Euro Leads But French Politics Cap Gains, Dollar Mixed – Action Forex

Euro is leading the foreign exchange market today, staging a solid recovery from last week’s weakness. Investors are clearly positioning back into the single currency, but the rally has yet to find a convincing fundamental driver, leaving momentum somewhat constrained.

Political uncertainty in France is also serving as a cap on Euro gains. The minority government of Prime Minister Francois Bayrou faces a high-stakes confidence vote on September 8 over its budget plans for 2026. With opposition parties aligned against the austerity package, defeat is seen as highly likely.

Still, markets are not turning bearish on the Euro purely on political grounds. Historically, domestic instability within one Eurozone member weighs heavily on the currency only when there are signs of contagion spreading across the bloc. At this stage, broader Eurozone fundamentals remain stable, and no such contagion is evident.

Dollar, meanwhile, is trading on the softer side but also lacks decisive momentum. Traders are cautious ahead of a heavy week of U.S. releases, with Friday’s nonfarm payrolls at the center of attention. The risk is skewed toward further Dollar weakness if data fall short, forcing the Fed to act more forcefully than the current market pricing suggests. For now, however, markets are waiting rather than moving aggressively.

In today’s performance table, Euro tops the leaderboard so far, followed by Sterling and Aussie. Yen is the weakest, trailed by Swiss Franc and Loonie, while the greenback and Kiwi are mixed in the middle.

In Europe, at the time of writing, FTSE is up 0.15%. DAX is up 0.41%. CAC is up 0.02%. UK 10-year yield is up 0.029 at 4.752. Germany 10-year yield is up 0.029 at 2.756. Earlier in Asia, Nikkei fell -1.24%. Hong Kong HSI rose 2.15%. China Shanghai SSE rose 0.46%. Singapore Strait Times rose 0.15%. Japan 10-year JGB yield rose 0.02 to 1.625.

ECB’s Lagarde warns on Fed independence, tariff uncertainty

ECB President Christine Lagarde issued a stark warning today, saying it would be “very worrying” if U.S. President Donald Trump succeeded in his efforts to exert control over the Fed.

In an interview with Radio Classique, Lagarde stressed “if US monetary policy were no longer independent and instead dependent on the dictates of this or that person, then I believe that the effect on the balance of the American economy could, as a result of the effects this would have around the world, be very worrying, because it is the largest economy in the world,”

Lagarde added that Friday’s U.S. appeals court ruling, which declared most of Trump’s tariffs illegal, created a “further layer of uncertainty” for the global economic outlook. The combination of policy unpredictability in Washington and structural risks elsewhere leaves investors wary at a time when global growth is already under strain from weak trade flows and tariff disputes.

Turning to domestic matters, Lagarde addressed mounting political risk in France ahead of the September 8 confidence vote. Opposition parties have pledged to bring down Prime Minister Francois Bayrou’s minority government over unpopular budget squeeze plans for 2026. The political drama has hit French bonds and equities, raising questions about the stability of the Eurozone’s second-largest economy.

Lagarde stressed, however, that France’s banking system is not at the root of the problem. She noted that banks are far better capitalised and structured than during the 2008 financial crisis, and remain responsibly managed. Still, she acknowledged that markets are sensitive to political shocks, and that uncertainty around government stability continues to weigh on risk sentiment.

Eurozone unemployment rate eases to 6.2% in July, matches expectations

Eurozone unemployment edged down to 6.2% in July from 6.3% in June, in line with expectations. The broader EU rate slipped from 6.0% to 5.9%, according to Eurostat.

Eurostat estimated 13.025 million unemployed across the EU in July, including 10.805 million in the Eurozone. Compared with June, jobless figures fell by -165k in the EU and -170k in the Eurozone.

China RatingDog PMI manufacturing rises to 50.5, relief rally rather than turning point

China’s manufacturing sector showed a modest improvement in August, with the RatingDog Manufacturing PMI rising from 49.5 to 50.5, beating expectations of 49.9 and returning to expansion. However, RatingDog described the uptick as a “breath of relief rather than a sustained rally,” reflecting cautious optimism. By contrast, the official NBS survey offered a more subdued view, with manufacturing inching up from 49.3 to 49.4 and non-manufacturing steady at 50.3.

The RatingDog report highlighted firmer new orders, which pushed inventories of raw materials and finished goods higher. Export demand remains weak but showed slower contraction. Yao cautioned that external demand may have been pulled forward while domestic demand stays soft, limiting the scope for sustained output gains without stronger local consumption.

Meanwhile, input costs continued to climb under the “Anti-involution” policy backdrop, and those upstream pressures are now filtering into output prices, ending an eight-month streak of falling charges. With profit recovery still slow, the durability of the latest rebound depends on whether exports can stabilize further and domestic demand begins to catch up.

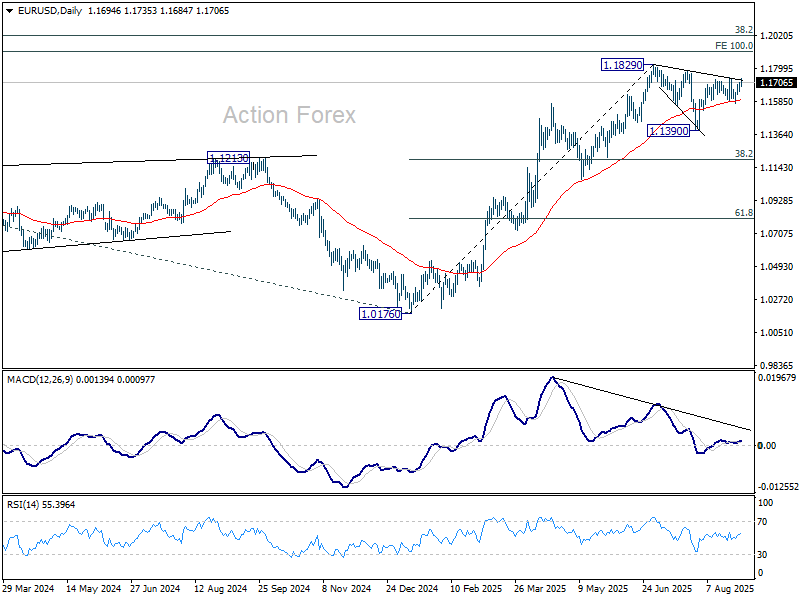

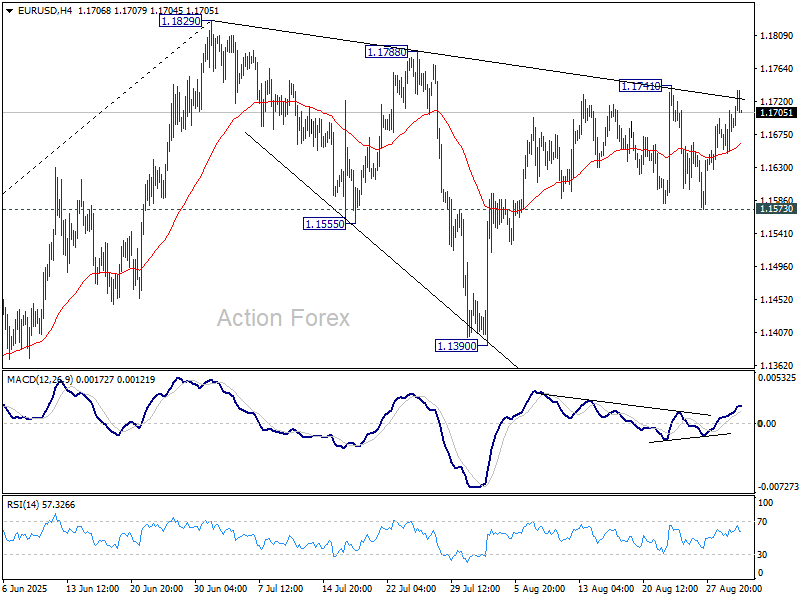

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1655; (P) 1.1682; (R1) 1.1713; More…

EUR/USD continues to struggle to break through 1.1741 resistance and intraday bias stays neutral Overall outlook is unchanged that corrective fall from 1.1829 should have completed with three waves down to 1.1390. On the upside, above 1.1741 will bring retest of 1.1829 high first. Firm break there will resume larger up trend. However, sustained break of 1.1573 will dampen this view, and indicate that corrective pattern from 1.1829 is extending with another falling leg towards 1.1390 again.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.