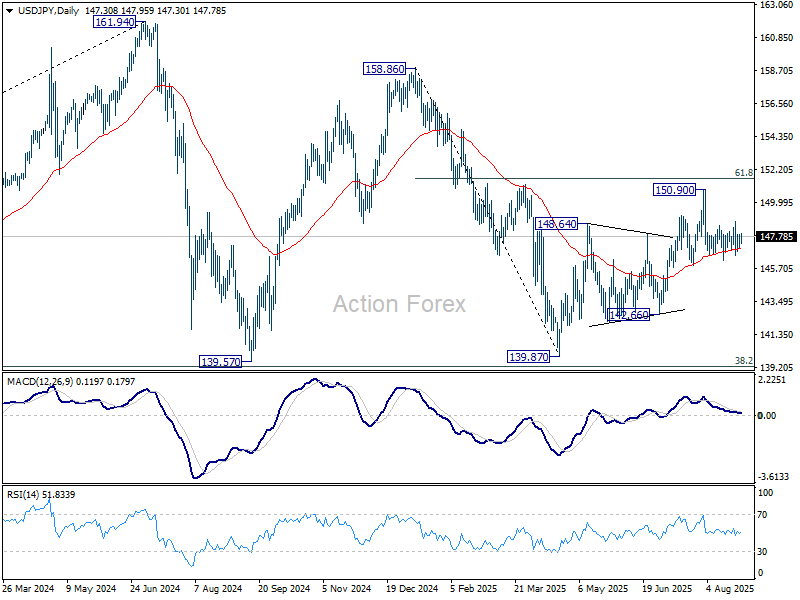

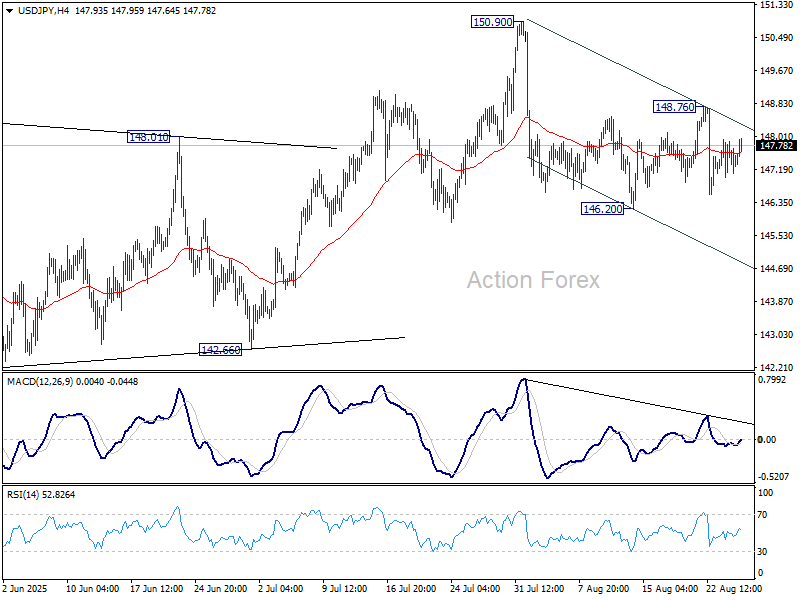

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.97; (P) 147.45; (R1) 147.92; More…

USD/JPY recovers mildly today but stays inside range of 146.20/148.76. Intraday bias remains neutral. On the downside, firm break of 146.20 will resume the fall from 150.90. Also, that would argue that rebound from 139.87 has completed as a corrective move to 150.90. Deeper fall should be seen to 142.667 support for confirmation. On the upside, above 148.76 will bring another rise to retest 150.90 instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.