Everybody Happy? Fed’s Decision Calms Markets—for Now – Action Forex

The past week has been anything but quiet for global markets. A long-anticipated Fed rate cut finally arrived, but the message was less dovish than traders had braced for. Instead, policymakers struck a balance — restarting the easing cycle while simultaneously projecting confidence in the economy’s resilience. That left investors reassured. Equities cheered the outcome, with all three major U.S. indices printing record closes. Bond yields swung sharply before settling higher, while Dollar staged an equally forceful rebound from the week’s lows.

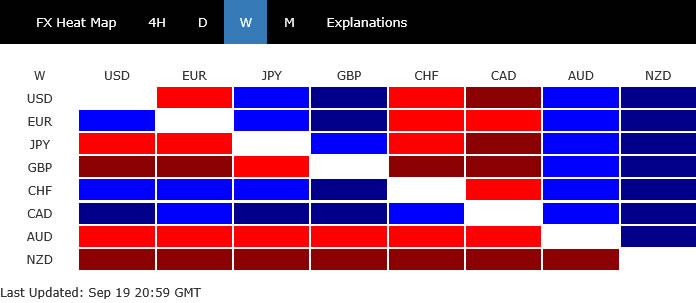

The foreign-exchange market told its own story. By week’s end, Loonie surprisingly sat at the top of the performance ladder, joined by Swiss Franc and Euro. The strength of the Loonie was especially striking, coming despite a widely anticipated BoC rate cut. Solid August retail sales estimates pointed to a Q3 rebound, keeping expectations of further BoC easing measured.

At the other end of the scale, Kiwi was crushed after a shocking Q2 GDP contraction. Traders are now openly speculating about a 50bps RBNZ cut in October, with the policy rate potentially falling below the Bank’s own year-end estimate. Aussie fared little better, weighed down by poor August jobs data and a growing consensus that November will bring another RBA rate cut.

Sterling also struggled, with the BoE holding steady but showing a slightly more dovish split. Euro and Franc were firmer in crosses, yet their momentum against Dollar faded quickly after the Fed’s rebound. Meanwhile, Yen was caught in a tug-of-war: boosted by hawkish dissenters at the BoJ, but capped by rebounding U.S. yields and relentless U.S. equity strength.

Fed’s Balanced Cut Signals Confidence, Not Capitulation

The highly anticipated FOMC decision did not disappoint investors. The Fed lowered federal funds rate by 25bps to 4.00–4.25%, restarting its easing cycle after holding policy steady for much of the year. The overall tone of the announcement leaned less dovish than markets had hoped. Still, equities, bonds, and Dollar responded constructively, showing that the outcome struck a balance that reassured all sides.

What stood out was Chair Jerome Powell’s characterization of the move as a “risk management” cut rather than an emergency measure. This distinction signaled confidence in the underlying strength of the U.S. economy and underlined that the Fed is not panicking in the face of softer labor data and tariff uncertainty. For investors, that was an important reassurance.

The decision was accompanied by a clear signal that policymakers still see two more cuts this year, in October and December. That aligns closely with market pricing, reinforcing the idea that monetary policy is easing in a measured, predictable fashion rather than an abrupt pivot.

Projections offered additional comfort. The Fed nudged its GDP forecasts higher across the projection horizon, with growth now seen at 1.6% in 2025, 1.8% in 2026, and 1.9% in 2027. Unemployment forecasts were revised lower, pointing to a more resilient labor market than previously thought. Together, these revisions suggest policymakers believe the economy can withstand the tariff shock and still maintain positive momentum.

Inflation forecasts were also adjusted only slightly, with 2026 core PCE raised to 2.6% from 2.4% on the view that tariff effects could linger. Crucially, the longer-run trajectory remains anchored around the 2% target, and the shallow upward tweak was viewed as temporary rather than destabilizing.

On the rate path, the overall picture was modestly softer. The Fed now projects one additional cut in 2026 and another in 2027, lowering the terminal policy rate to 3.1%. That remains just above the longer-run neutral estimate of 3.0%, underscoring that policymakers still see policy ending in slightly restrictive territory rather than slipping into excessive accommodation.

Equally significant was the voting composition. Newly confirmed Governor Stephen Miran dissented in favor of a larger 50bps cut, but even well-known doves Christopher Waller and Michelle Bowman supported the 25bps move. This alignment suggests that the decision was broadly supported across the Committee, and that the Fed is maintaining institutional discipline rather than bending to political pressure.

The optics matter. After months of speculation that the Trump administration could force the Fed into more aggressive easing, the outcome showed no evidence of interference. Instead, the vote and dot plot highlighted an independent central bank weighing risks carefully and arriving at a balanced decision.

For markets, this combination of gradual easing, stronger growth projections, and a reaffirmation of Fed independence was almost the ideal mix. Risk assets surged, bond yields rebounded, and Dollar found a floor. The sense was that monetary policy is flexible enough to manage risks while still anchored by confidence in the broader economy.

All told, the decision was received as a pragmatic and measured step. It reminded markets that the Fed is easing, but not capitulating, and that growth and employment prospects remain intact. In that sense, the announcement made “everybody happy”—a rare outcome in today’s polarized policy environment.

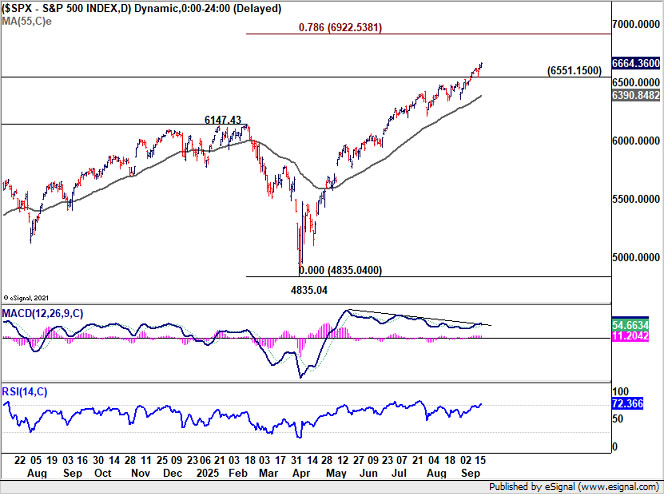

S&P 500 Breaks Higher Eyes Extension Toward 6920 in Q4

S&P 500 closed at a fresh record high after the Fed’s decision, extending an already powerful run in U.S. equities. The index gained ground in tandem with the NASDAQ and DOW.

Technically, Daily MACD has broken above its falling trend line, a sign buying momentum is regathering after a period of consolidation. This comes on top of sustained trading above the long-term channel ceiling on the weekly chart, which continues to reinforce the broader bullish structure.

With that backdrop, the S&P 500’s current rise looks on course for 78.6% projection of 3491.58 to 6147.43 from 4835.04 at 6922.53 in Q4.

Nevertheless, firm break of 6551.15 support would indicate that near-term momentum has stalled. Such a pullback would not imply a topping pattern, but rather a transition to a slower, more natural pace of gains rather than the rapid upside bursts seen this week.

10-Year Yield Rebounds After Finding Support at 4%

U.S. Treasury yields responded decisively to the Fed’s policy shift, with the 10-year climbing to 4.139, its highest close in two weeks. The move was particularly notable given that the benchmark had briefly slipped below 4% psychological level earlier in the week. That level is should now be being recognized as a near-term floor, with buyers reluctant to push yields much lower while the Fed’s easing path remains measured rather than aggressive.

Technically, D MACD has crossed above its signal line, confirming that downside momentum has eased and that a short-term bottom was formed at 3.992. This pivot was also supported by the falling channel floor. With that base in place, further recovery toward 55 D EMA (now at 4.228) is in favor. Nevertheless, strong resistance should be seen above there to limit upside.

Meanwhile, as the US economy is expected to retain resilience even under a measured easing cycle, it’s unlikely for yield to collapse. That backdrop leaves the 10-year in a consolidation phase rather than a one-way trend. Another downside attempt cannot be ruled out, but any move lower is likely to be contained by 3.992 low. Sideways trading in a 4.0–4.25% band could define the near-term range until incoming data challenge the Fed’s forecasts.

Dollar Index Rebounds Post-Fed, Long-Term Channel Support Intact

Dollar Index staged a strong rebound alongside U.S. yields, shaking off the heavy tone that had dominated in early part of the week.

The broader context is important and shouldn’t be ignored. DXY remains perched just above the long-term channel floor that has defined its uptrend since 2008. That structural support matters: rebounds from these levels are common, even if they ultimately resolve into consolidations rather than new bull runs.

Zooming into the near-term picture, the Index breached 96.37 briefly to 96.21, only to recover sharply. Focus now shifts to 55 D EMA (currently at 98.09). Decisive break there would confirm short-term bottoming at 96.21 and open the path to higher levels.

The first upside marker in such a scenario would be 100.25, a resistance level that represents a natural test of the rebound’s durability. Even under the most conservative interpretation — treating the recovery as just the third leg of a sideway consolidation pattern from 96.37 — that level should be achievable.

More bullish interpretations are also possible. The rebound could evolve into a correction of the whole fall from 110.17, or even the beginning of a reversal of the entire decline from the 2022 high at 114.77. Such outcomes, however, hinge heavily on whether incoming data validate the Fed’s current projections of shallow easing and resilient growth. Until then, Dollar Index remains in a state of cautious, near term recovery first.

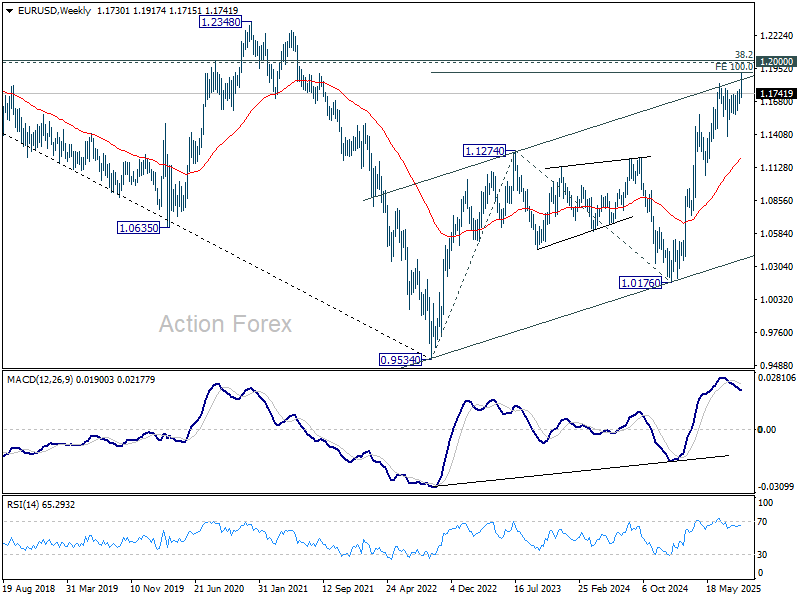

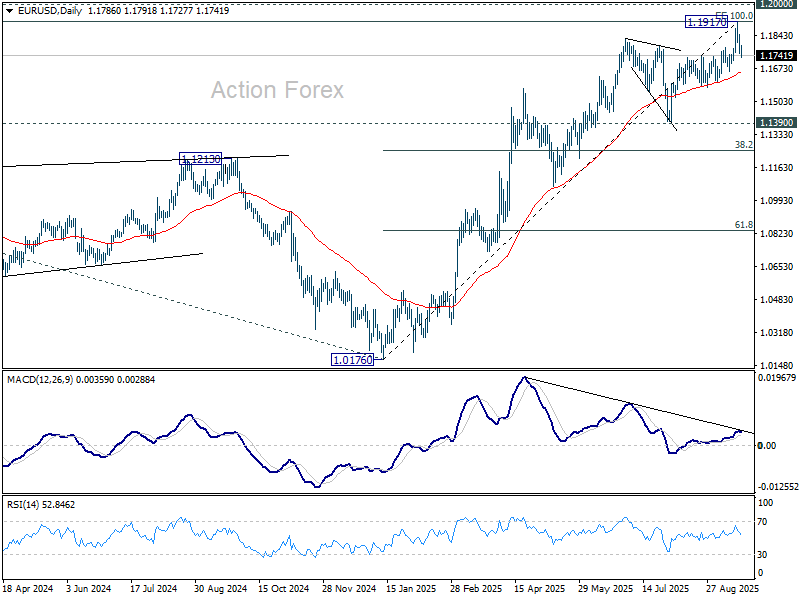

EUR/USD Weekly Outlook

A short term top should be formed in EUR/USD at 1.1917 with subsequent deep pullback. Initial bias is staying on the downside this week for 55 D EMA (now at 1.1653). Considering bearish divergence condition in D EMA, sustained break of 55 D EMA will argue that 1.1917 is already a medium term top. Deeper fall should then be seen to 1.1390 support next. On the upside, though, above 1.1847 minor resistance will retain near term bullishness and bring retest of 1.1917 high instead.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1214).

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.