Yen Rebounds as BoJ Tilts Hawkish, Nikkei Retreats From Record – Action Forex

Yen staged a broad rebound today after the BoJ held rates steady at 0.50% but delivered a hawkish signal with two members dissenting in favor of a hike. The shift in the board underlined growing momentum toward policy normalization. At the same time, the Nikkei pulled back sharply from record highs reached earlier this week, reflecting investor caution around the prospect of tighter conditions.

The changing balance within the BoJ highlights a gradual move closer to resuming rate hikes, even as inflation pressures ease. Yet, political developments could complicate the path ahead. The departure of Prime Minister Shigeru Ishiba and uncertainty over his successor may encourage policymakers to tread carefully, waiting for a clearer political backdrop before committing to a move.

In currency markets, Kiwi remains the weakest performer of the week, weighed down by a shock contraction in Q2 GDP that fueled speculation of a deeper easing cycle by the RBNZ. The Aussie also lags following soft labor market data. Sterling is under pressure after the BoE left policy unchanged, with two members voting for a cut. By contrast, Swiss Franc leads the pack, followed by Loonie and Euro. Dollar and Yen are holding mid-table, though today’s rebound leaves the Yen better positioned than earlier in the week.

Looking ahead, focus will shift to upcoming data releases including Germany’s PPI, UK retail sales, and Canadian retail sales. While these could generate short-term volatility, they are unlikely to provide lasting direction heading into the weekend, with broader themes of central bank divergence still dominating market sentiment.

In Asia, at the time of writing, Nikkei is down -0.27%. Hong Kong HSI is down -0.02%. China Shanghai SSE is up 0.14%. Singapore Strait Times is down -0.17%. Japan 10-year JGB yield is up 0.04 at 1.641. Overnight, DOW rose 0.27%. S&P 500 rose 0.48%. NASDAQ rose 0.94%. 10-year yield rose 0.028 to 4.104.

BoJ holds with two members calling for hike, starts selling ETFs and J-REITs

The BoJ kept rates steady at 0.50% in September, but the 7–2 vote revealed a growing hawkish bias. Naoki Tamura and Hajime Takata broke ranks to support a rate increase, citing upside risks to inflation and progress toward achieving the 2% price stability target. Takata said that Japan has more or less achieved its inflation goal, while Tamura argued that the key rate should move closer to neutral given skewed risks to the upside.

Alongside the decision, the BoJ unveiled plans to shrink its massive balance sheet by selling assets. The Bank will sell ETFs at a pace of JPY 330B annually and J-REITs at JPY 5B, with the principle of minimizing market disruption. With its balance sheet at 125% of GDP—far larger than other major central banks—the BoJ’s move marks a notable shift toward normalization, even as rates remain unchanged for now.

Japan core CPI Slows to 2.7%, lowest since late 2024

Japan’s consumer inflation eased notably in August, with both headline CPI and core CPI (excluding fresh food) falling to 2.7% yoy from 3.1% in July, the lowest since November 2024. Despite the slowdown, inflation has remained above the BoJ’s 2% target for over three years.

Core-core CPI, which strips out both fresh food and energy and is seen as a key gauge of underlying price dynamics, ticked down to 3.3% yoy from 3.4%. The moderation suggests a gradual cooling in inflationary pressures, though price growth remains elevated relative to historical norms.

Food prices continued to drive the cost-of-living squeeze, with processed food up 8.0% yoy, though slower than July’s 8.3%. Rice inflation also eased to 69.7% yoy from an eye-watering 90.7%. Energy prices provided some relief, falling -3.3% yoy after a -0.3% drop in July.

NZ exports jump 23% in August, imports flat, deficit at NZD -1.2B

New Zealand recorded a goods trade deficit of NZD 1.2B in August as imports outpaced a sharp rise in exports. Goods exports climbed NZD 1.1B, or 23% yoy, to NZD 5.9B, supported by strong shipments to major partners. Imports slipped slightly, falling NZD 30m (-0.4% yoy) to NZD 7.1B, but remained elevated enough to keep the monthly balance in deficit.

Export growth was broad-based, with China (+35% yoy, the EU (+52%), Australia (+17%), and the U.S. (+14%) all showing strong gains. Japan was the notable exception, where exports fell -11% yoy, driven by a NZD 28m decline in milk powder, butter, and cheese.

On the import side, flows from China rose 6.2% yoy, while purchases from the EU fell -6.0% and from the U.S. declined -1.3%. The largest pullback came from South Korea, where imports dropped -32% yoy.

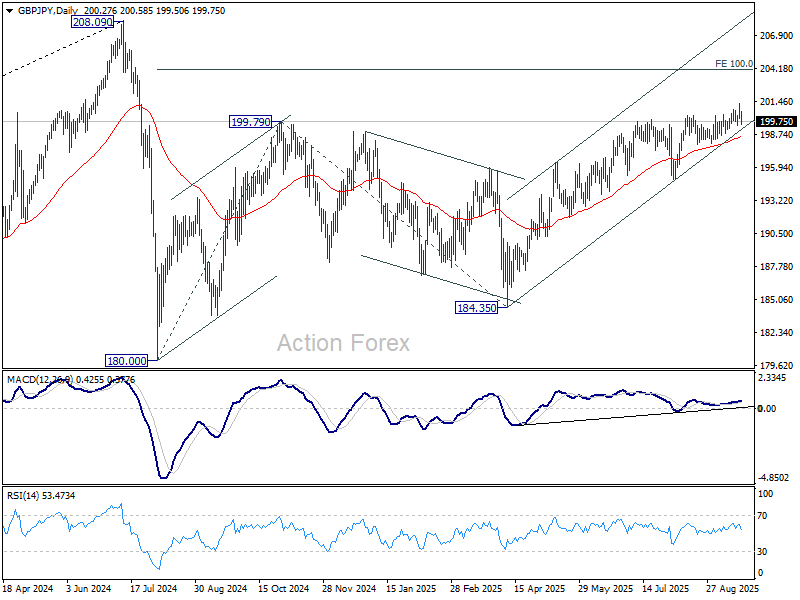

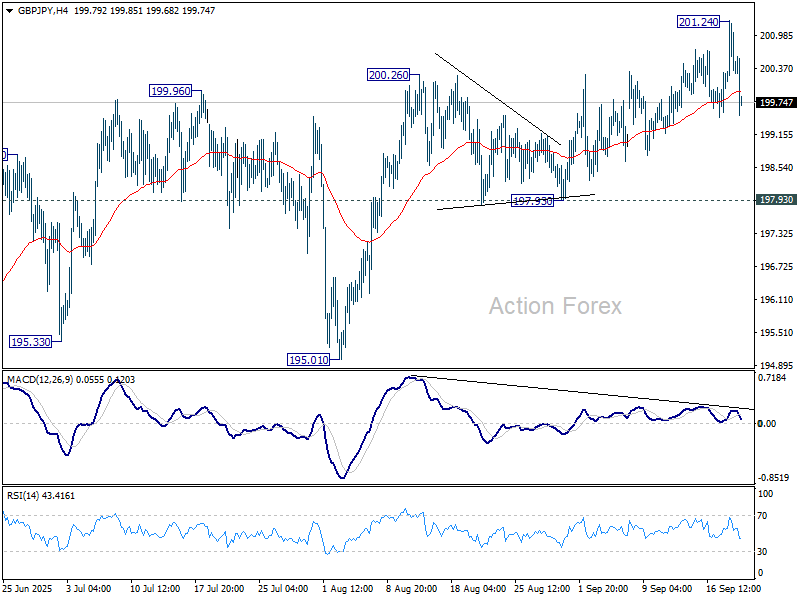

GBP/JPY Daily Outlook

Daily Pivots: (S1) 200.00; (P) 200.64; (R1) 201.22; More…

GBP/JPY spikes higher to 201.24 but quickly retreated. Intraday bias remains neutral first. Further rise is expected as long as 197.93 support holds. Firm break of 201.24 will target 100% projection of 180.00 to 199.79 from 184.35 at 204.14. However, considering bearish divergence condition in both D and 4H MACD, firm break of 197.93 will indicate bearish reversal and bring deeper fall back to 195.01 support first.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.