Calm Returns as Markets Bet on U.S.–China De-escalation – Action Forex

Global markets were notably calmer today as investors looked past last week’s turbulence and welcomed signs of a tentative thaw in U.S.–China trade relations. Asian stocks, which opened sharply lower, managed to recover most of their earlier losses by the close, while both European indexes and U.S. futures traded higher. The relative calm suggested that sentiment, while still cautious, was no longer gripped by fears of an immediate escalation in the trade conflict.

The improved mood followed remarks from U.S. Treasury Secretary Scott Bessent, who confirmed that President Donald Trump remains on track to meet with Chinese President Xi Jinping at the APEC summit in South Korea later this month. Bessent told Fox Business that the two sides have engaged in substantial communications over the weekend and that tensions have “substantially de-escalated” since Friday’s exchange of threats.

Bessent emphasized that the planned 100% tariffs on Chinese imports would not take effect until November 1, leaving a window for diplomacy. Dialogue channels remain open, while staff-level meetings will take place in Washington this week on the sidelines of the World Bank and IMF annual gatherings. These discussions could lay the groundwork for progress before the leaders’ meeting.

While Bessent struck a reassuring tone, he maintained that Washington retains leverage should diplomacy fail. “If not, we have substantial levers we can pull,” he warned, adding that “we could move more aggressively than China has” and that “everything’s on the table.”

In the currency markets, most major pairs were confined within Friday’s ranges. Dollar traded on the firmer side, joined by Aussie and Kiwi, while Swiss Franc, Yen, and Euro softened slightly. Sterling and Loonie hovered in mid-range positions.

In Europe, at the time of writing, FTSE is down -0.05%. DAX is up 0.35%. CAC is up 0.18%. UK 10-year yield is down -0.013 at 4.66. Germany 10-year yield is down -0.013 at 2.633. Earlier in Asia, Japan was on holiday. Hong Kong HSI lost -1.52%. China Shanghai SSE fell -0.19%. Singapore Strait Times fell -0.84%.

Greene says BoE should skip some rounds of rate cuts to tame inflation

BoE policymaker Megan Greene sounded a hawkish note today, warning that interest rates may need to stay elevated for an extended period to ensure inflation is fully subdued. She said monetary policy is “less restrictive than it had been,” a worrying sign given that price growth has shown renewed momentum over the past year.

While Greene believes the disinflation process “remains intact,” she expressed concern that it is losing pace, adding that inflation’s earlier spike above 11% has likely reshaped consumer and business behavior.

Ahead of Tuesday’s key U.K. wage and jobs data, Greene said the labor market appears to be stabilizing after a mild slowdown, having avoided the sharp deterioration some had feared earlier in the year. That resilience, combined with lingering inflation pressures, supports the case for patience before cutting rates again.

To ensure inflation is fully defeated, Greene argued that the Bank Rate should be “more restrictive than the market curve”, but without undermining the BoE’s credibility by alternating between hikes and cuts. Instead, she said the preferable path would be to keep rates “higher for longer”, and “skipping some rounds in terms of rate cuts.”

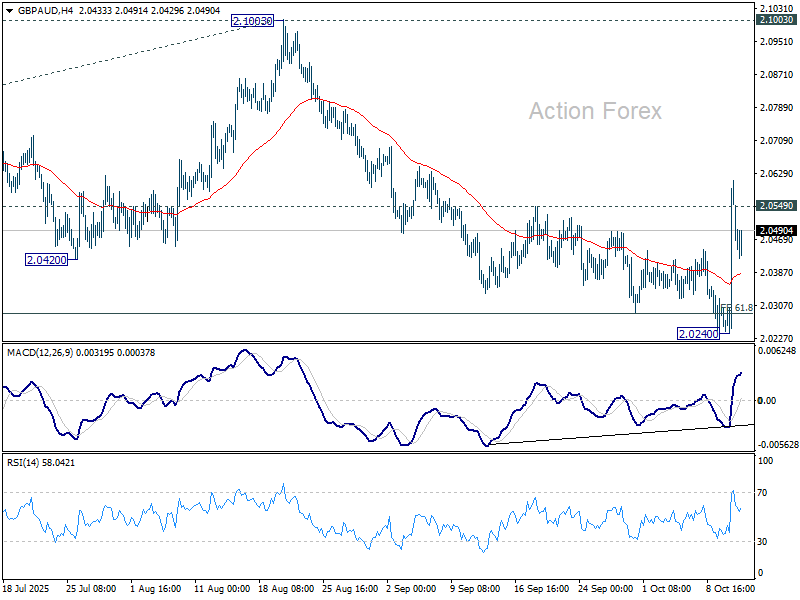

GBP/AUD in focus ahead of key UK, Australia events; Near-term upside bias holds

GBP/AUD will be a pair to watch this week as a string of key economic releases from both the U.K. and Australia promise to inject volatility. There will be RBA meeting minutes and U.K. labor market data on Tuesday, followed by Australian employment and U.K. GDP figures on Thursday. The cross has already shown renewed strength, rebounding firmly after a period of weakness, and traders are positioning for fresh direction from the incoming data.

Australian Dollar endured a setback late last week after the U.S.–China trade war flared up again, sending risk sentiment tumbling. Yet, the currency has stabilized on Monday, suggesting that markets are refocusing on domestic fundamentals rather than external shocks. Attention now turns to whether the RBA’s November policy meeting will bring another rate cut, a decision clouded by conflicting economic signals.

Recent data indicate that Australia’s economy is regaining momentum, supported by stronger consumer spending and rising house prices. However, this recovery has been accompanied by slower employment growth and upside surprises in inflation, leaving the RBA in a delicate position. Policymakers must weigh whether the rebound is sustainable enough to delay further easing, or if lingering labor market slack warrants additional stimulus. Tomorrow’s employment report and the Q3 CPI later in the month could tip the balance either way.

In the U.K., the policy outlook is equally nuanced. The BoE’s Monetary Policy Committee remains split, though the hawkish voices have grown louder in recent weeks. Chief Economist Huw Pill underscored that monetary policy should stay “resolutely focused on price stability,” while MPC member Catherine Mann argued for keeping rates restrictive despite weak consumption, warning that high inflation continues to weigh heavily on households.

Still, policymakers have stressed that their stance will remain data-dependent, placing a spotlight on Tuesday’s labor data—particularly wage growth—as a key input ahead of the next meeting. A firmer set of figures could reinforce the BoE’s cautious approach toward easing, lending further support to Sterling against the Aussie.

Technically, GBP/AUD’s rebound and break of 2.0549 resistance suggests that a short term bottom was already formed at 2.0240, on bullish convergence condition in 4H MACD. It’s also possibly that fall from 2.6143 (April high) has completed as a three-wave correction after hitting 61.8% projection of 2.1643 to 2.0478 from 2.1003 at 2.0283. For now, risk will stay mildly on the upside as long as 2.0240 support holds. Sustained trading above 55 D EMA (now at 2.0524) will affirm this bullish case, and target 2.1003 resistance for confirmation.

China trade in September, exports and imports surge, surplus narrows

China’s trade figures for September delivered a mixed picture. Exports rose 8.3% yoy, well above forecasts of 6.0% and marking the fastest pace in six months. Imports jumped 7.4% yoy, the strongest gain since April 2024 and far exceeding expectations of 1.5%.

However, the details showed signs of strain beneath the surface. Exports of rare earths—a key strategic material—fell -30.9% from August to 4,000 tonnes, the lowest level since February, amid tighter export restrictions. Meanwhile, soybean imports surged to the second-highest level on record, boosted by heavy purchases from South America as buyers avoided U.S. supplies in response to the escalating trade conflict.

Overall, China’s trade surplus narrowed to USD 90.5B from USD 102.3B, undershooting expectations of USD 98.5B. The surplus with the U.S. widened to USD 22.8B, even as total bilateral trade continued to shrink—exports to the U.S. fell nearly -17% in the first three quarters, while imports declined -11.6%. At the same time, trade deficit with Russia expanded to its widest level in six months at USD 2.1B.

NZ BNZ services at 48.3, contracts for 19th month as signs of strain persist

New Zealand’s services sector remained mired in contraction in September, with BNZ Performance of Services Index edging up modestly from 47.6 to 48.3. While the improvement marks a slight lift in momentum, the index has now stayed below the 50-point expansion threshold for 19 consecutive months.

Activity and sales rose to 47.8, and new orders improved to 49.6, but both remained in negative territory. Employment slipped to 47.8, reflecting ongoing caution among firms facing soft sales and squeezed margins.

BNZ reported that 58% of survey comments were negative, only marginally below August’s 59.6%. Respondents cited weak consumer confidence, rising living costs, and reduced discretionary spending as key drags. Many businesses also noted clients delaying projects and contracts amid broader economic uncertainty.

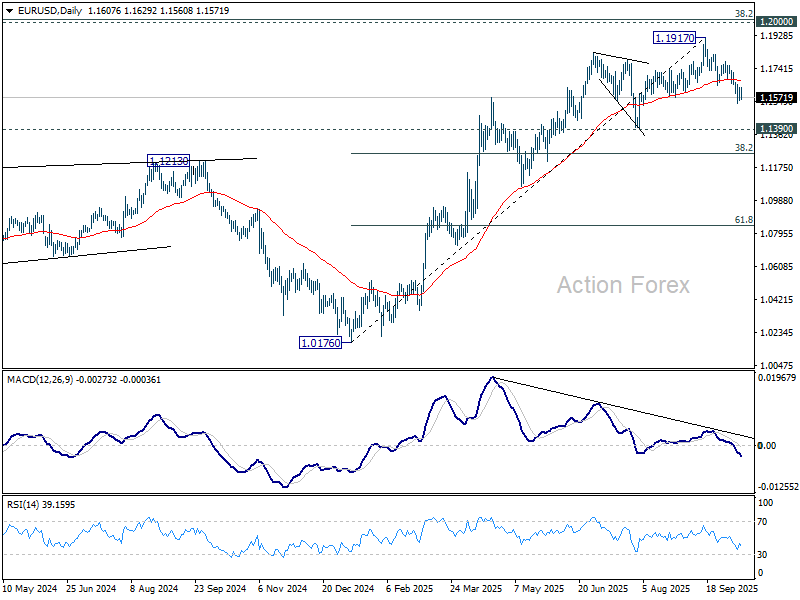

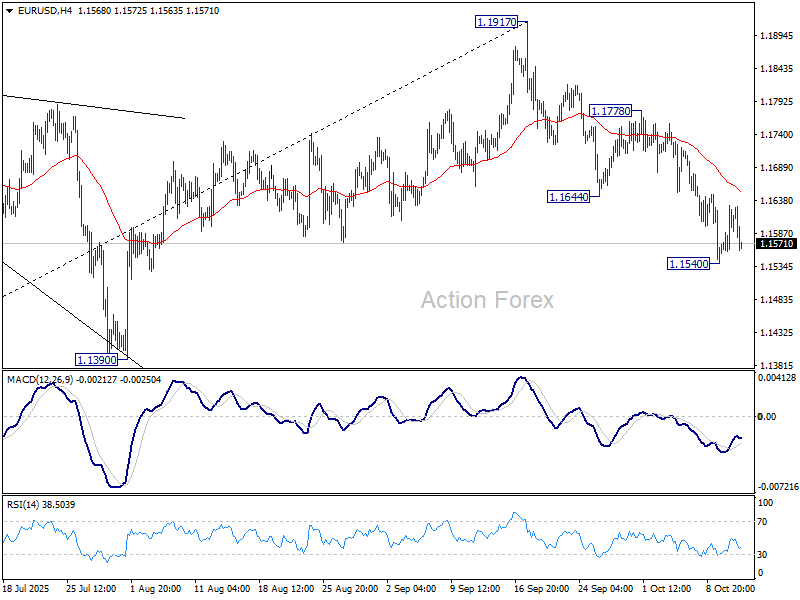

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1573; (P) 1.1601; (R1) 1.1651; More…

EUR/USD dips mildly today but stays above 1.1540 temporary low. Intraday bias remains neutral for more consolidations. Deeper decline is expected as long as 1.1778 resistance holds. On the downside, break of 1.1540 will resume the fall from 1.1917 to 1.1390 , or further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1247) holds, the up trend from 0.9534 (2022 low) is still extended to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.