Nikkei Slumps as Investors Question Full Return of Abenomics Under Takaichi, Commodity Currencies Sink – Action Forex

Sentiment soured sharply in Asian markets, led by a steep selloff in Japan where the Nikkei reversed early gains to fall more than 3%. The downturn reflected a mix of political uncertainty in Tokyo and renewed caution over U.S.–China trade tensions. After months of strong gains, Japanese equities appear to have reached a point where investors are pausing to reassess the outlook amid rising volatility and shifting policy expectations.

The source of anxiety lies partly in Japan’s unfolding leadership transition. While LDP leader Sanae Takaichi remains widely expected to become Japan’s next prime minister, her path to confirmation has been complicated by the breakup with coalition partner Komeito. The split has introduced a small but symbolic risk that an opposition figure could be elected by parliament later this month — a scenario still viewed as unlikely but unsettling enough to spark caution among investors.

Adding to the uncertainty, Finance Minister Katsunobu Kato emphasized today that “inflation, rather than deflation, has become a challenge for us now.” He emphasized the need for policies suited to this new environment, implying that Japan is unlikely to return to a full-fledged “Abenomics” reflationary stance even if Takaichi takes office. The remarks reinforce expectations that fiscal and monetary policies may remain more balanced, tempering hopes for aggressive stimulus measures that had previously fueled market optimism.

Beyond domestic politics, escalating U.S.–China trade tensions also weighed on investor sentiment. With Washington and Beijing trading fresh barbs over tariffs and rare earth restrictions, Japanese exporters face renewed headwinds. After a strong rally since April, profit-taking was perhaps overdue, and today’s selloff appears to reflect a broader correction rather than a fundamental shift in outlook.

Overall in the currency markets, Aussie led declines, followed by Kiwi and Loonie, all under pressure from the deterioration in sentiment and weaker equities. In contrast, the safe-haven trio, Yen, Swiss Franc and Euro, gained. Dollar and British Pound held in mid-range.

In Asia, at the time of writing, Nikkei is down -2.68%. Hong Kong HSI is down -0.19%. China Shanghai SSE is up 0.21%. Singapore Strait Times is down -0.22%. Japan 10-year JGB yield is down -0.00at 1.663. Overnight, DOW rose 1.29%. S&P 500 rose 1.56%. NASDAQ rose 2.21%.

RBA minutes signal caution as board flags risk of hotter Q3 inflation

RBA’s September meeting minutes confirmed a steady hand on policy, with members concluding there was “no need for an immediate reduction” in the cash rate. The Board agreed that the economic data and forecasts since August supported maintaining the current level of restrictiveness, while emphasizing that decisions will remain “cautious and data dependent.”

Discussions focused heavily on inflation risks, particularly after stronger readings in the monthly CPI indicators for July and August. While acknowledging that these data are partial and volatile, members noted that upside surprises in market services and housing costs suggest the September quarter CPI could come in higher than expected in August forecasts.

The minutes revealed growing concern that if this pattern continues, the Bank’s assumptions about the balance between aggregate demand and supply could be too optimistic. Members also referenced lessons from abroad, where services inflation has proven stubbornly elevated, as a warning for domestic policy calibration.

Still, the Board recognized that risks remain “two-sided”. On the upside, consumption could recover faster than assumed, or capacity pressures could prove stronger. On the downside, members highlighted the drag from weak consumer sentiment, slower employment growth, and subdued wage indicators.

The balance of views suggests the RBA will tread carefully in coming months, awaiting confirmation from the full Q3 inflation report before deciding whether further policy easing remains justified at the November meeting.

New Philly Fed chief Paulson backs gradual easing toward neutral policy

New Philadelphia Fed President Anna Paulson used her debut speech to call for a balanced approach to monetary policy as the economy navigates rising labor market risks and uncertain inflation dynamics.

She said policy should move toward a “more neutral stance,” stressing that the Fed must weigh both sides of its mandate. While she noted that the job market remains solid overall, she warned that conditions are “moving in the wrong direction” and that risks are “noticeably” increasing.

Paulson indicated she supports a measured pace of rate cuts consistent with the Fed’s latest projections, which outlined a quarter-point reduction last month and an additional 50 basis points of easing before the end of 2025, followed by further cuts in subsequent years.

On inflation, Paulson acknowledged that the recent tariff hikes could lift prices modestly, but said she does not expect those effects to persist. Still, she cautioned against rushing into deeper rate reductions given uncertainty over where the neutral rate truly lies.

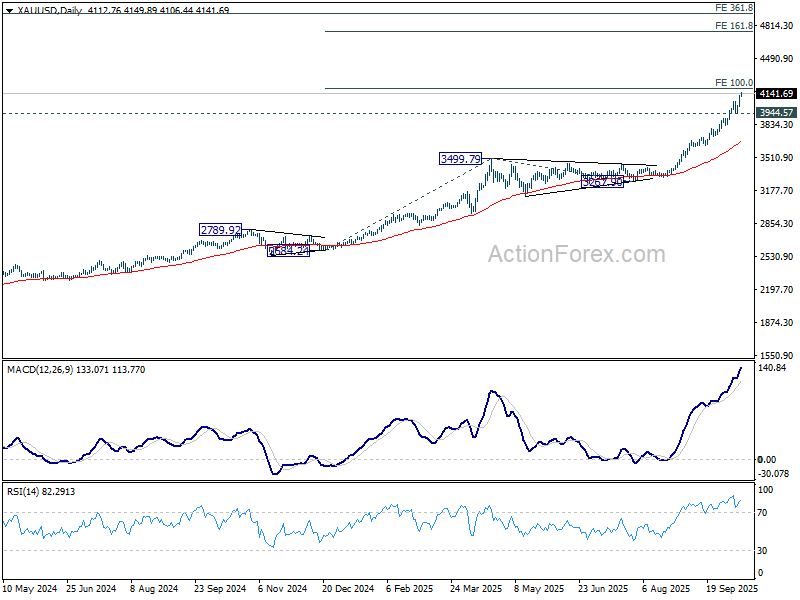

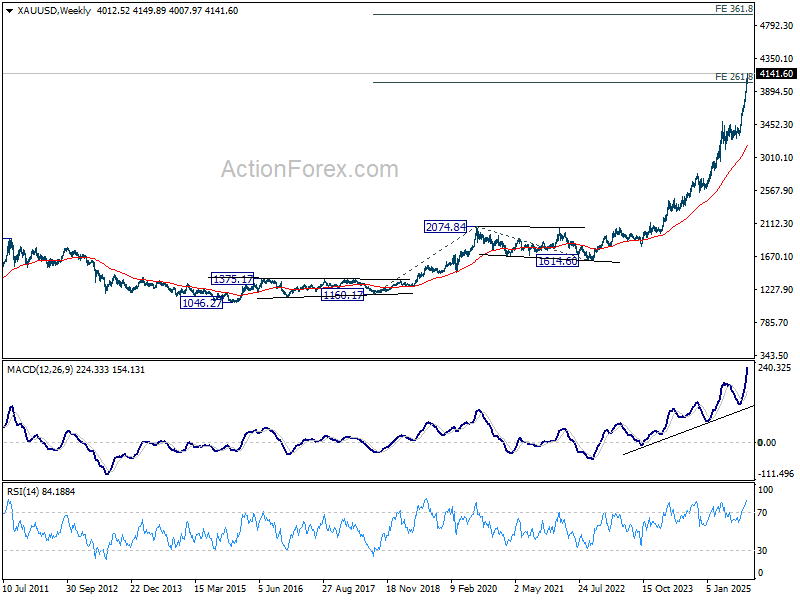

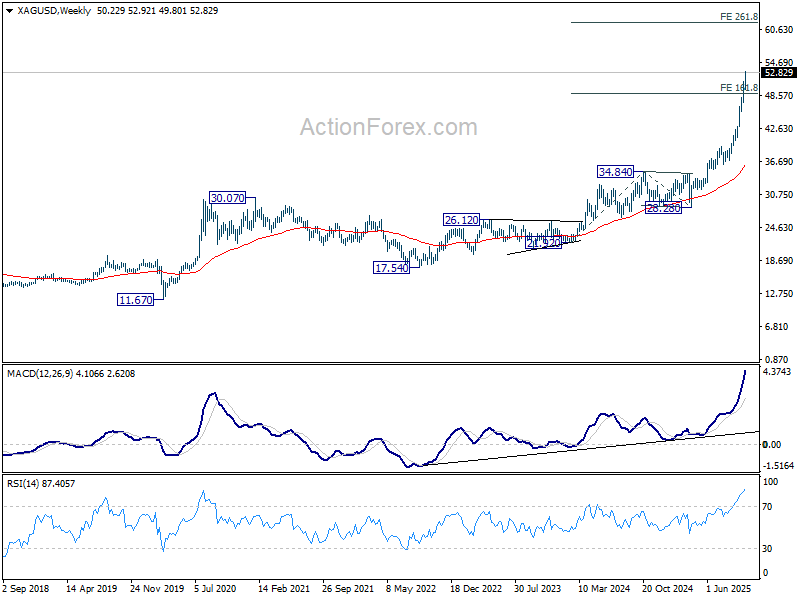

Gold and Silver shatter key barriers as bull run accelerates – 5000 and 60 next

The precious metals rally showed no sign of fatigue, with Gold surging beyond 4,000 and Silver clearing 50 in a powerful continuation of their uptrend. Neither milestone proved a deterrent, as safe-haven demand strengthened amid renewed global uncertainty. Although initial market reactions to the latest U.S.–China trade tensions were subdued, investors have steadily rotated back into metals, betting that geopolitical instability will sustain demand well into 2026.

The rally has now reached a stage where institutional forecasts are catching up to price reality. On Monday, Bank of America became the first major institution to lift its long-term targets, projecting Gold at 5,000 per ounce in 2026 and Silver at 65.

Silver remains the outperformer, up about 80% year-to-date, compared with a 55% rise in gold. However, the surge has not come without risks. Some analysts caution that as liquidity improves and industrial demand fluctuates, volatility could increase in the near term. The latest spike has also been fueled by a temporary shortage in physical supply, which is expected to ease soon.

Technically, Gold’s next immediate focus lies at 100% projection of 2,584.24 to 3,499.79 from 3,267.90 at 4,183.45. Resistance could emerge there, prompting some profit-taking on first test. Break below 3,944.57 support would signal short-term topping and consolidation. However, sustained strength above 4,183.45 would pave the way toward 161.8% projection at 4,749.25 next.

In the broader view, now that 261.8% projection of 1,160.17 to 2,074.84 from 1,614.60 at 4,009.21 is cleared, Gold could be heading towards 361.8% projection at 4.923.87, which is close to 5000 psychological level. The technical setup aligns closely with the latest upward revisions from institutional forecasts.

For Silver, near term outlook will stay bullish as long as 48.35 support holds. Next target is 161.8% projection of 28.28 to 39.49 from 36.93 at 55.06. Firm break there will target 200% projection at 59.35, which is close to 60 psychological level.

In the bigger picture, the up trend remains in acceleration phase, and could further stretch to 261.8% projection of 21.92 to 34.84 from 28.28 at 62.10 in the medium term.

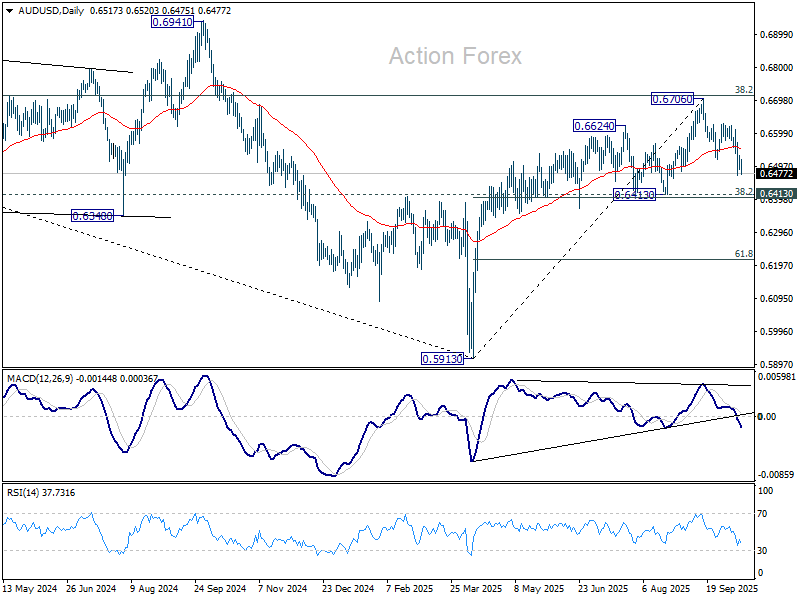

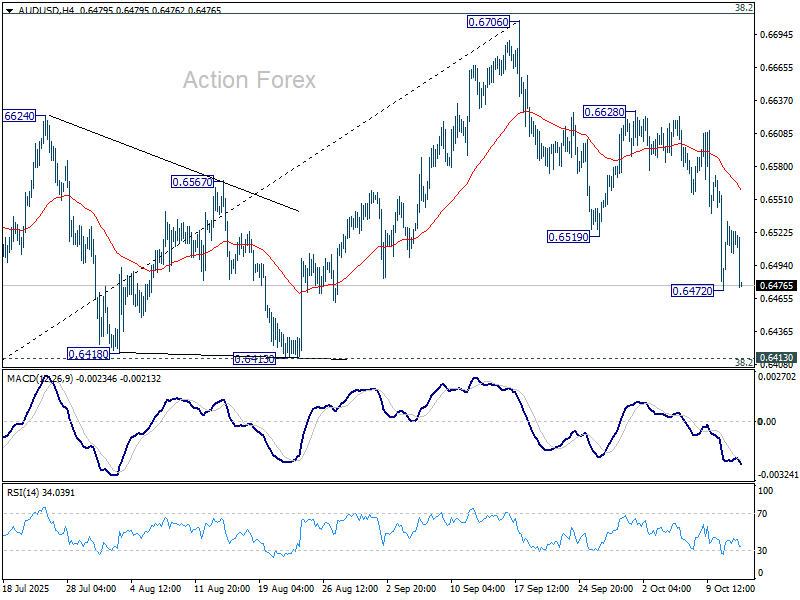

AUD/USD Daily Report

Daily Pivots: (S1) 0.6492; (P) 0.6513; (R1) 0.6534; More...

AUD/USD falls sharply today but stays above 0.6472 temporary low. Intraday bias remains neutral first and more consolidations could be seen. Still, risk will remain on the downside as long as 0.6628 resistance holds. Current development suggests rejection by 0.6713 fibonacci resistance. Below 0.6472 will resume the fall from 0.6706 to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.