Global Risk Rally Reignites as US, UK, and Japan Hit All-Time Highs – Action Forex

Global markets resumed their risk-on momentum last week, buoyed by softer U.S. inflation data, easing political uncertainty, and renewed optimism over global trade. In the U.S., both DOW and S&P 500 climbed to fresh record highs after September CPI figures came in below expectations, cementing confidence that the Fed remains on track to deliver two more rate cuts by year-end. Sentiment was also underpinned by progress on the U.S.–China trade front, as high-level officials met in Malaysia to lay the groundwork for a Trump–Xi summit. Markets welcomed the prospect of de-escalation that could avert the next wave of tariffs in November.

In Europe, downside surprise in UK inflation further boosted risk appetite by reinforcing expectations that the BoE will continue its easing cycle. Combined with firmer oil prices and robust corporate earnings, FTSE 100 surged to a new record high. Meanwhile in Asia, Japan’s political clarity provided another lift to sentiment. The election of Sanae Takaichi as Japan’s first female prime minister removed a major source of uncertainty and drove the Nikkei to new all-time highs.

In currency markets, commodity-linked currencies led the way — with Kiwi, Aussie and Loonie as the top performers — reflecting a renewed global appetite for risk. Yen, by contrast, weakened sharply, while Sterling and Swiss Franc also softened. Dollar and Euro finished the week in middle positions.

CPI Miss Locks in Fed Cuts, DOW Extends Record-Breaking Rally

The U.S. inflation report for September was the most consequential data point of the week. Headline CPI ticked up from 2.9% to 3.0%, slightly below market expectations of 3.1%. Core CPI eased from 3.1% to 3.0%, its first slowdown since spring. For the Fed, some officials had long argued that while tariffs may keep inflation sticky in the short term, they would not cause an uncontrolled spike. The data supported that narrative

Also, the softer core reading offered a degree of reassurance to both policymakers and investors that underlying price pressures are no longer reaccelerating. The uptrend in core inflation that began in May has possibly peaked. Fed’s policy focus can shift more comfortably toward supporting growth and managing downside risks.

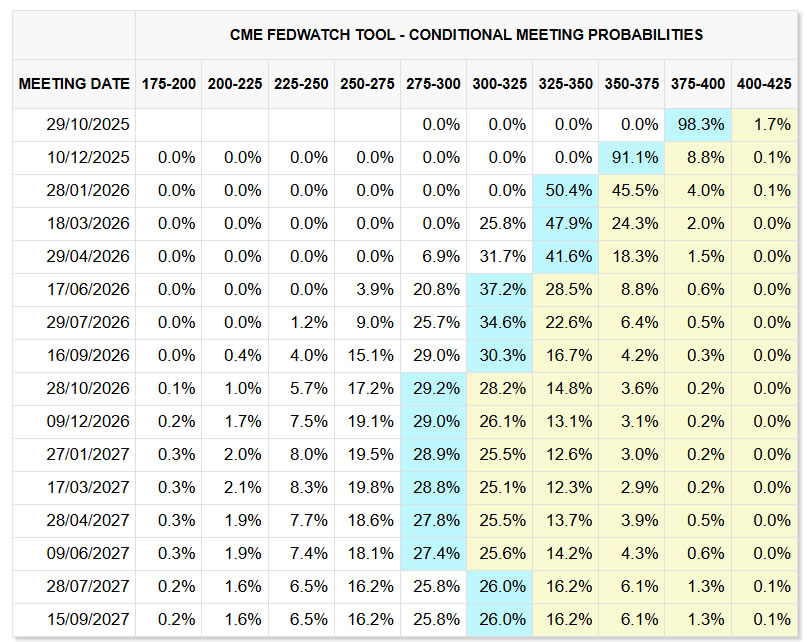

Fed fund futures now price in nearly a 100% probability of a 25bps rate cut at Wednesday’s FOMC meeting, which would bring the policy rate down to the 3.75–4.00% range. Expectations of another 25bps move in December have also solidified, with traders assigning more than 90% likelihood. The market now envisions the easing cycle extending into 2026, with three more cuts anticipated to lower rates toward 2.75–3.00% by late 2026 or early 2027.

Technically, DOW remains comfortably within its near term ascending channel, and well supported by the rising 55 D EMA (now at 45,799). Friday’s decisive advance confirmed that the rally from 36,611 has resumed, targeting 61.8% projection of 36,611 to 44,885 from 43,340 at 48,454. The index could encounter some initial resistance near that level, which is close to the channel top. Even if short-term retreat occurs, outlook will stay as long as 55 D EMA holds firm.

10-Yields Trying to Stabilize Near 4%, Dollar Index Lacks momentum

U.S. 10-year yield briefly dipped to 3.947 but stabilized from there. Technically, the yield’s downward momentum has started to flatten, as indicated by D MACD, suggesting that the selling pressure seen through late September is losing force.

Further decline remains possible in the near term, but firm support zone near 61.8% projection of 4.493 to 3.992 from 4.200 at 3.891 should contain the downside on the first test. If yields hold above that level and break back above 4.05, that would signal short-term bottoming, paving the way for rebound toward 55 D EMA (now at 4.129).

From a macro perspective, the next move in yields will serve as a litmus test for broader market confidence. With the absence of renewed stress in regional banks or credit markets like the prior week, 3.9% could emerge as a durable floor for the benchmark yield.

Meanwhile, Dollar Index rebounded after drawing support from 55 D EMA (now at 98.35), but upside momentum proved unconvincing. Dollar’s rally attempts were capped by by falling yields and broad risk-on sentiments.

Overall outlook is unchanged that rebound from 96.21 is tentatively viewed as a corrective move. Break above 99.56 would extend the recovery toward 100.25 resistance. But upside should be capped near the 38.2% retracement of 110.17 to 96.21 at 101.54.

Failure to hold 97.46 support, however, would signal that the corrective phase has ended prematurely, setting up a retest of 96.21 low.

FTSE Hits Record High, EUR/GBP Bounces from 55 D EMA

The latest UK inflation report revived hope that the BoE will continue easing later this year. Headline inflation held steady at 3.8%, defying expectations for an uptick to 4.0%, while core CPI slipped to 3.5% from 3.6%. The expectations sent FTSE to new record high and kept Sterling pressured.

However, a move at the November meeting still appears premature. BoE officials are expected to hold fire until after the government’s November 26 Budget, which could significantly influence the inflation and growth outlook. Chancellor Rachel Reeves reaffirmed last week that there would be “targeted action in the Budget around prices” to lower the cost of living, adding that she wants to see interest rates — already reduced five times in the past year — “come down further.” Against that backdrop, December remains the most likely timing for the next cut, with markets now pricing an 80% chance of a 25bps reduction to 3.75%.

Technically, FTSE’s up trend remains on track to 61.8% projection of 8,707.65 to 9,577.08 from 9,354.54 at 9,814.22. That level could act as interim resistance for the near term. There would be scope to challenge 100% projection at 10,146.34, if the Budget confirms a supportive fiscal tone. In any case, outlook will stay bullish as long as 55 D EMA (now at 9,305.33) holds.

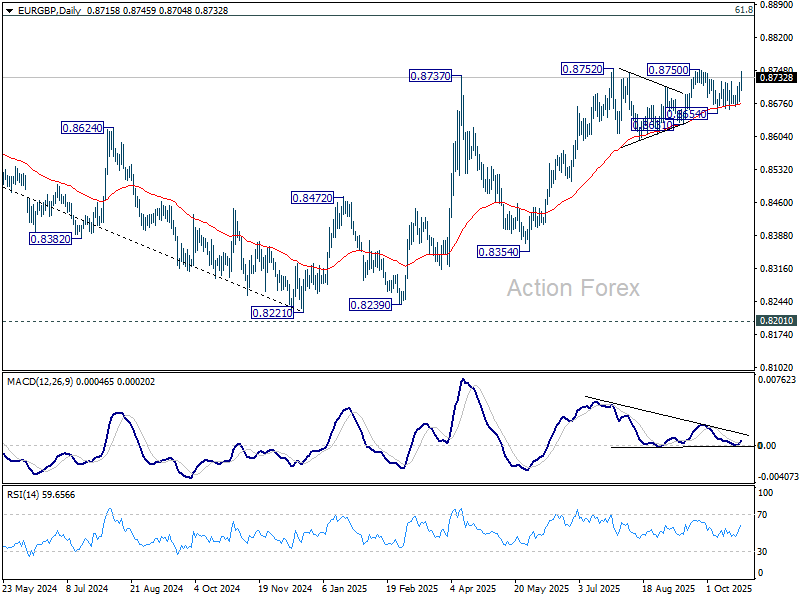

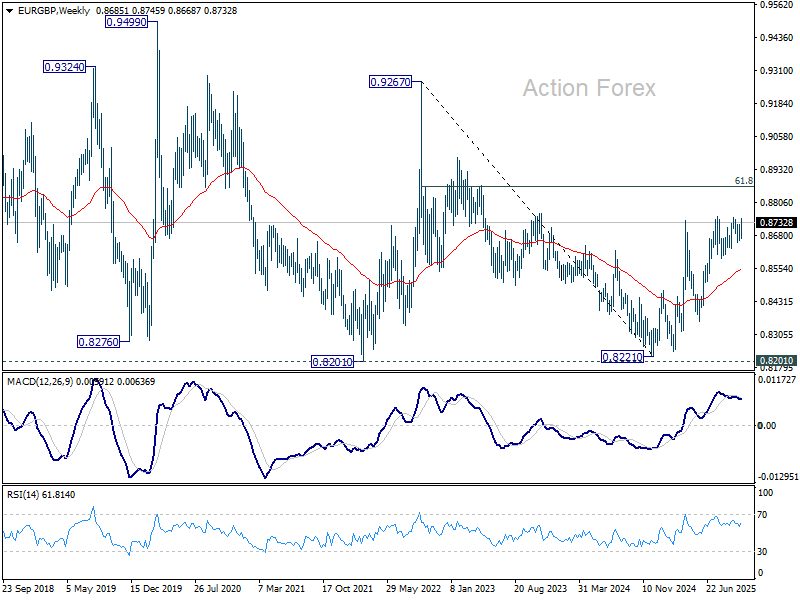

In the currency markets, EUR/GBP is showing renewed strength. Fundamentally, the cross is structurally supported by the policy divergence between the ECB and BoE — with the former firmly maintaining a hold stance and the latter leaning toward further easing.

Technically, EUR/GBP was repeatedly supported by 55 D EMA (now at 0.8676). Pullback from 0.8750 may have already run its course. Firm break above 0.8750 would signal resumption of the rise from 0.8221, with the next target 61.8% retracement of 0.9267 to 0.8221 at 0.8867.

This 0.8867 level will be a key hurdle to test the underlying momentum of EUR/GBP. For now, considering bearish divergence condition in D MACD, it will more likely cap upside than not.

Nikkei Eyes 50k as Takaichi Era Begins; NZD/JPY Jumps on Yen Weakness

Japanese markets extended their strong run last week, with Nikkei 225 hitting a new record high before easing slightly below the psychological 50,000 mark. The rally came as political uncertainty faded after Sanae Takaichi formally secured her premiership, becoming Japan’s first female prime minister. Backed by a newly formed coalition between the Liberal Democratic Party and the Japan Innovation Party, Takaichi’s leadership has been broadly welcomed by investors anticipating continuity in pro-growth and pro-stimulus policies.

Despite minor profit-taking into the weekend, the overall tone in Tokyo remains upbeat. The shallow pullback from the 50,000 level did not trigger the kind of “sell-the-news” response some had feared. Also, the global risk-on environment would be a powerful tailwind for Japanese equities.

Another take on 50,000 market is likely in the near term. Though, whether Nikkei could sustain above 50,000 would very much depend on how Takaichi performs during her first 100 days in office.

Technically, near term outlook will stay bullish as long as 46,544.05 support holds. Sustained trading above 50,000 will extend the up trend to 138.2% projection of 25,661.89 to 42,426.77 from 30,792.74 at 43,961.80 in the medium term.

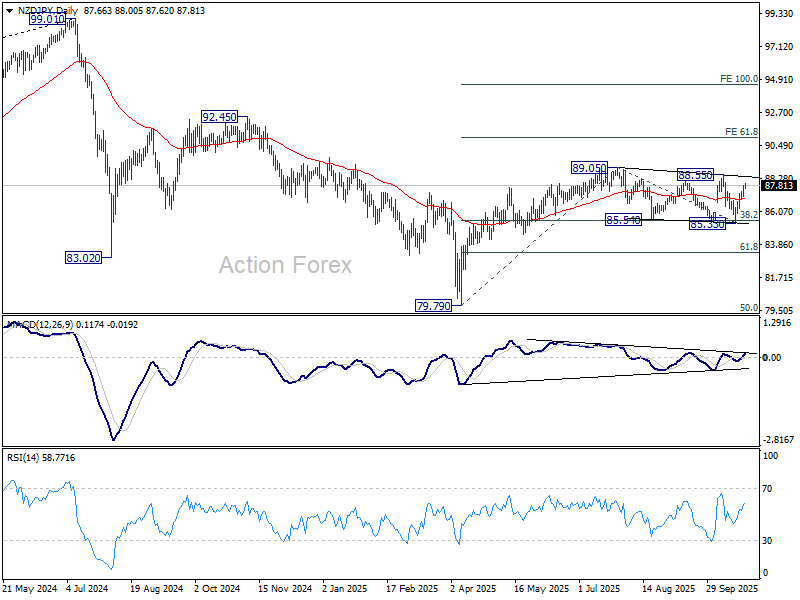

Meanwhile, Yen continues to underperform, with NZD/JPY ended as the top mover, registering 1.89% gain. Technically, for NZD/JPY, repeated support from 38.2% retracement of 79.79 to 89.05 at 85.51 keeps the rise from 79.79 intact. Indeed, it’s possible that the corrective pattern from 89.05 has already completed with three waves to 85.33.

Near term focus will now be on 88.55 resistance. Firm break there will bolster the bullish case that rise from 79.79 is resuming. Further break of 89.05 will confirm and target 61.8% projection of 79.79 to 89.05 from 85.33 at 91.05 next.

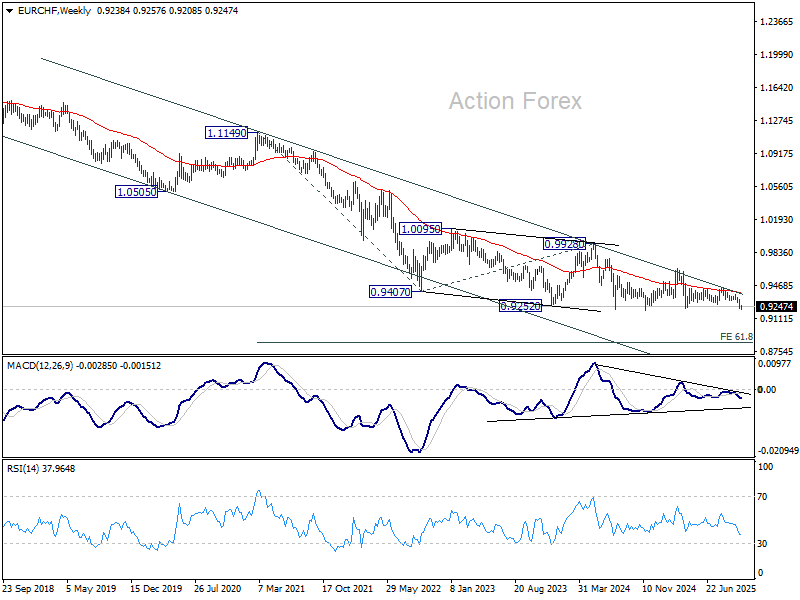

EUR/CHF Weekly Outlook

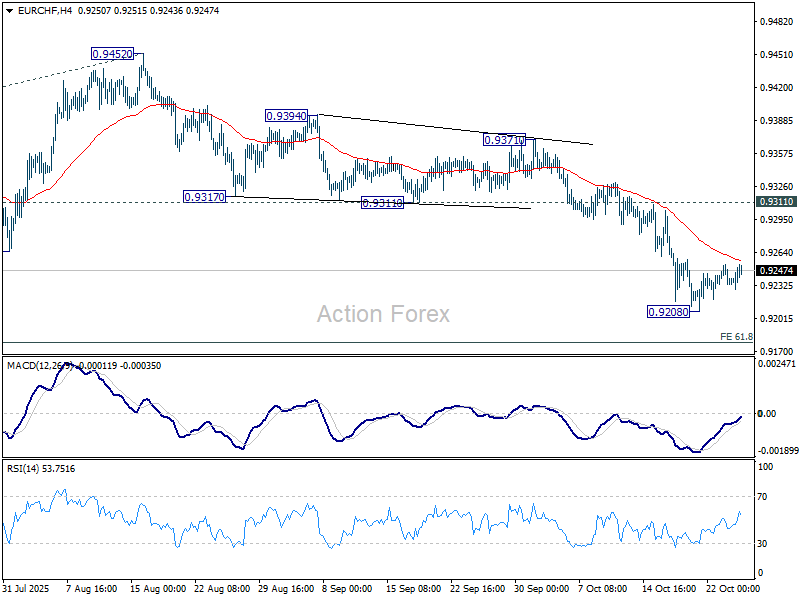

EUR/CHF edged lower last week but recovered ahead of 0.9204 support. Initial bias remains neutral this week first, and some more consolidations could be seen. But upside should be limited below 0.9311 support turned resistance. On the downside, break of 0.9204 will confirm larger down trend resumption. Next target is 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179. Firm break there will target 100% projection at 0.9010.

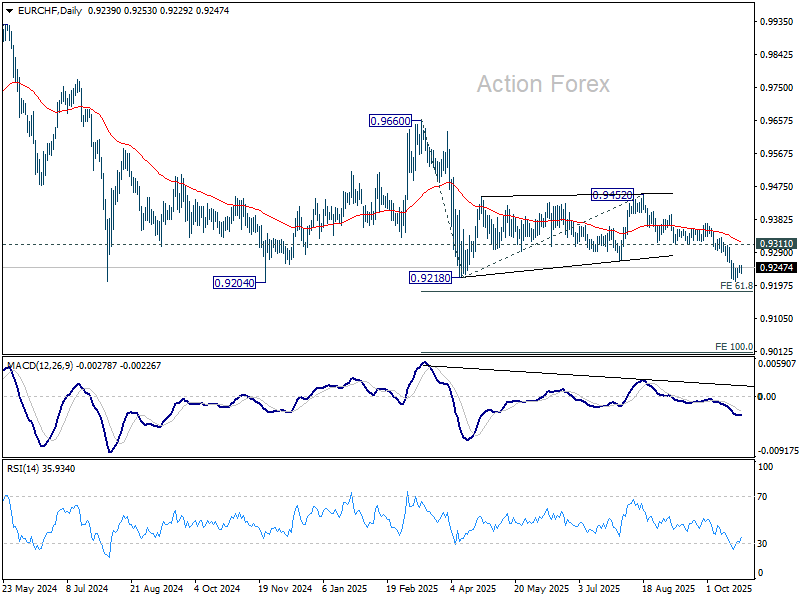

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9395). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming.

In the long term picture, overall long term down trend is still in progress in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9820) holds.