UoM Consumer Sentiment Index drops to 55.4 in September vs. 58 forecast

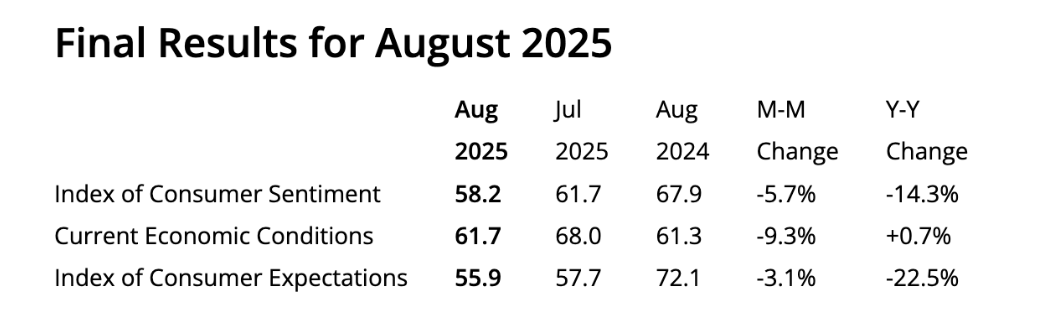

Consumer confidence in the US deteriorated further in September, with the University of Michigan’s Consumer Sentiment Index dropping to 55.4 in its preliminary estimate from 58.2 in August. This reading came in worse than the market expectation of 58.

Other details of the publication showed that the Consumer Current Conditions Index edged lower to 61.2 from 61.7, while the Consumer Expectations Index declined to 51.8 from 55.9.

Finally, the 1-year Consumer Inflation Expectation remained unchanged at 4.8% and the 5-year Inflation Expectation rose to 3.9% from 3.5%.

Market reaction to UoM Consumer Sentiment Index data

The US Dollar (USD) Index retreated from session highs after this report and was last seen gaining 0.2% on the day at 97.70.

US Dollar Price This week

The table below shows the percentage change of US Dollar (USD) against listed major currencies this week. US Dollar was the weakest against the Australian Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.08% | -0.37% | -0.41% | 0.07% | -1.34% | -0.99% | -0.19% | |

| EUR | 0.08% | -0.30% | -0.26% | 0.14% | -1.25% | -0.87% | -0.11% | |

| GBP | 0.37% | 0.30% | -0.04% | 0.45% | -0.95% | -0.57% | 0.20% | |

| JPY | 0.41% | 0.26% | 0.04% | 0.41% | -0.95% | -0.73% | 0.24% | |

| CAD | -0.07% | -0.14% | -0.45% | -0.41% | -1.31% | -1.01% | -0.26% | |

| AUD | 1.34% | 1.25% | 0.95% | 0.95% | 1.31% | 0.39% | 1.16% | |

| NZD | 0.99% | 0.87% | 0.57% | 0.73% | 1.01% | -0.39% | 0.77% | |

| CHF | 0.19% | 0.11% | -0.20% | -0.24% | 0.26% | -1.16% | -0.77% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

This section below was published as a preview of the University of Michigan’s Consumer Sentiment Index data at 11:00 GMT.

- September’s preliminary Michigan Consumer Sentiment Index is expected to have eased to 58.0 from 58.2 in August.

- US consumers are likely to maintain a pessimistic view of the economic outlook.

- Friday’s Consumer Sentiment is expected to strengthen the case for Fed easing.

The University of Michigan (UoM) is expected to release the preliminary figures of its monthly Consumer Confidence Index for September on Friday. This survey covers U.S. consumers’ views on their personal finances, business conditions, and purchasing plans, and is typically released alongside the University of Michigan Consumer Expectations Index and the University of Michigan Consumer Inflation Expectations.

Consumption is a key contributor to the US Gross Domestic Product (GDP). In that sense, the UoM Consumer Sentiment Index and Inflation Expectation figures have a solid reputation as forward-looking indicators for US economic trends, and their release tends to have a significant impact on US Dollar (USD) crosses.

Regarding preliminary September’s reading, the UoM Consumer Sentiment is expected to show further deterioration, to 58, from an already soft 58.2 level seen in August.

Market participants will also focus on the five-year Consumer Inflation Expectation reading, which rose to 3.5% in August from July’s 3.4%.

What to expect from September’s UoM Consumer Sentiment Index report?

September’s Consumer Sentiment data comes after a raft of grim employment indicators, with the last episode being a sharp downward revision of US job creation. The US Bureau of Labor Statistics (BLS) reported on Tuesday that the preliminary revision of the Current Employment Statistics (CES) national benchmark to total Nonfarm employment for the 12-month period through March 2025 was -911,000, or -0.6% fewer jobs than initially reported.

Later in the week, a sharp increase in US Initial Jobless Claims added to evidence of the labour market deterioration. This, coupled with a moderate uptick in consumer prices in August, has practically confirmed a September Fed interest rate cut and one or two more cuts before the year-end.

With this in mind, today’s consumer sentiment figures are likely to support those views. If August’s report reflected an increasing pessimism about the current economic conditions and the overall economic outlook, things seem to have only worsened in September.

Consumer Sentiment is expected to have dropped to 58.0 in September from 58.2 in August and 61.7 in July. These figures are nearly 15% below the levels of August last year, which highlights the negative impact of US President Donald Trump’s trade policies on US consumption.

Source: University of Michigan

All in all, not the best news for the US Dollar, which is suffering amid rising concerns that the Federal Reserve might have fallen behind the curve with rate cuts. A mix of weak employment, relatively moderate inflation, and deteriorating consumer sentiment provides an ideal scenario for the US central bank to resume its monetary easing cycle.

When will the UoM Consumer Sentiment Index be released, and how could it affect EUR/USD?

The University of Michigan will release its Consumer Sentiment Index, together with the Consumer Inflation Expectations survey, on Friday at 14:00 GMT. The market consensus points to further deterioration in US consumer sentiment, which would add downside pressure to the US Dollar. However, geopolitical tensions in the Eurozone might offset the impact on the EUR/USD pair as frictions between Russia and Poland have undermined confidence in the common currency.

The EUR/USD rally has been halted below late July highs of 1.1790, but downside attempts have been contained above the 1.1700 area so far, which maintains the immediate positive trend in place.

To the downside, the early September lows, near 1.1610 and 1.1630, are key levels for bears, while, on the upside, resistance at 1.1780 (September 9 high) and 1.1790 (July 24 high) need to be broken to extend the broader bullish trend towards the year-to-date highs, at 1.1830.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.