Yen Recovers as Nikkei Pulls Back, Dollar Pressured by US Shutdown Risk – Action Forex

Yen jumped broadly in Asian trading today, marking a strong performance on the penultimate session of Q3. The move coincided with a drop in Nikkei, where ex-dividend effects weighed on equities, prompting flows into Yen. The quarter-end context likely amplified positioning shifts.

Beyond equities, anticipation of the BoJ’s upcoming Summary of Opinions also bolstered Yen. With two policymakers dissenting in favor of a hike at the last meeting, markets expect the document to reveal a more hawkish tone. The key question is how much support is building within the Board for an imminent move toward higher rates. Even a modest signal of broadening support for rate increases could sharpen expectations for a hike later this year.

On the other side of the ledger, Dollar came under pressure as US political risk resurfaced. Washington faces the prospect of a partial government shutdown if Congress fails to pass a funding bill before Tuesday. While shutdowns are nothing new in the US, the uncertainty has weighed slightly on the greenback in early trading.

Investors are more focused on how a shutdown could disrupt economic data releases, particularly the highly anticipated September non-farm payrolls due Friday. Any delay in the report would leave markets flying blind on the most important labor market gauge, complicating Fed expectations heading into October.

For now, Yen leads the day’s performance, followed by Aussie and Kiwi. Dollar sits at the bottom alongside the Loonie and Euro. Sterling and Swiss Franc are trading mid-pack.

In Asia, at the time of writing, Nikkei is down -0.89%. Hong Kong HSI is up 1.57%. China Shanghai SSE is up 0.41%. Singapore Strait Times is up 0.20%. Japan 10-year JGB yield is down -0.018 at 1.642.

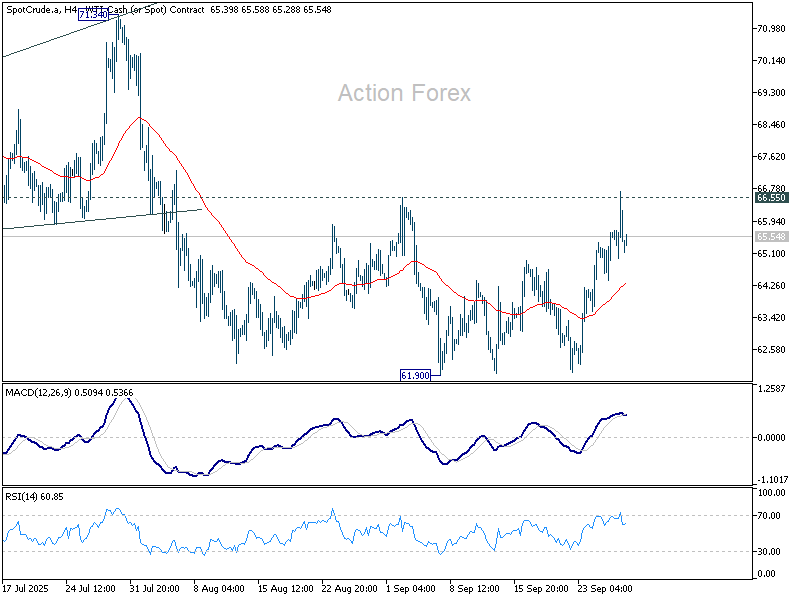

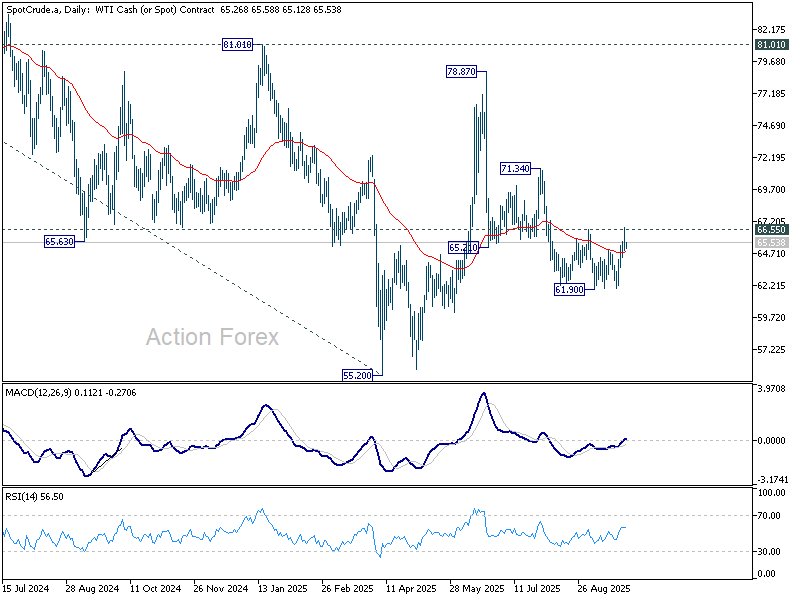

WTI oil bulls need 66.55 break as OPEC+ hike decides next move

Oil prices slipped slightly in Asian session after reports that OPEC+ is set to approve another production hike in November. The group is said to consider lifting quotas by at least 137k barrels per day when ministers meet next Sunday, adding to the series of increases since April.

The cartel has already boosted output quotas by more than 2.5 million barrels per day, equivalent to around 2.4% of global demand. The shift marks a decisive reversal from earlier supply restraint, with members now focused on regaining market share as prices hover at supportive levels.

Eight key producers will meet online on October 5 to finalize the November decision. Markets will be watching not just the headline figure but also whether the hike overshoots expectations, which could put fresh pressure on prices. On the other hand, smaller-than-anticipated increase could give oil prices a lift through a key near term resistance level.

Technically, WTI’s drop from 78.87 appears to have completed as a three wave correction at 61.90. The immediate focus is resistance at 66.55. Firm break above this barrier would reinforce this bullish and target 71.34.

However, rejection by the resistance would keep the short-term outlook bearish, leaving the door open for another fall through 61.90 as a later stage.

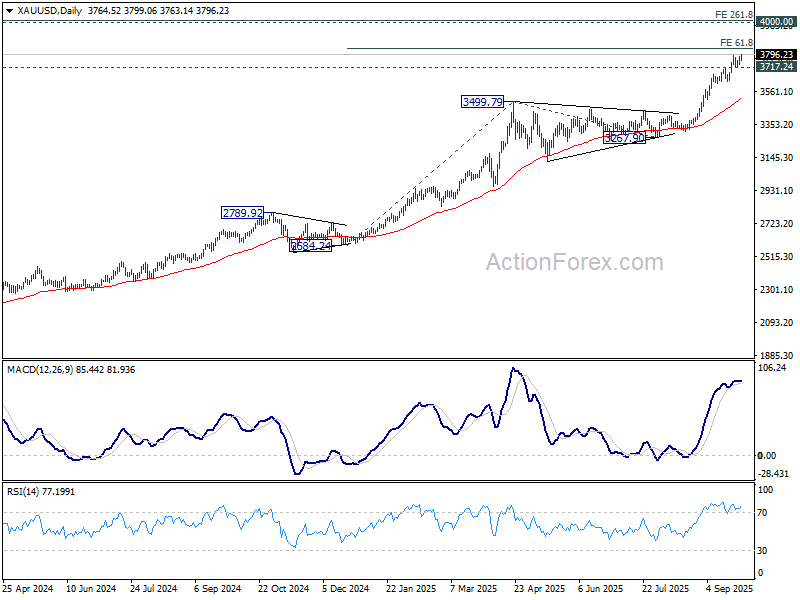

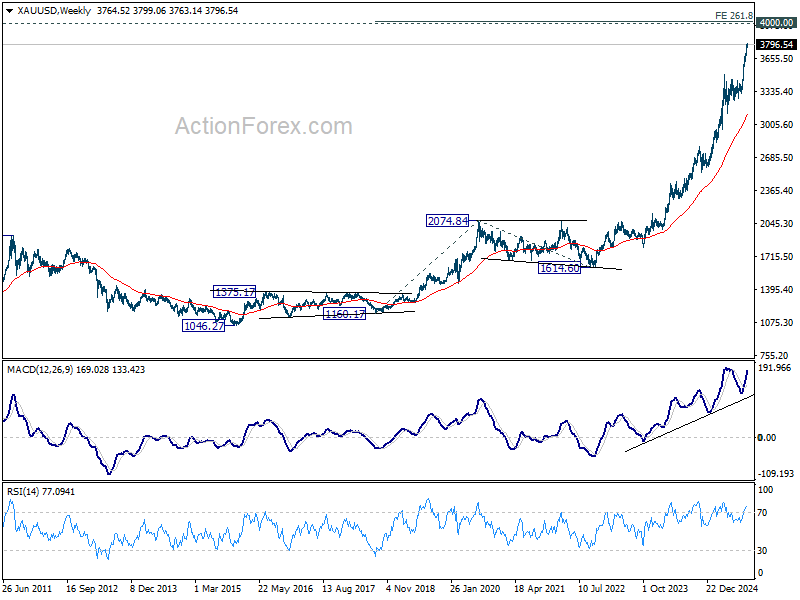

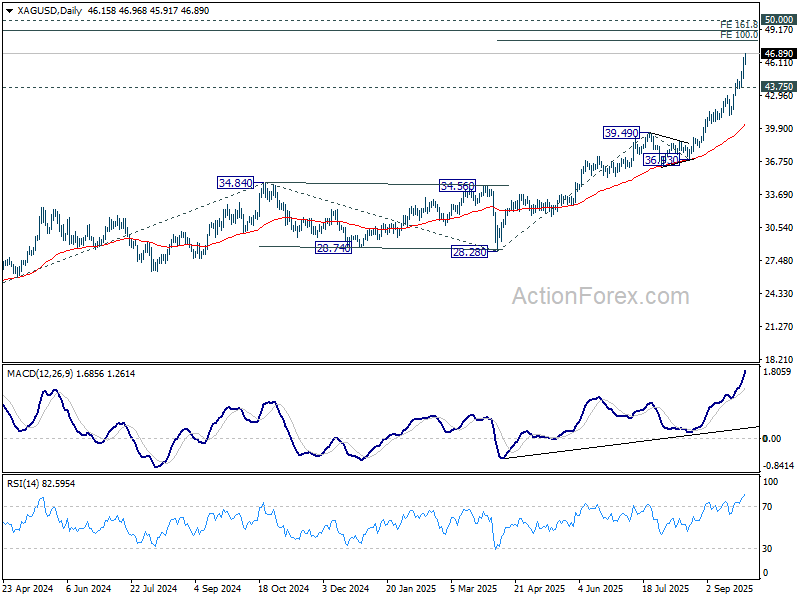

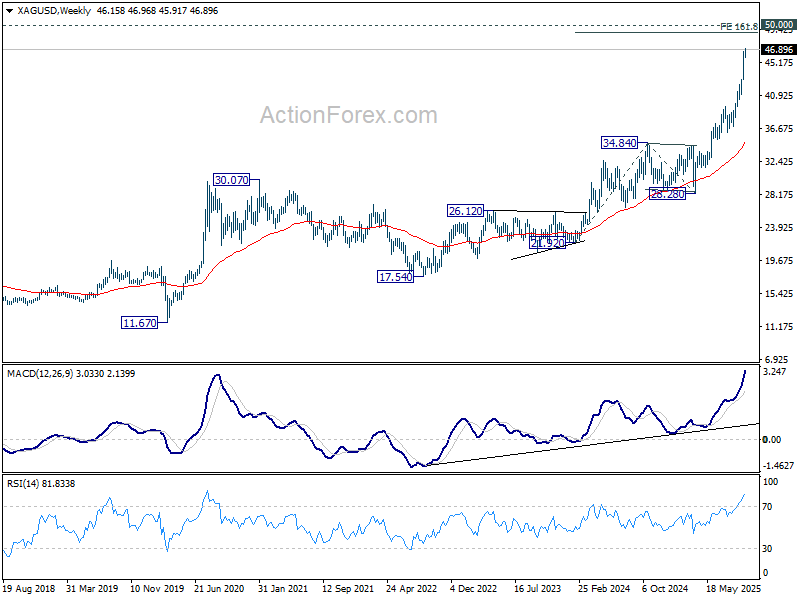

Gold and Silver rally near exhaustion points, caution warranted

Gold surged to another record in Asian trading today, edging toward 3800 level, while Silver held firm around 46.5 after last week’s sharp 7% rise. Both metals remain supported by low interest rates and geopolitical risks, but the relentless rally is entering territory where traders should start to grow more cautious.

For Gold, the technical outlook still points higher as long as 3717.24 support holds. Immediate upside target is 61.8% projection of 2584.24 to 3499.79 from 3267.90 at 3833.79. Yet as prices stretch further, momentum could start fading even as new highs are made, on overbought conditions.

The 4000 psychological barrier looms as a potential turning point. That zone also aligns with the 261.8% projection of 1160.17 to 2074.84 from 1614.60 at 4009.20, making it an ideal level for a major top. Traders should view this area as one to scale out, not chasing higher.

As Gold could also complete its five-wave rally from 1046.27 (2015 low), reversal at or near 4000 could be steep. The next meaningful correction might drag Gold quickly back toward 55 W EMA (now at 3113.80).

Silver carries similar warning signs. With support intact at 43.75, further rise should be seen to 100% projection of 28.28 to 39.49 from 36.93 at 48.14. But momentum is already running into a zone where upside looks limited relative to risk.

Between 161.8% projection of 21.92 to 34.84 from 28.28 at 49.18 and 50 psychological level, Silver faces a heavy resistance band that could complete its five-wave rally from 17.54 (2022 low). If rejected by 50, the metal could retrace rapidly, mirroring the kind of correction gold risks at 4000.

The message is clear: while fundamentals still favor precious metals, the technical picture is flashing caution. Traders should be tightening stops and locking in gains above 3800 in Gold and 48 in Silver, and be prepared for the possibility of sharp reversals.

Non-farm payrolls to decide fate of December Fed cut

Markets step into the final quarter of 2025 facing a dense calendar of high-stakes events. The spotlight is firmly on the US, with September’s non-farm payrolls and the ISM surveys set to guide the next leg of Fed expectations. After a run of resilient US data, investors are questioning how much scope remains for additional easing this year.

The October cut is still priced as near-certain, but the conviction for a follow-up move in December has started to erode. Markets increasingly see the Fed delivering just one more insurance cut to cushion the labor market rather than embarking on a deeper easing cycle. Unless data takes a sudden turn lower, the prospect of a year-end move will diminish further.

Non-farm payrolls will be the main test. A solid report would likely drive December cut odds even lower, especially if job creation show sign of rebound. By contrast, a weaker-than-expected number could revive market conviction that the Fed will act twice more this year, but such an outcome looks less probable after the recent run of firm data.

In the run-up to NFP, sentiment may shift on a series of important releases. Consumer confidence and ISM Manufacturing will all feed into the growth narrative, as well as ISM Services after NFP. These interim prints may create volatility across Dollar pairs, but none are expected to fundamentally challenge the October cut baseline.

In the Asia-Pacific, the RBA holds its policy meeting, where rates are widely expected to remain at 3.60%. The subtle hawkish lean from Governor Michele Bullock, combined with an upside surprise in August CPI, has already prompted traders to scale back bets on a November cut. Bullock’s tone this week will be crucial in gauging how seriously the Board views resurgent price pressures from strong domestic demand.

Should Bullock’s comments reinforce hawkish expectations, Australian Dollar could find support, particularly in the crosses. Even without an outright shift in forward guidance, a firmer stance on inflation risks could differentiate AUD from its weaker commodity peers.

Japan also enters the spotlight with the BoJ’s Summary of Opinions from the September meeting due. The release could shed more light on the growing internal divide, after two members dissented in favor of a hike. Any evidence that additional board members are edging toward that camp would sharpen expectations for an earlier move.

Alongside the Summary, the Tankan survey will provide a critical gauge of corporate sentiment and investment intentions, both essential inputs for BoJ’s policy deliberations.

In Europe, CPI releases from the Eurozone and Switzerland round out the week, likely confirming steady stances from both the ECB and SNB.

Here are some highlights for the week:

- Monday: UK M4 money supply, mortgage approvals; US pending home sales.

- Tuesday: BoJ summary of opinions, industrial production, retail sales; New Zealand ANB business confidence; RBA rate decision; China PMIs; Germany import prices, retail sales, unemployment; UK Q2 GDP final; Swiss KOF economic barometer; US house price index, Chicago PMI, consumer confidence.

- Wednesday: Japan Tankan survey, PMI manufacturing final; Swiss retail sales, PMI manufacturing; Eurozone PMI manufacturing final, CPI flash; US ADP employment, ISM manufacturing; BoC summary of deliberations.

- Thursday: Japan monetary base, consumer confidence; Australia trade balance, household spending; Swiss CPI; Eurozone unemployment rate; US jobless claims, factory orders.

- Friday: Japan unemployment rate; Eurozone PMI services final, PPI; UK PMI services final; US non-farm payrolls, ISM services.

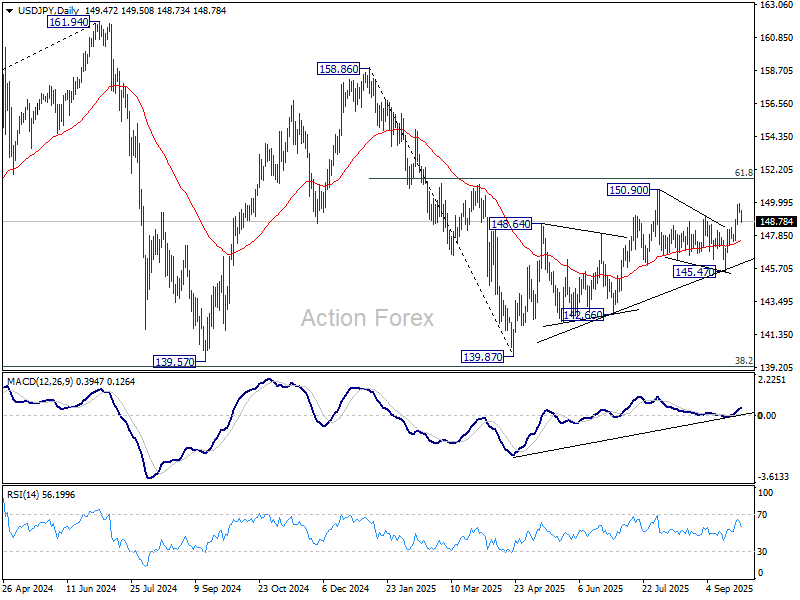

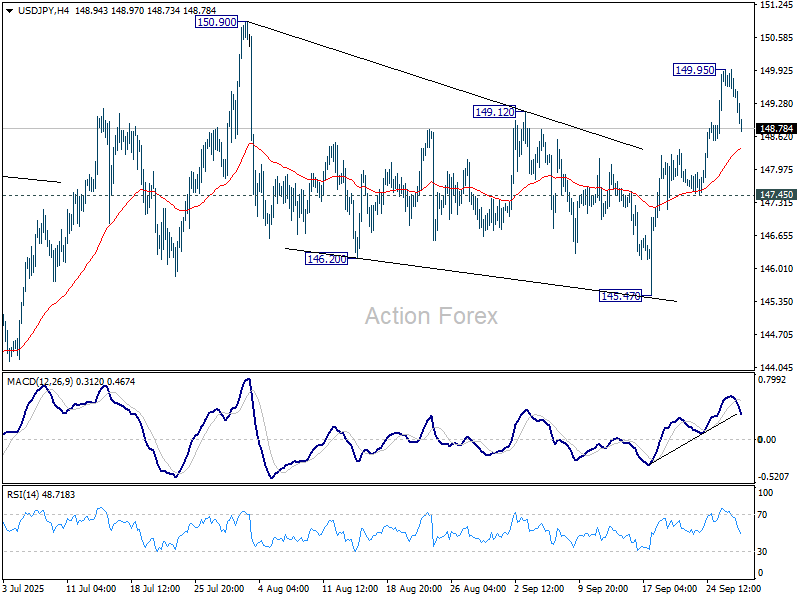

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.28; (P) 149.62; (R1) 149.83; More…

Intraday bas in USD/JPY is turned neutral first as retreat from 149.95 deepens. Some consolidations would be seen first but further rally is expected as long as 147.45 support holds. Corrective pattern from 150.90 should have completed at 145.47. Above 149.95 will bring retest of 150.90 first. Firm break there will target 151.22 fibonacci level. However, sustained break of 147.45 will dampen this bullish view and bring deeper fall to 145.47 support instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.