Markets Edge Higher as Shutdown Deal Hopes Lift Sentiment – Action Forex

Global markets traded with a mildly positive tone as investors entered the U.S. session on Monday, buoyed by some optimism that the prolonged government shutdown could end within days. U.S. top White House economic adviser Kevin Hassett said on CNBC that a resolution was “likely to end sometime this week,” citing signals from the Senate that moderate Democrats may soon move to reopen the government after nationwide “No Kings” protests over the weekend.

Hassett also warned that if talks stall, the administration may adopt “stronger measures” to push Democrats toward cooperation. But markets appeared focused more on the potential for compromise than confrontation. His comments gave a modest lift to risk sentiment, helping equities stabilize after last week’s volatility.

Overall, investors appear cautiously optimistic but reluctant to chase risk ahead of confirmation that the US government will indeed reopen. A successful deal this week could add momentum to equities and higher-yielding currencies in the near term, while any renewed political brinkmanship might quickly unwind the fragile calm currently seen across global markets.

In forex markets, direction remained limited. Kiwi outperformed, followed by Swiss Franc and Dollar. Loonie was the weakest of the majors, trailed by Aussie and Yen, while Euro and Sterling traded largely sideways in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.38%. DAX is up 1.48%. CAC is up 0.15%. UK 10-year yield is down -0.025 at 4.512. Germany 10-year yield is up 0.001 at 2.585. Earlier in Asia, Nikkei rose 3.37%. Hong Kong HSI rose 2.42%. China Shanghai SSE rose 0.63%. Singapore was on holiday. Japan 10-year JGB yield rose 0.037 to 1.669.

BoJ’s Takata repeats call for rate hike warns inflation risks overshooting

BoJ board member Hajime Takata reinforced his hawkish stance today, arguing that Japan has roughly achieved the 2% inflation goal and now risks overshooting it. In a speech, Takata said steady gains in wages and prices show the economy is strong enough to withstand further normalization, calling the current environment a “prime opportunity to raise interest rates.”

Takata was one of two board members who dissented at the September meeting, when the BoJ voted to keep its policy rate at 0.5%. He instead proposed a 25bps hike to 0.75%.

Citing the BOJ’s October Tankan survey and feedback from branch managers, Takata said improvements in employment and income are supporting private consumption. He emphasized that both wage and price-setting behaviors have changed materially, signaling that Japan’s economy has entered a new phase after decades of deflationary mindset.

NZ CPI jumps to 3% in Q3, hits top of RBNZ target band

New Zealand’s inflation pulse picked up in the Q3, highlighting lingering price pressures that could restrain the RBNZ from cutting rates too aggressively. Headline CPI rose 1.0% qoq, above forecasts of 0.8% and sharply higher than 0.5% pace in Q2. On an annual basis, inflation climbed from 2.7% yoy to 3.0% yoy, matching expectations but reaching the top of the central bank’s target band and its highest level since mid-2024.

Much of the rebound came from tradeable prices, which rose 2.2% yoy versus 1.2% previously, suggesting imported cost pressures are resurfacing. By contrast, non-tradeable inflation eased slightly from 3.7% yoy to 3.5%, hinting at some moderation in domestic demand.

Even so, the composition of inflation is concerning: housing and utilities accounted for nearly one-third of the total rise in the annual CPI. Electricity prices jumped 11.3%, rents increased 2.6%, and local authority rates surged 8.8%.

With these three categories making up just 17% of the CPI basket, the data underline how sticky living costs have become. For the RBNZ, which only recently delivered an outsized 50bps rate cut to counter slowing growth, this renewed inflation uptick narrows its policy flexibility.

China GDP growth slows to 4.8% in Q3, property slump deepens

China’s GDP expanded 4.8% yoy in the Q3, the slowest pace in a year but still slightly ahead of expectations for 4.7%. Even so, with cumulative growth of 5.2% over the first nine months, China remains on track to meet its full-year target of “around 5%”.

Industrial production provided a bright spot, climbing 6.5% yoy in September, up sharply from August’s 5.2% and well above expectations of 5.0%. Retail sales also beat expectations of 2.9% yoy slightly, rising 3.0% even as the pace slowed from 3.4%, pointing to modest resilience in consumption.

Yet beneath the surface, the investment picture deteriorated further. Fixed-asset investment slipped -0.5% year-to-date yoy. Property investment fell -13.9%, extending the sector’s prolonged drag on growth. Private investment declined -3.1%, marking a deeper contraction than earlier in the year, and even ex-property investment slowed from 4.2% to 3.0% growth.

The data reaffirm that while parts of the industrial economy are stabilizing, domestic demand and investor sentiment remain fragile.

Bitcoin rebounds as market panic fades, consolidations seen between 101K–126K

Bitcoin rebounded sharply on Monday, regaining some footing after a two-week selloff driven by risk aversion across global markets. The recovery came as sentiment stabilized following an intense stretch of macro headwinds — including U.S. President Donald Trump’s renewed tariff threats on China and escalating worries over regional banks’ exposure to bad loans. Even expectations of Fed rate cuts failed to cushion the selloff.

With risk appetite showing tentative signs of recovery, Bitcoin rebounded alongside equities and other higher-beta assets. The technical picture, however, is not totally bullish.

The earlier break below 108,627 support confirmed that rise from 74,373 to 126,289 has likely completed its five-wave advance. Tentatively, price action from 126,289 is viewed as consolidations to the rise from 74,373 only.

A push above 116,074 would reinforce this view, and set up the range for the corrective pattern between 101,896 and 126,289. That would imply scope for further consolidation before another run to record highs. The structure suggests the market is resetting rather than reversing.

However, the broader trend shows signs of fatigue. W MACD continues to display bearish divergence, warning that upward momentum is fading. A break below 101,896 would put 55 W EMA (now at 96,913) in focus. Sustained move under that level would suggest a deeper correction of the entire uptrend from the 2022 low of 15,452.

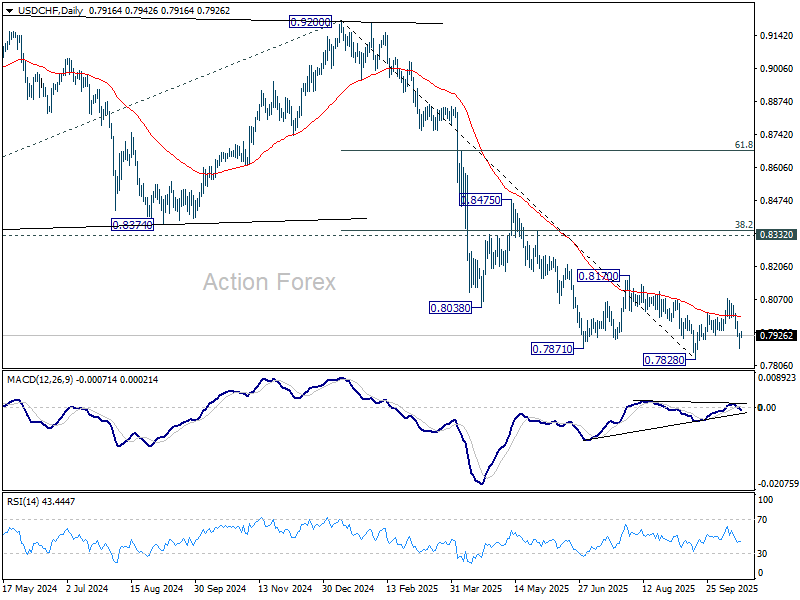

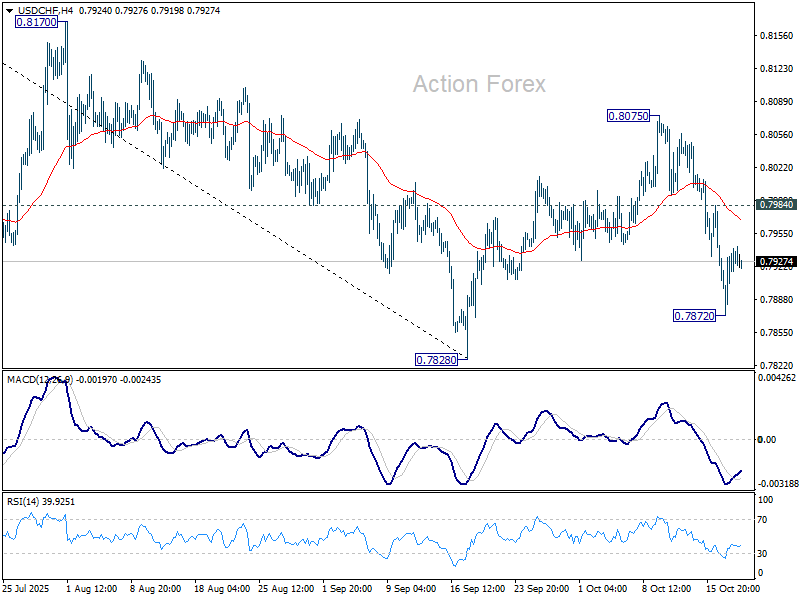

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7893; (P) 0.7916; (R1) 0.7958; More…

Range trading continues in USD/CHF and intraday bias stays neutral. Further decline is expected as long as 0.7984 resistance holds. On the downside, below 0.7872 will bring retest of 0.7828. Firm break there will resume larger down trend. However, break of 0.7984 will suggest that corrective pattern from 0.7828 is extending with another rising leg, and target 0.8075 again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).