Sterling Sinks on UK Fiscal Shock; Aussie Steady Ahead of CPI – Action Forex

Sterling tumbled sharply today, hitting its lowest level against Euro in nearly a year as renewed fiscal concerns dominated sentiment. The selloff followed reports from the Financial Times that UK Chancellor Rachel Reeves will face a deeper-than-expected deterioration in the UK’s public finances, delivering an early setback ahead of next month’s crucial Budget.

According to the report, the Office for Budget Responsibility is preparing to slash its long-term productivity growth forecast by 0.3 percentage points, a more severe downgrade than markets had anticipated. The revision reflects persistent weakness in productivity growth since the 2008 financial crisis and would force the Treasury to account for roughly GBP 20–21B in additional borrowing by 2029–30.

The Institute for Fiscal Studies, which provided the underlying calculations cited by the Financial Times, noted that each 0.1-point reduction in productivity growth adds roughly GBP 7B to public borrowing. Markets had previously expected a smaller downgrade of between 0.1 and 0.2 points, implying a fiscal hit closer to GBP 7–14B. The larger revision leaves Chancellor Reeves with far less room for maneuver .

Elsewhere, Aussie traded mixed as risk sentiment cooled ahead of the highly anticipated Q3 CPI report due in the next Asian session. Economists expect headline inflation to rise 1.1% qoq, lifting the annual rate to 3.0% yoy from 2.1%. The trimmed mean CPI—the RBA’s preferred core measure—is forecast to rise 0.8% qoq, keeping the yearly rate steady at 2.7% yoy.

RBA Governor Michele Bullock signaled this week that an upside surprise in core inflation could be a “material miss.” She warned that a 0.9% quarterly increase—just 0.3 percentage points above the RBA’s own forecast—would raise concerns about inflation persistence. Her comments dampened market expectations for near-term rate cuts.

Money markets now assign just a 40% probability of a 25bps cut in November, down sharply from near 60% before Bullock’s remarks and over 80% a week ago. The CPI data will therefore be pivotal in shaping the RBA’s near-term guidance and the path of Australian Dollar into year-end.

In the broader currency space, Aussie remains the week’s top performer, followed by Yen and Kiwi. Sterling sits at the bottom. Dollar and Loonie also trade soft, while Euro and Swiss Franc hold mid-range. The configuration underscores a market leaning toward risk neutrality — cautious on Sterling, patient on the RBA, and positioning ahead of key macro catalysts later in the week.

In Europe, at the time of writing, FTSE is up 0.20%. DAX is down -0.04%. CAC is down -0.07%. UK 10-year yield is down -0.011 at 4.394. Germany 10-year yield is flat at 2.620. Earlier in Asia, Nikkei fell -0.58%. Hong Kong HSI fell -0.33%. China Shanghai SSE fell -0.22%. Singapore Strait Times rose 0.23%. Japan 10-year JGB yield fell -0.035 to 1.640.

ECB survey shows inflation expectations edge lower to 2.7%

The ECB’s September Consumer Expectations Survey showed a modest easing in near-term inflation expectations, with the median outlook for the next 12 months slipping to 2.7% from 2.8%.

Expectations for three years ahead were unchanged at 2.5%, while five-year projections held steady at 2.2%, suggesting longer-term views remain well anchored. Uncertainty around the 12-month outlook also stayed unchanged, indicating little shift in household sentiment.

On the growth side, consumers’ expectations for economic performance over the next year remained negative but stable, holding at –1.2%. The data continue to reflect subdued confidence in the near-term recover.

Unemployment expectations were similarly steady at 10.7% for the 12-month horizon, signaling limited change in labor-market sentiment.

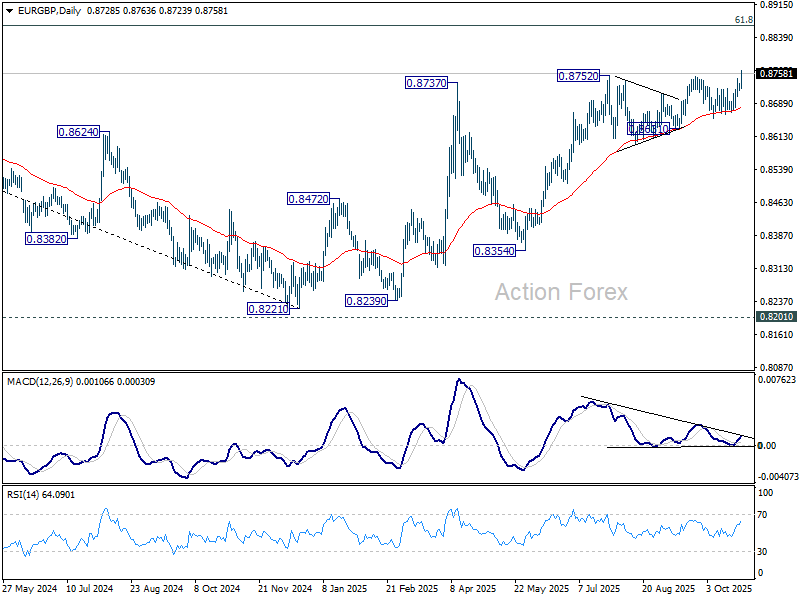

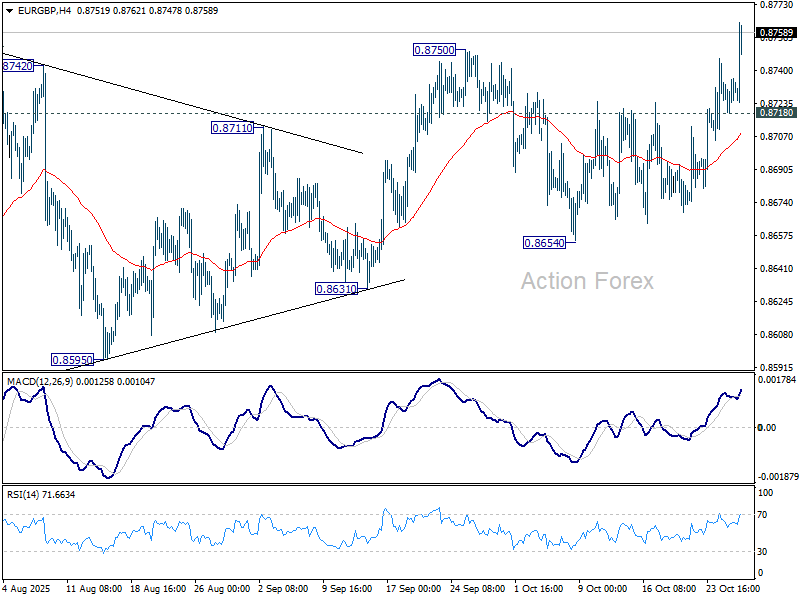

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8729; (R1) 0.8738; More…

EUR/GBP’s break of 0.8750 resistance confirms resumption of whole rally from 0.8221. Intraday bias is back on the upside for 0.8867 fibonacci level. On the downside, below 0.8718 minor support will turn intraday bias neutral again first. But near term outlook will now stay bullish as long as 0.8654 support holds, in case of retreat.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8654 support will be the first sign that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high).