Calm Before the Fed: Dollar Soft, Markets Brace for Guidance – Action Forex

Markets traded with a subdued tone today as investors awaited the Fed’s highly anticipated policy decision. The Fed is expected to cut rates by 25bps, but the real market mover will be the details: how divided the vote is, what the updated projections show, and the signals Chair Jerome Powell delivers in his press conference. These elements will define expectations for how far and how fast easing progresses from here.

The stakes are high. U.S. equities and Gold are already at record highs, with scope to extend gains if Powell confirms a dovish tilt. Bond traders are focused on whether the 10-year yield can slip below the 4% mark, a level that could trigger broader repricing across global fixed income. Meanwhile, Dollar — this week’s laggard — risks an accelerated selloff if the Fed opens the door to back-to-back cuts.

The BoC decision also lands today, with a 25bps cut to 2.50% widely expected. Markets will be looking for any signal that more easing is in the pipeline, particularly now that uncertainty around tariffs has eased. Recent soft growth and employment data have built the case for further accommodation, and the Loonie’s resilience could hinge on whether Governor Tiff Macklem leaves that door open.

In Europe, the spotlight is on UK inflation figures. With the BoE expected to hold policy tomorrow, the real question is whether the data tilt the odds for another cut in November. Headline and services inflation will be critical, with a stronger print weakening the case for further easing.

Overall, Dollar remains pinned to the bottom of the currency performance ladder, followed by Kiwi and Aussie. Swiss Franc has emerged as the strongest, followed by Euro and Yen, while Sterling and Loonie are stuck in the middle of the pack.

On the trade front, U.S. Treasury Secretary Scott Bessent struck an optimistic tone, saying he believes a deal with China is “near.” With reciprocal tariffs due to take effect in November, Bessent said further talks are expected before then, noting that each round of discussions has become “more and more productive.” He added that Chinese negotiators now “sense that a trade deal is possible,” offering a rare dose of optimism in a tense environment.

In Asia, at the time of writing, Nikkei is down -0.34%. Hong Kong HSI is up 1.59%. China Shanghai SSE is up 0.21%. Singapore Strait Times is down -0.39%. Japan 10-year JGB yield is down -0.003 at 1.601. Overnight, DOW fell -0.27%. S&P 500 fell -0.13%. NASDAQ fell -0.07%. 10-year yield fell -0.008 to 4.026.

Japan August exports near flat, -13.8% US plunge balanced by other markets

Japan’s trade deficit narrowed in August to JPY -242.5B, smaller than expectations for JPY -513.6B, as exports outperformed forecasts. Overall exports dipped just 0.1% yoy to JPY 8425B, beating projections for a 1.9% yoy decline. Imports, however, fell -5.2% yoy to JPY 8668B, a steeper drop than the -4.2% yoy contraction expected.

The details highlighted stark divergences. Exports to the U.S. tumbled -13.8% yoy, the sharpest fall since February 2021, led by a -28.3% yoy plunge in autos and a -38.9% yoy drop in chipmaking equipment. By contrast, shipments to Asia rose 1.7% yoy, while exports to Western Europe jumped 7.7% yoy. Exports to mainland China slipped 0.5% yoy, though shipments to Hong Kong surged 14.4% yoy.

Australia leading index turns below trend, but RBA to wait until November to cut again

Australia’s Westpac Leading Index growth rate slipped into negative territory in August, falling from 0.11% to -0.16%. It marks the first below-trend reading since September 2024 and a sharp moderation from February’s peak of 0.86%.

Westpac noted the weakness is “not overly concerning” but highlights a “clear softening” from earlier in the year, consistent with the economy slowing after a relatively strong June quarter. It expects growth of 1.9% in 2025, better than the 1.3% expansion in 2024 but still below trend, with a return to trend pace only in 2026.

The RBA meets on September 29–30, where policymakers are almost certain to hold the cash rate steady at 3.6%. Westpac argues that incoming data should eventually validate benign inflation and soft demand, paving the way for a 25bp cut in November, followed by two further cuts in 2026. For now, the RBA will proceed cautiously, watching for confirmation of underlying trends before easing again.

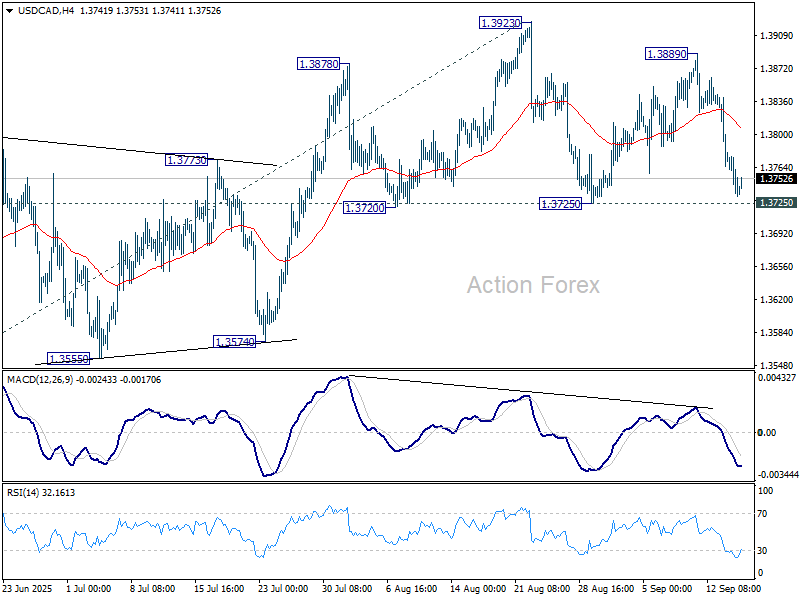

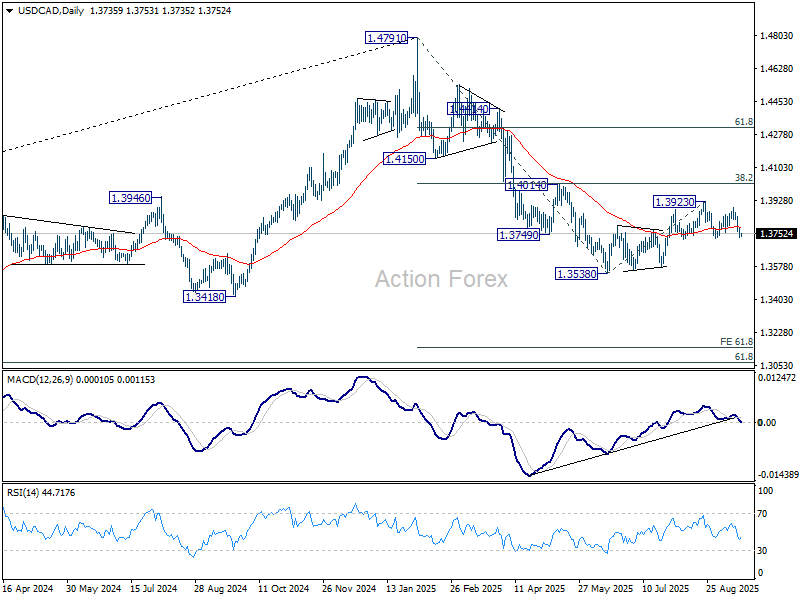

BoC and Fed double-header as USD/CAD flirts with head-and-shoulders reversal

Global markets are bracing for a double dose of central bank action today, with both the BoC and the Fed expected to deliver interest rate cuts. While the decisions themselves are largely anticipated, the bigger question is what kind of guidance policymakers provide for the months ahead. With USD/CAD now sitting just above the neckline of a head and shoulder top pattern, today’s policy decisions could be the make or break for the currency pair.

The BoC is almost certain to trim its policy rate by 25bps to 2.50%. The case for cutting was reinforced by August CPI, which rose 1.9% yoy — weaker than forecast. While core inflation remains sticky at elevated levels, the fact that it has stayed steady for three months gives policymakers confidence that underlying pressures are contained.

Beyond inflation, the growth backdrop has deteriorated noticeably. Canada’s economy contracted by -0.4% qoq in Q2, undershooting the BoC’s own forecasts. August data revealed a second consecutive month of job losses and a higher unemployment rate. These signals of slackening demand strengthen the case for pre-emptive easing. Markets now want to know whether Governor Tiff Macklem will acknowledge the need for more cuts before year-end.

According to a Reuters poll, over 70% of economists see at least one more 25bps reduction in 2025, with some forecasting two additional cuts to take the policy rate down to 2.00%. Whether the BoC leans toward validating that view, or opts to remain data-dependent, could set the tone for Canadian Dollar.

For the Fed, a 25bps cut to 4.00–4.25% is virtually locked in, with futures assigning only a 4% chance to a larger 50bps move. Consensus has hardened around the idea of “back-to-back-to-back” cuts in September, October, and December, which would lower the target range to 3.50–3.75% by year-end. The policy statement, dot plot, and Chair Jerome Powell’s press conference will be dissected for confirmation of this trajectory.

Beyond the near term, attention will turn to the pace of easing in 2026 and beyond. June projections showed rates drifting to 3.6% in 2026 and 3.4% in 2027, with the longer-run neutral rate anchored near 3.0%. The critical question is whether the Fed signals that the 3.00–3.25% zone could be reached as early as 2026, suggesting a faster normalization path than previously expected — with significant implications for bonds, equities, and Dollar.

Technically, USD/CAD is now on a knife edge. Decisive break below 1.3725 would complete a head-and-shoulders top (ls: 1.3878; h: 1.3923; rs: 1.3889), confirming that the corrective rebound from the 1.3538 low has ended. That would put the larger downtrend back in play, with an retest of 1.3538 first. Firm break there would open the way toward 61.8% projection of 1.4791 to 1.3538 from 1.3923 at 1.3149.

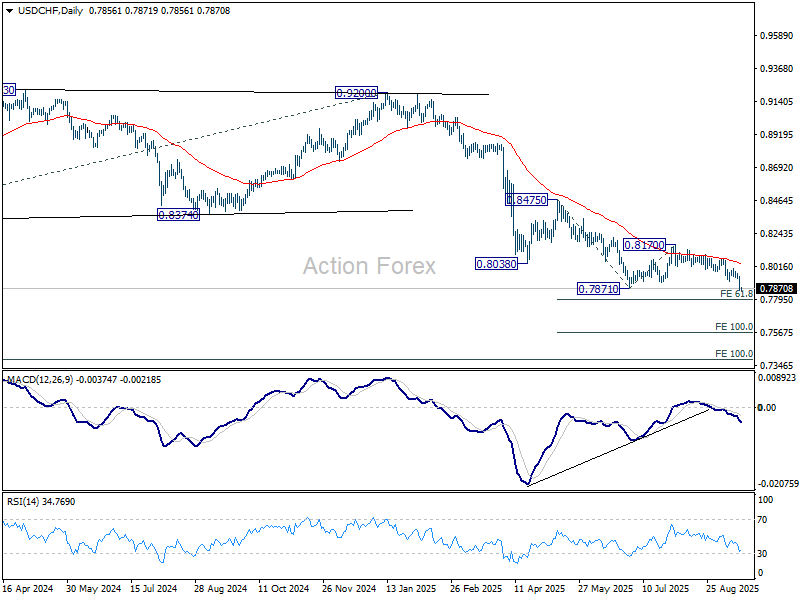

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7827; (P) 0.7888; (R1) 0.7920; More….

USD/CHF’s break of 0.7871 low confirms down trend resumption. Intraday bias stays on the downside for 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797. Firm break there will pave the way to 100% projection at 0.7566. On the upside, 0.7914 support turned resistance will turn intraday bias neutral for consolidations But recovery should be limited below 0.8006 resistance to bring another fall.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds.