Geopolitics Back in Play as Oil Surges on Fresh Sanctions Against Russia – Action Forex

Oil prices surged today, emerging as the clear focus in otherwise subdued global markets, as geopolitical tensions flared again following a fresh wave of Western sanctions against Russia. The U.S. announced new measures targeting energy giants Rosneft and Lukoil, accusing Moscow of prolonging the conflict in Ukraine. The decision reignited fears of tighter global supply, prompting a strong rebound in crude prices.

Together, Rosneft and Lukoil account for nearly half of Russia’s crude exports, which exceed four million barrels per day. The sanctions effectively restrict these companies from accessing Western financial channels and trading networks, raising questions about how quickly buyers can adapt. The move could trigger short-term disruptions in global flows, particularly given the heavy reliance of Asian refiners in China and India on Russian crude.

In practical terms, the sanctions will force Chinese and Indian refineries to seek alternative suppliers to avoid secondary penalties and maintain access to international banking systems. Both countries could pivot more heavily toward U.S. and OPEC producers, which still have spare capacity to fill part of the gap — particularly Saudi Arabia. However, the redirection of demand toward non-sanctioned barrels will likely drive broader upward pressure on global oil prices.

The U.S. action follows the U.K.’s sanctions last week on the same Russian firms, underscoring a coordinated Western push to tighten the noose on Russia’s energy sector. Meanwhile, the European Union approved its 19th sanctions package, which includes a ban on Russian LNG imports and potentially a new plan to use frozen Russian assets to fund Ukraine over the next two years. The measures mark a further escalation of economic pressure just as Western leaders seek to reaffirm long-term support for Kyiv.

In currency markets, performance diverged along familiar lines. Aussie leads gains for the week so far, followed by Kiwi and Loonie. In contrast, Yen extended its slide, while Swiss Franc and Euro also weakened. Sterling and Dollar traded in the middle.

Canada retail sales rise 1.0% mom in August, but early data point to September dip

Canada’s retail sales grew 1.0% mom in August to CAD 70.4B, in line with market expectations, driven largely by strength in motor vehicle and parts dealers. Gains were recorded in six of nine subsectors, underscoring still-solid consumer activity despite higher borrowing costs.

Excluding volatile components such as autos and fuel, core retail sales rose an even stronger 1.1% mom, suggesting a firm base of household spending momentum through late summer.

However, the outlook for the following month looks weaker. Statistics Canada’s advance estimate pointed to a -0.7% mom decline in September sales, hinting at some loss of momentum heading into the fourth quarter.

SNB minutes: Price stability intact, no threat of lasting deflation

The SNB reaffirmed its accommodative stance in the summary of its September policy meeting, noting that inflation is expected to remain comfortably within the range consistent with price stability. The Governing Board discussed the outlook in detail with experts, concluding that “all available information points to inflation remaining within the range consistent with price stability” and that it is “not expected to become persistently negative.”

While price pressures remain subdued, policymakers highlighted a rising degree of external uncertainty, particularly stemming from U.S. trade policy. The SNB warned particularly that tariffs on pharmaceutical products — one of Switzerland’s key export sectors — could weigh on GDP in both the short and medium term. The extent of the drag, however, remains uncertain and will depend on how global supply chains and exchange rates evolve. Large currency swings were cited as a key risk factor for the inflation outlook.

The Governing Board noted that monetary policy remains “expansionary”, with the full effects of previous easing still filtering through the economy. Despite weak inflationary pressure and a modest deterioration in the growth outlook, policymakers believe the current stance is supporting a gradual rise in prices and providing essential backing for domestic activity.

Given this backdrop, the SNB concluded that “a further easing of monetary policy was not appropriate.” The conditional inflation forecast and the overall growth assessment justify holding rates steady, and the policy rate was left unchanged at 0%.

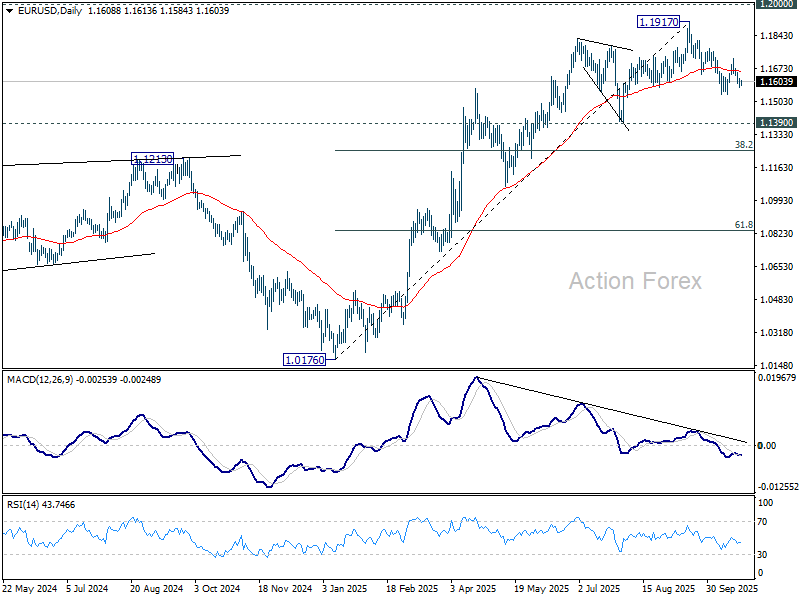

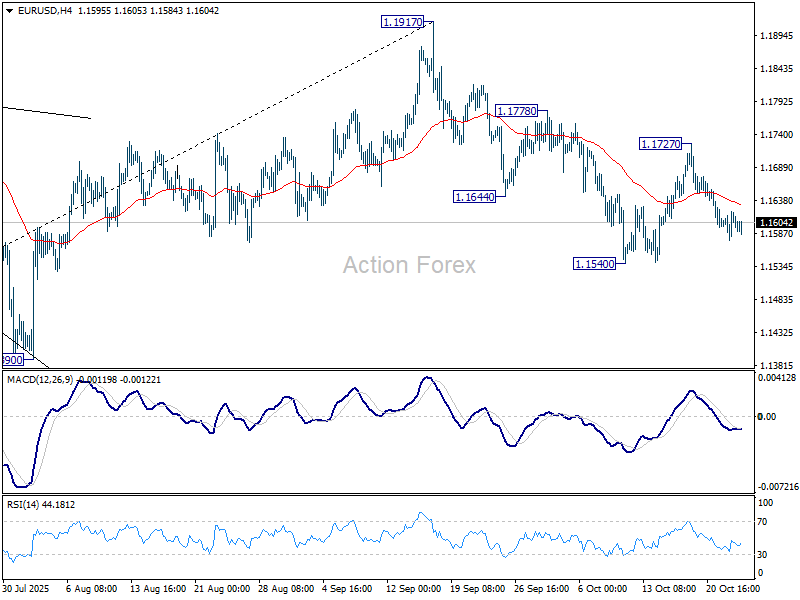

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1584; (P) 1.1603; (R1) 1.1629; More…

Outlook in EUR/USD is unchanged. Intraday bias stays neutral, and further decline is expected with 1.1727 resistance intact. Break of 1.1540 will resume the fall from 1.1917 to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1290) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.