Markets Hold Breath Ahead of US CPI, US–China Talks in KL – Action Forex

Dollar traded steady in Asian session, with traders showing little appetite for new positions ahead of key inflation data. The September CPI report, due later in the day, is expected to show a 0.4% monthly increase in headline prices and a 0.3% gain in core CPI, which would push the annual headline rate up to 3.1% while leaving core steady at 3.1%.

While the CPI outcome is unlikely to derail the Fed’s plan to ease this month, it could help determine the pace of cuts going forward. Markets are currently assigning more than 90% probability to another reduction in December. A hotter print could raise the chance of delaying the next move. Beyond Fed implications, the CPI release is also seen as a volatility trigger for broader markets that have drifted without clear direction.

On the trade front, U.S.–Canada trade relations took a sudden turn after US President Donald Trump declared all negotiations with Ottawa “terminated,” citing a “fraudulent” advertisement featuring Ronald Reagan criticizing tariffs. The Ronald Reagan Presidential Foundation later said the ad used “selective audio and video,” adding that it was reviewing legal options. Canadian Prime Minister Mark Carney on the other hand, vowed not to grant “unfair access” to U.S. markets if ongoing trade discussions collapse.

At the same time, attention is shifting to Kuala Lumpur, where senior officials from the U.S. and China are set to meet on Friday to defuse trade tensions. Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer will hold talks with Chinese Vice Premier He Lifeng to prevent a further escalation ahead of next week’s planned Trump–Xi summit. The talks are crucial to averting a new wave of 100% tariffs on Chinese goods, set to take effect on November 1, in retaliation for Beijing’s expanded export controls on critical rare earth materials.

Overall for the week so far, commodity currencies are generally strong, with Kiwi leading, followed by Aussie and Loonie. Yen is pinned at the bottom, followed by Sterling and Euro. Swiss Franc and Sterling are trading mid-pack.

In Asia, at the time of writing, Nikkei is up 1.33%. Hong Kong HSI is up 0.47%. China Shanghai SSE is up 0.45%. Singapore Strait Times is up 0.23%. Japan 10-year JGB yield is down -0.01 at 1.651. Overnight, DOW rose 0.31%. S&P 500 rose 0.58%. NASDAQ rose 0.89%. 10-year yield rose 0.038 to 3.991.

Japan CPI core Rises to 2.9%, ending three-month slowdown

Japan’s inflation picked up in September, with core CPI (excluding fresh food) rising from 2.7% to 2.9% yoy, matching expectations and marking the first acceleration in four months. The key gauge has stayed at or above the BoJ’s 2% target since April 2022. Headline CPI also rose from 2.7% to 2.9% yoy, in line with the core measure.

Underlying momentum was uneven. Core-core CPI, which strips out both energy and fresh food and is considered a closer measure of domestic demand, slowed to 3.0% from 3.3% yoy, suggesting that broader inflationary pressures are gradually easing.

Food prices continued to rise, but at a slower pace — non-fresh food prices gained 7.6%, down from 8.0% in August. Rice prices, which spiked earlier this year, rose 49.2%, their fourth consecutive month of deceleration after peaking at more than 100% growth in May.

Meanwhile, service prices, a metric closely watched by the BoJ for its link to wage growth, increased 1.4%, slightly below August’s 1.5%.

Japan PMI composite falls to 50.9, weak Yen keeps inflation hot

Japan’s private sector lost further momentum in October, with both manufacturing and services activity softening, according to S&P Global’s Flash PMI survey. The Manufacturing PMI slipped from 48.5 to 48.3, extending its contraction, while Services PMI fell from 53.3 to 52.4. As a result, Composite index eased from 51.3 to 50.9, signaling the slowest pace of overall growth since May.

Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, said the survey showed the first decline in new business in 16 months. While the services sector remained the key driver of growth, its fading strength “will be a point of concern” as manufacturing continues to struggle. The factory sector’s downturn deepened, with new orders falling at the fastest pace in 20 months.

Inflationary pressures, however, remained elevated. Both input costs and output charges continued to rise at historically strong rates, driven by higher wage, fuel, and material costs, and alongside by a weaker Yen.

Australia PMI composite ticks up to 52.6, easing inflation keeps RBA on easing track

Australia’s private sector activity sent mixed signals in October, according to the S&P Global Flash PMI survey. Manufacturing PMI slipped back into contraction, falling from 51.4 to 49.7, while Services PMI rose to 53.1 from 52.4, lifting the Composite PMI modestly from 52.4 to 52.6. The data suggest that overall business activity grew at a slightly faster pace at the start of Q4, though the underlying picture remains uneven across sectors.

According to Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, the divergence between sectors was striking. Manufacturing “notably worsened,” with new orders dropping further and factories shedding jobs amid pressure on profit margins.

In contrast, services activity expanded at a solid pace, but even there, new business growth and hiring momentum slowed, and business confidence weakened.

On a positive note, price pressures continued to ease, with output price inflation falling to a five-year low. This cooling in inflation dynamics should reassure the RBA, which remains on track to pursue further monetary easing.

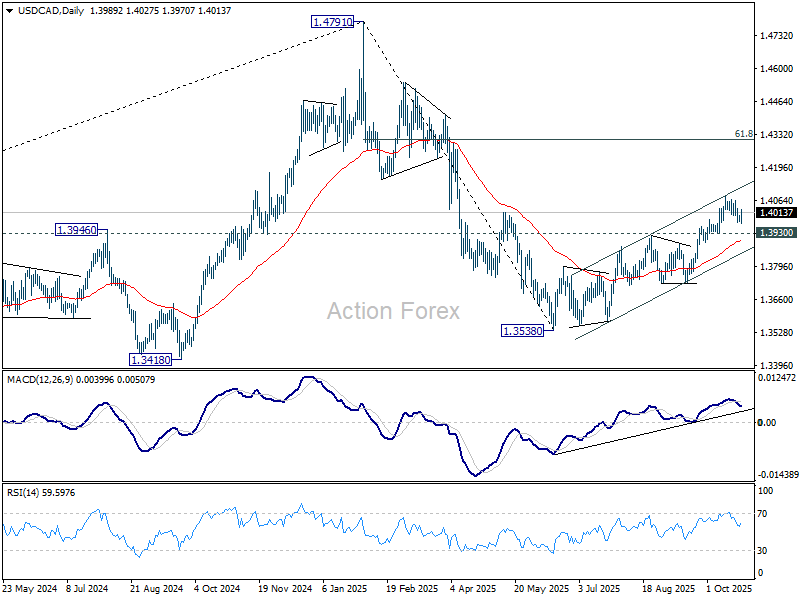

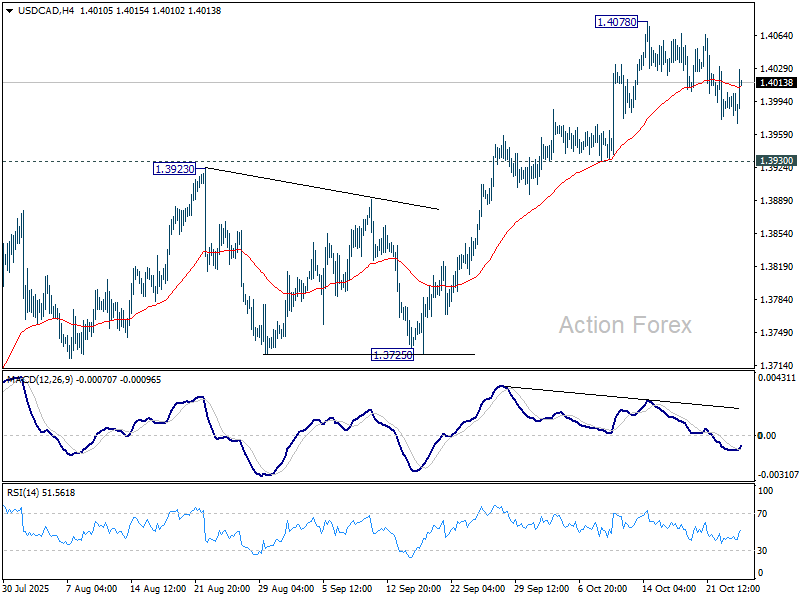

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3981; (P) 1.3993; (R1) 1.4006; More…

USD/CAD is still extending the corrective pattern from 1.4078. Intraday bias stays neutral for the moment. While deeper retreat cannot be ruled out, further rally is still expected as long as 1.3930 support holds. Current development suggest that rise from 1.3538 is reversing whole fall from 1.4791. Above 1.4078 will target 61.8% retracement of 1.4791 to 1.3538 at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds.