Sterling Supported by Symbolic GDP Growth, Franc Under Pressure – Action Forex

Sterling traded slightly firmer as one of the day’s top performers. The modest 0.1% mom GDP growth in August confirmed that the UK economy continues to grind forward. While small, the uptick carries symbolic weight, reinforcing the notion that Britain’s slowdown is stabilizing heading into the final quarter of the year.

Markets are still divided over whether another rate cut is on the table for BoE’s November 6 decision. Inflation data in the coming weeks will be pivotal in shaping expectations. Another key variable is the outcome of the Chancellor’s upcoming budget on November 26, which could alter the BoE’s policy calculus. Given the uncertainty, a “wait-and-see” approach at the November meeting is plausible, allowing policymakers to assess the fiscal backdrop before committing to the next step.

Meanwhile, Swiss Franc weakened after Bern lowered the country’s 2026 growth forecast to 0.9%, citing U.S. tariffs as a “heavy burden” on its manufacturing and export sectors. The downgrade comes after Switzerland failed to secure a tariff exemption from Washington, leaving its goods subject to 39% duties—the steepest country-specific rate imposed under the Trump administration.

Trade headwinds have magnified downside risks for Switzerland’s export-reliant economy, where pharmaceuticals, machinery, and precision instruments dominate shipments abroad. sustained tariff exposure could dampen business confidence and delay investment decisions well into next year.

For the week so far, Sterling leads the major currencies, followed by the Aussie, which recovered despite soft labor data that boosted odds of a November RBA cut. Euro ranks third, supported by calmer political conditions in France. At the weaker end, Loonie, Dollar, and Yen lag, while Kiwi and Swiss Franc are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.22%. DAX is up 0.15%. CAC is up 0.98%. UK 10-year yield is down -0.025 at 4.525. Germany 10-year yield is up 0.003 at 2.578. Earlier in Asia, Nikkei rose 1.27%. Hong Kong HSI fell -0.09%. China Shanghai SSE rose 0.10%. Singapore Strait Times fell -0.28%. Japan 10-year JGB yield rose 0.001 to 1.657.

Fed’s Waller favors cautious 25bp cuts amid weak hiring, uncertain outlook

Fed Governor Christopher Waller told Bloomberg that even without the official employment data, the available evidence points to a clear slowdown in hiring across the U.S. economy. He noted that private and survey-based indicators have been consistent in signaling weaker labor demand, reinforcing the view that the job market is losing momentum.

Waller argued that this backdrop supports the case for the Fed to continue with measured 25bps rate cuts, emphasizing caution amid high uncertainty.

“We don’t know which way this is going to break,” he said. “If the labor market rebounds, there is less pressure to cut rates—you don’t want to make a mistake.”

Fed’s Miran backs 50bp cut, warns trade war add to downside growth risks

Fed Governor Stephen Miran said today that he would support a 50bps rate cut at the upcoming policy meeting, arguing that monetary policy remains too restrictive given the heightened risks surrounding U.S.–China trade tensions.

Speaking to Fox Business, Miran said that the escalation in trade uncertainty adds downside risks to growth and that the Fed must act preemptively to cushion the economy.

“If monetary policy stays as restrictive as it is, and you have a shock like this hit the economy, it does materially increase the negative consequences of that shock,” he warned.

Miran added that the outlook for next year’s growth will depend heavily on whether trade risks are “realized or defused” in the weeks ahead.

Eurozone trade surplus narrows, as exports to the US down -22.2% yoy

The Eurozone recorded a EUR 1.0B surplus in trade in goods with the rest of the world, down from EUR 3.0B a year earlier. Exports fell -4.7% yoy to EUR 205.9B, while imports declined -3.8% yoy to EUR 204.9B.

At the broader EU level, the picture was even weaker. The EU recorded a EUR- 5.8B deficit in August, widening from EUR -2.4B in the same month last year, as exports dropped -6.7% yoy and imports fell -4.9% yoy.

Looking at bilateral flows, EU’s exports to the US plunged -22.2% yoy, while imports from the U.S. dipped just -1.9% yoy, reducing the EU’s trade surplus to EUR 6.5B from EUR 15.3B a year earlier.

Trade with China also weakened, with exports down -11.3% yoy and imports falling -7.1% yoy, though the EUR -28.8B deficit narrowed slightly.

In contrast, trade with the UK remained relatively resilient—exports edged only -1.2% yoy lower, while imports dropped -8.5% yoy, leaving the EU’s surplus with the UK relatively steady at EUR 13.4B.

UK GDP expands 0.1% mom in August, growth patchy across sectors

The UK economy expanded modestly by 0.1% mom in August, in line with expectations, suggesting that activity remains subdued but stable. Industrial production rose 0.4% mom, helping to offset flat performance in the dominant services sector and a -0.3% mom contraction in construction.

On a three-month basis, GDP grew 0.3% in the period to August compared with the previous three months. The details were uneven: services output rose 0.4%, maintaining its role as the primary driver of growth, while production slipped -0.3% and construction gained -0.3%.

Australia jobless rate rises to 4.5%, highest since 2021

Australia’s labor market showed further signs of cooling in September as hiring momentum eased and the jobless rate climbed from 4.2% to 4.5%, the highest since November 2021. The unemployment rate figure exceeded expectations for 4.3%, driven by a 5.2% jump in the number of unemployed persons, equivalent to an increase of 33.9k people.

Total employment rose by 14.9k, undershooting forecasts of 20.0k. The breakdown showed full-time positions up 8.7k and part-time jobs rising 6.3k. Despite slower hiring, the participation rate edged up by 0.1% to 67.0%, indicating that more Australians are re-entering the labor force even as job creation moderates.

At the same time, monthly hours worked increased 0.5% mom, showing that those employed are still working longer hours on average, cushioning some of the weakness in headline employment figures.

RBA’s Bullock warns markets too optimistic, says trade war effects to linger for years

RBA Governor Michele Bullock cautioned today that financial markets may be underestimating global economic risks, warning that investors have taken a “Goldilocks view” of the outlook. Speaking at a forum, Bullock said markets appear to be “discounting the bad macroeconomic risks,” even as trade and geopolitical tensions threaten to slow global growth. She emphasized that the effects of the trade war will “play out over the next few years,” as tariffs are maintained or expanded by multiple countries, dampening trade and investment.

Bullock said the unpredictability of government responses to tariffs—rather than the general uncertainty surrounding them—was the biggest risk to investors’ confidence. “You just don’t know what might come out tomorrow morning,” she said, noting that sudden policy shifts could easily destabilize the currently “rosy” market outlook.

Addressing China’s economic struggles directly, Bullock pointed to the country’s ongoing deflationary pressures and excess industrial capacity, saying that “competing provinces” are cutting prices to maintain output, effectively exporting deflation to the rest of the world. She suggested that Beijing could do more to stimulate domestic consumption to rebalance its economy, adding that China’s “massive population” provides untapped potential demand if policies shift toward supporting households.

BoJ’s Tamura urges faster move toward neutral rate, warns against falling behind the curve

BoJ board member Naoki Tamura, one of the central bank’s most hawkish policymakers, who voted for a 25bps hike at the September meeting, reiterated his call for a faster shift toward a neutral policy stance. In a speech today, he said the current stance remains “far away from the neutral interest rate” the impact of prior rate hikes on the domestic economy has been “extremely limited.” He warned that keeping policy too loose for too long could invite future instability.

Tamura explained that his dissent was based on “risks to prices being skewed to the upside”. He now sees it as “more likely that the price stability target will be achieved earlier than expected,” helped by the recent Japan–U.S. tariff policy agreement, which he believes will support growth while keeping price momentum intact.

He acknowledged that U.S. tariff measures could weigh on the American economy, with spillover effects on Japan. But he emphasized “It is important from a risk management perspective for the Bank to move closer to a neutral monetary policy stance”.

Delaying further moves, he warned, could lead to Japan “falling behind the curve,” forcing abrupt rate hikes later that might “inflict significant damage” on the economy.

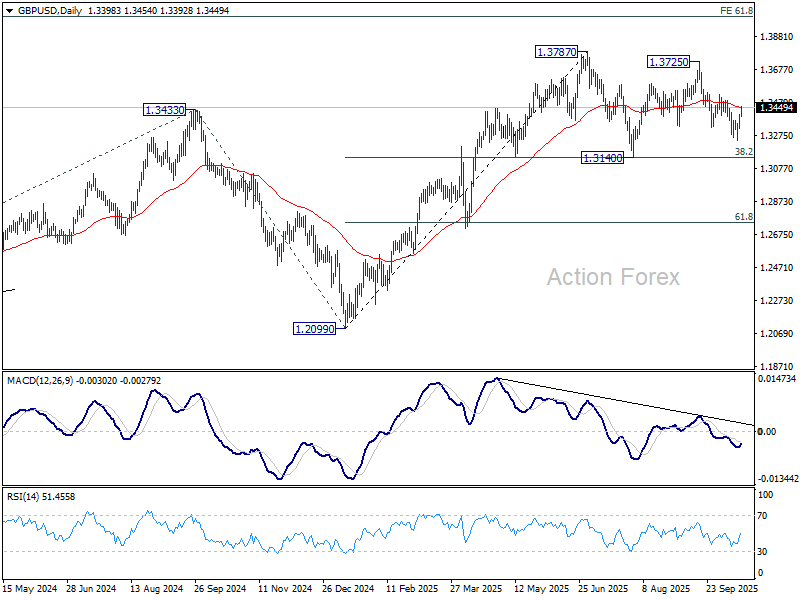

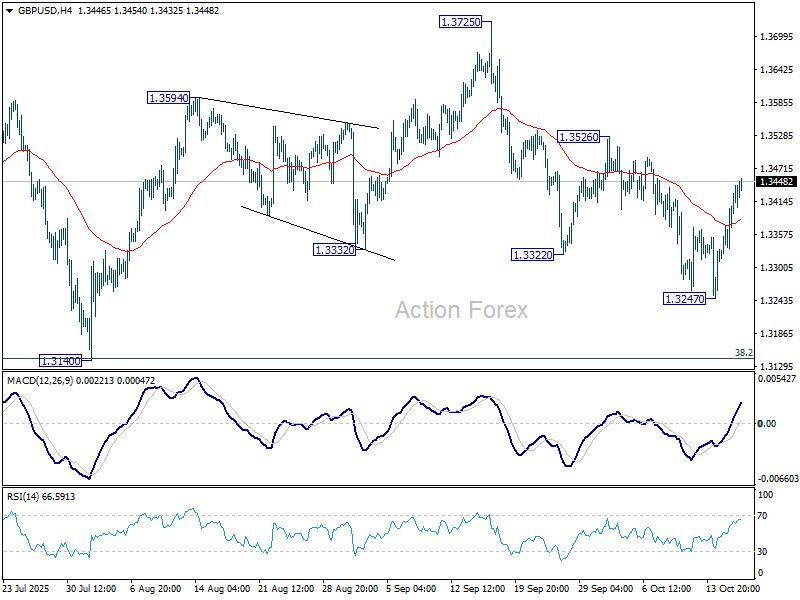

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3344; (P) 1.3376; (R1) 1.3435; More…

Intraday bias in GBP/USD remains neutral first. Fall from 1.3725 could still extend lower. But even in that case, Strong support is expected from 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142) to complete the corrective pattern from 1.3787. On the upside, break of 1.3526 will bring stronger rally back to 1.3725/87 resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3173) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.