Risk-Off Mood Deepens as U.S.–China Trade War Expands to Shipping – Action Forex

Global markets turned sharply defensive today as renewed U.S.–China trade tensions reignited fears of broader economic disruption. Equities fell across Asia and Europe, while safe-haven demand lifted Yen and Dollar. The latest flashpoint emerged at sea, where both countries introduced new port charges on ocean shipping firms, adding a fresh dimension to the ongoing trade confrontation.

Beijing announced that it would begin collecting special charges on U.S.-owned, operated, built, or flagged vessels. Washington, in turn, rolled out its own fees on Chinese-linked shipping companies. In another retaliatory step, China also sanctioned five U.S.-linked subsidiaries of South Korea’s Hanwha Ocean, accusing them of aiding a U.S. investigation into Chinese trade practices.

The risk-off tone spread swiftly through financial markets. Investors rotated into safe-haven currencies, with the Yen leading gains, followed by Dollar and Swiss Franc, while risk-sensitive units — Aussie, Kiwi and Sterling — underperformed. Euro and Canadian Dollar held to mid-range positions.

Adding to Sterling’s weakness, U.K. labor market data showed further signs of cooling. The combination of softer wage growth and rising unemployment gave the report a dovish tilt. However, policymakers are unlikely to pivot toward immediate easing yet. Despite the cooling trend, total pay growth remains elevated, and inflation is expected to tick higher to 4% in September, keeping the BoE cautious.

In Europe, at the time of writing, FTSE is down -0.45%. DAX is down -1.23%. CAC is down -1.00%. UK 10-year yield is down -0.066 at 4.594. Germany 10-year yield is down -0.03 at 2.607. Earlier in Asia, Nikkei fell -2.58%. Hong Kong HSI fell -1.73%. China Shanghai SSE fell -0.62%. Singapore Strait Times fell -0.80%. Japan 10-year JGB yield fell -0.033 to 1.663.

German ZEW edges higher to 39.3, but Eurozone sentiment slips on French turmoil

Germany’s ZEW Economic Sentiment Index rose modestly in October to 39.3, up from 37.3 but below expectations of 41.7. Current Situation Index deteriorated further from -76.4 to –80.0, undershooting forecasts of –75.0.

ZEW President Achim Wambach noted that experts “are still hoping for an upturn in the medium term,” but persistent global uncertainties and questions over Berlin’s state investment program continue to weigh on confidence.

Sectorally, expectations improved in several export-oriented industries after a recent slump in shipments to China. However, the automotive sector—long Germany’s industrial backbone—remains an exception with “slightly deteriorating indicator.”

Across the broader Eurozone, confidence took a sharper turn lower. ZEW Economic Sentiment Index dropped to 22.7 from 26.1, missing expectations of 30.2. Current Situation Index plunged by -30 points to –31.8. ZEW attributed the decline largely to political instability in France and ongoing budget disputes.

BoE’s Taylor sees mounting downside risks, says trade diversion aiding disinflation

BBoE MPC member Alan Taylor, one of the committee’s most dovish voices, warned that the U.K. economy faces a “preponderance of downside risks” as growth slows and labor market slack widens.

In a speech today, he said output has fallen below potential, confidence among firms and households remains weak, and the trend of disinflation continues to deepen. Wage settlements are now expected to end the year around 3–3.5%, moving lower into 2026 — a sign, he argued, that “wage-led domestic inflation will not re-kindle an upward spiral.”

Taylor also pointed to global trade dynamics as a growing disinflationary force. He noted that U.K. import prices, particularly from Europe, have been falling for several years and are likely to decline further as “trade diversion” accelerates — a process through which supply chains shift across regions, increasing competition and reducing goods prices.

While acknowledging that the 2025 inflation hump and moderate expectations pose some upside risk, Taylor said these should fade by early 2026 as earlier tax and administered price effects roll off. With inflation fundamentals softening and external price pressures subsiding, he maintained that the balance of risks justifies a lower path for Bank Rate, consistent with his repeated dissents at recent MPC meetings.

UK payrolled employment falls -10k, but wages growth still firm

The latest U.K. labor market figures painted a mixed picture for September, highlighting a slowdown in hiring momentum alongside still-solid wage growth. Payroll employment fell by -10k. Claimant count rose sharply by 25.8k, well above expectations for a modest 10.3k increase.

At the same time, wage growth remains resilient, albeit easing from its prior peak. Median monthly pay increased by 5.5% yoy, down from 6.5% in August but still within the tight range seen since the start of the year.

Over the three months to August, unemployment rate ticked up to 4.8%, slightly higher than the expected 4.7%. Meanwhile, average earnings including bonuses rose 5.0% yoy, beating forecasts of 4.7% yoy. Pay growth excluding bonuses slowed to 4.7% yoy, in line with expectations.

Overall, the figures reinforce the view of a gradual cooling in the labor market rather than a sharp deterioration. Elevated wage pressures will remain a key concern for the BoE.

RBA minutes signal caution as board flags risk of hotter Q3 inflation

RBA’s September meeting minutes confirmed a steady hand on policy, with members concluding there was “no need for an immediate reduction” in the cash rate. The Board agreed that the economic data and forecasts since August supported maintaining the current level of restrictiveness, while emphasizing that decisions will remain “cautious and data dependent.”

Discussions focused heavily on inflation risks, particularly after stronger readings in the monthly CPI indicators for July and August. While acknowledging that these data are partial and volatile, members noted that upside surprises in market services and housing costs suggest the September quarter CPI could come in higher than expected in August forecasts.

The minutes revealed growing concern that if this pattern continues, the Bank’s assumptions about the balance between aggregate demand and supply could be too optimistic. Members also referenced lessons from abroad, where services inflation has proven stubbornly elevated, as a warning for domestic policy calibration.

Still, the Board recognized that risks remain “two-sided”. On the upside, consumption could recover faster than assumed, or capacity pressures could prove stronger. On the downside, members highlighted the drag from weak consumer sentiment, slower employment growth, and subdued wage indicators.

The balance of views suggests the RBA will tread carefully in coming months, awaiting confirmation from the full Q3 inflation report before deciding whether further policy easing remains justified at the November meeting.

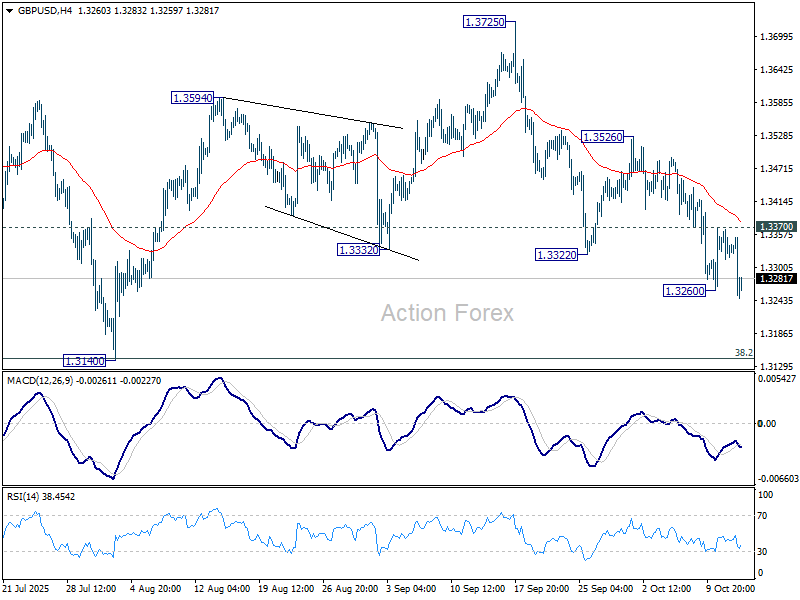

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3309; (P) 1.3338; (R1) 1.3360; More…

Breach of 1.3260 suggests that GBP/USD’s fall is resuming. Intraday bias is back on the downside for 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected from there to complete the corrective pattern from 1.3787. On the upside, above 1.3370 minor resistance will turn intraday bias neutral first.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3173) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.