Stronger Canada CPI Narrows Odds of Back-to-Back BoC Easing – Action Forex

Canadian Dollar climbed across the board as markets enter into U.S. session, leading major currencies higher after domestic inflation data came in hotter than expected. Combined with this month’s firm employment figures, the data have made the case for a rate cut at the October 29 meeting a close call.

While the BoC maintain an easing bias and markets still expect more cuts ahead, the latest figures may prompt the BoC to pause this month and reserve ammunition for December, especially with signs that the domestic economy remains more resilient than feared.

Meanwhile, Yen stayed under sustained selling pressure. In a landmark parliamentary vote, Sanae Takaichi, leader of the ruling Liberal Democratic Party, was formally elected as Japan’s first female prime minister. The LDP’s new coalition partner, the Japan Innovation Party, helped deliver a comfortable win as opposition parties failed to field a unified challenger.

Takaichi swiftly unveiled her new Cabinet, naming Ryosei Akazawa, Japan’s chief tariff negotiator with the U.S., as trade minister to maintain momentum in bilateral talks. The new administration faces an immediate diplomatic challenge — the upcoming visit by U.S. President Donald Trump, which will test Japan’s approach to the ongoing tariff discussions and its broader defense cooperation with Washington.

Trade tensions between the U.S. and China remain another focal point. Chinese customs data showed rare earth magnet exports to the U.S. fell -28.7% mom in September to 420.5 tonnes — nearly 30% below last year’s levels. Reports suggest China tightened licensing procedures for rare earth exports in September, ahead of a broader regulatory expansion implemented in October. The move underscores Beijing’s intention to use resource controls as leverage in trade disputes, while Washington continues to forge strategic mineral alliances with partners such as Australia.

In currency markets, Loonie stands out as the day’s top performer, followed by Dollar and Sterling. Yen remains the weakest, trailed by the Swiss franc and Kiwi. Aussie and Euro trade in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.31%. DAX is up 0.17%. CAC is up 0.44%. UK 10-year yield is down -0.022 at 4.492. Germany 10-year yield is down -0.007 at 2.573. Earlier in Asia, Nikkei rose 0.27%. Hong Kong HSI rose 0.65%. China Shanghai SSE rose 1.36%. Singapore Strait Times rose 1.20%. Japan 10-year JGB yield fell -0.006 to 1.663.

Canada CPI surges to 2.4% in September, core measures accelerate too

Canada’s consumer prices accelerated more than expected in September. Headline CPI rose 2.4% yoy, up sharply from 1.9% in August and above consensus of 2.3%. The rebound was largely driven by a smaller year-ago decline in gasoline prices — down -4.1% compared with -12.7% in August — which created a notable base effect in the annual calculation.

Even so, underlying inflation momentum also firmed. Excluding gasoline, CPI rose 2.6% yoy, up from 2.4% in the previous month, signaling broader price pressures beyond energy. All three core inflation measures came in hotter than anticipated. CPI median held steady at 3.2%, beating expectations of 3.0%. CPI trimmed ticked up from 3.0% to 3.1%. CPI common accelerated from 2.5% yoy to 2.7%.

New Zealand trade deficit widens NZD -14B despite strong 19% export growth

New Zealand recorded another sizeable trade deficit in September 2025, as import growth outstripped exports despite solid overseas demand. Statistics NZ data showed goods exports rose 19% yoy to NZD 5.8B. Imports increased 1.6% yoy to NZD 7.2B. The result was a monthly deficit of NZD -1.4B, versus expectation of NZD -6B and prior month’s NZD -1.2B.

Export strength was broad-based, led by double-digit gains to all major partners. Shipments to China jumped 24% yoy, Australia 28%, and Japan 23%, while sales to the U.S. and EU rose 10% and 15%, respectively.

On the import side, purchases from China climbed 16% yoy, while inflows from the EU and Australia rose 7.3% and 6.4%. Offsetting that, imports from the U.S. slumped -30%, and South Korea fell -4.8%.

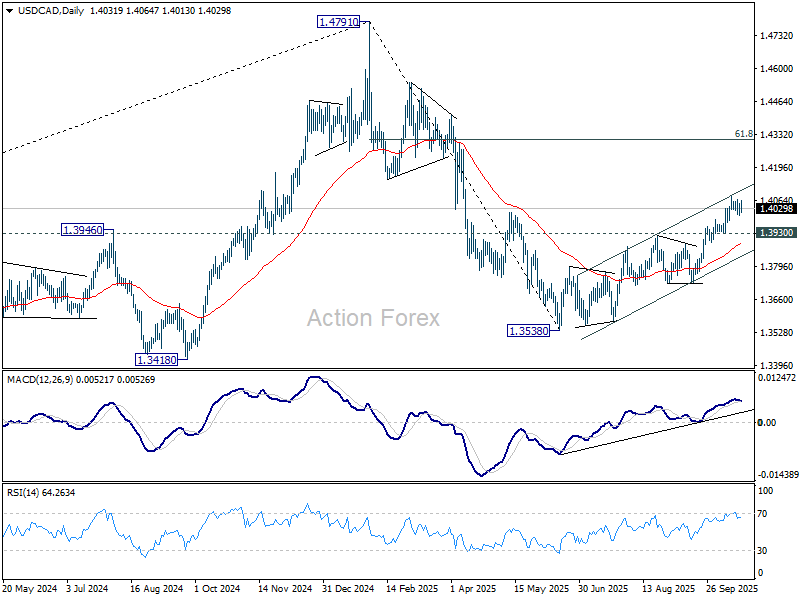

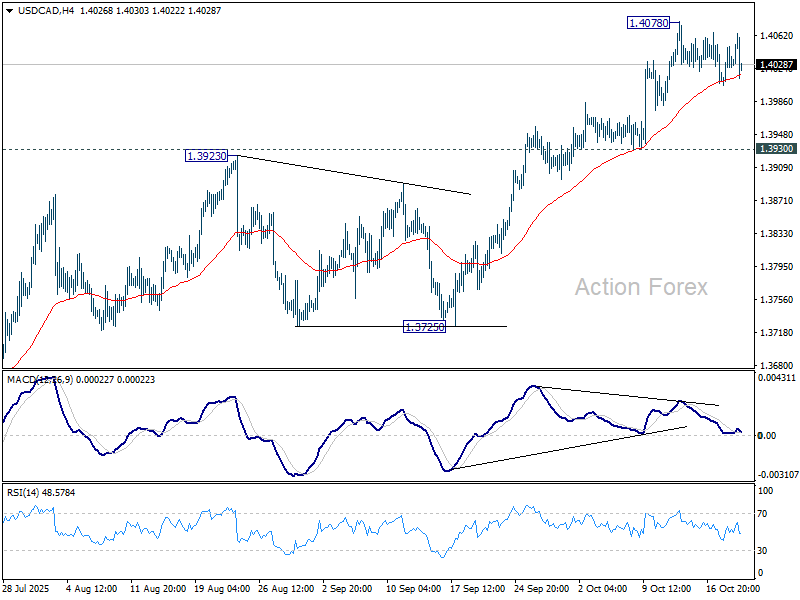

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4014; (P) 1.4032; (R1) 1.4059; More…

USD/CAD dips mildly in early US session, but stays well above 1.3930. Intraday bias remains neutral for more consolidations below 1.4078. But further rally is still expected as long as 1.3930 support holds. Current development suggest that rise from 1.3538 is reversing whole fall from 1.4791. Above 1.4078 will target 61.8% retracement of 1.4791 to 1.3538 at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds.