Canadian Dollar Jumps as BoC Declares Policy ‘About Right’ After Cut – Action Forex

Canadian Dollar climbed after the BoC lowered its overnight rate to 2.25% and signaled that policy is likely now at its terminal level. The bank’s statement that rates are “about the right level” if the outlook unfolds as expected was interpreted as a clear end-of-cycle message. The message was subtle but decisive: the bar for additional easing is now much higher.

That stance gave the Loonie a lift, even as the currency’s gains were eclipsed by Aussie, which remains the day’s star performer. Stronger-than-expected CPI report earlier today led some analysts to abandon expectations of further RBA cuts, while some analysts now speculate that the next policy move could even be upward if price pressures persist. Kiwi also joined the rally, supported by robust risk appetite.

At the weaker end, Sterling extended its sell-off amid lingering fiscal concerns tied to next month’s budget and a deteriorating U.K. fiscal outlook. The Swiss Franc and Euro also traded lower. Dollar and Yen were positioned mid-range ahead of Fed decision.

Attention now turns to the Fed, which is widely expected to cut rates by 25 bps to 3.75–4.00%. Futures continue to price in about a 90% chance of another cut in December, meaning that unless Fed Chair Jerome Powell explicitly pushes back, markets are unlikely to adjust much. Opinions on the 2026 policy path remain highly divided, not least because of uncertainty surrounding Powell’s successor. Until a decision is made and fresh data are available, markets are unlikely to get a clear picture of where rates may stand in 2026.

On the trade front, US President Donald Trump told business leaders at the APEC Summit he was confident of striking a “good deal” with President Xi Jinping at their Thursday meeting—the first since Trump’s second-term tariff offensive began. Officials say the deal could include deferring China’s export controls on rare earth minerals and scrapping the planned 100% U.S. tariff on Chinese goods, as well as renewed agricultural purchases. That optimism has helped propel U.S. indexes to record highs this week, a rally that now depends on both leaders delivering on expectations.

In Europe, at the time of writing, FTSE is up 0.64%. DAX is down -0.27%. CAC is down -0.30%. UK 10-year yield is down -0.01 at 4.395. Earlier in Asia, Nikkei rose 2.17%. Hong Kong was on holiday. China Shanghai SSE rose 0.70%. Singapore Strait Times fell -0.23%. Japan 10-year JGB yield rose 0.015 to 1.654.

BoC cuts to 2.25%, signals end of easing Cycle

BoC delivered a widely expected 25bps rate cut, lowering its overnight rate to 2.25%, but signaled that this could mark the end of its current easing cycle. The central bank said that if inflation and economic activity evolve in line with its October projection, the current policy rate is “about the right level” to balance supporting growth with keeping inflation close to target. That phrasing was interpreted as indicating that 2.25% is the likely terminal rate, barring major economic shocks.

In its accompanying statement, the BoC acknowledged that U.S. trade actions and uncertainty are having “severe effects” on key export-oriented industries. As a result, the Bank expects GDP growth to remain weak in the second half of the year before recovering gradually through 2026. The economy is projected to expand 1.2% in 2025, 1.1% in 2026, and 1.6% in 2027, with excess capacity expected to be absorbed only slowly.

The BoC described the labour market as soft, with job declines concentrated in trade-sensitive sectors, while hiring across the broader economy remains subdued.

On inflation, the BoC noted that headline CPI stood at 2.4% in September, slightly above expectations, while its preferred core measures remain sticky around 3%. Broader alternative indicators suggest underlying inflation near 2.5%, but the BoC expects price pressures to ease gradually and headline CPI to remain close to 2% over the projection horizon.

Australia inflation shock: CPI surges to 3.2%, core re-accelerates

Australia’s inflation surprised sharply to the upside in Q3, reigniting concerns that price pressures are proving stickier than expected. Headline CPI jumped 1.3% qoq, accelerating from 0.7% in Q2 and beating expectations of 1.1% — marking the strongest quarterly increase since Q1 2023. The Australian Bureau of Statistics said the largest contributor was a 9.0% rise in electricity costs, which alone drove much of the headline surge.

On an annual basis, CPI rose to 3.2% yoy, sharply higher than the previous 2.1% yoy and above forecasts of 3.0%. That marks the fastest pace of annual inflation since Q2 2024. Electricity costs were again the main driver, soaring 23.6% from a year earlier despite targeted government relief measures.

Core inflation was equally strong. Trimmed mean CPI — the RBA’s preferred measure — rose 1.0% qoq, up from 0.7% and above expectations of 0.8%. Annually, core inflation accelerated to 3.0% yoy from 2.7%, underlining persistent price pressures across utilities and essential services, exceeding the RBA’s 2–3% target range again. This marks the first uptick in the trimmed mean since Q4 2022, confirming that underlying price momentum remains firm.

The data strengthen the case for the RBA to delay or even reconsider rate-cut expectations for the near term.

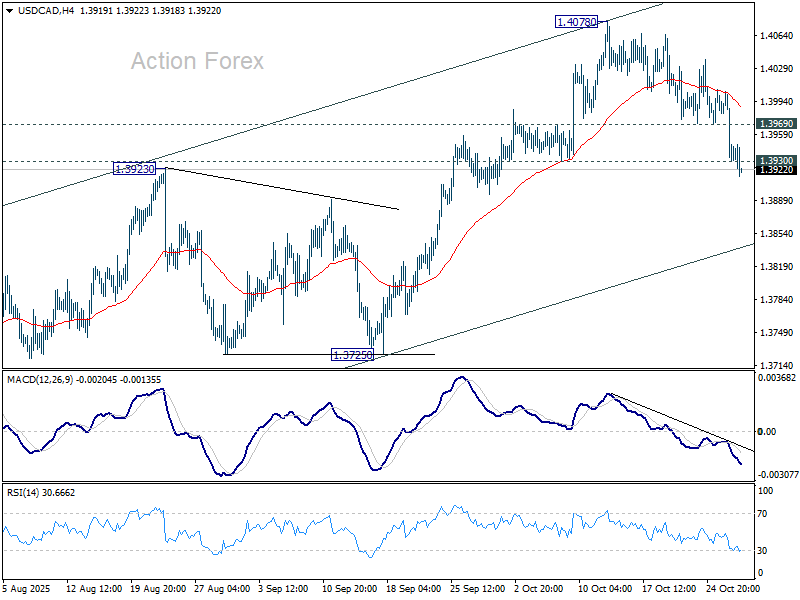

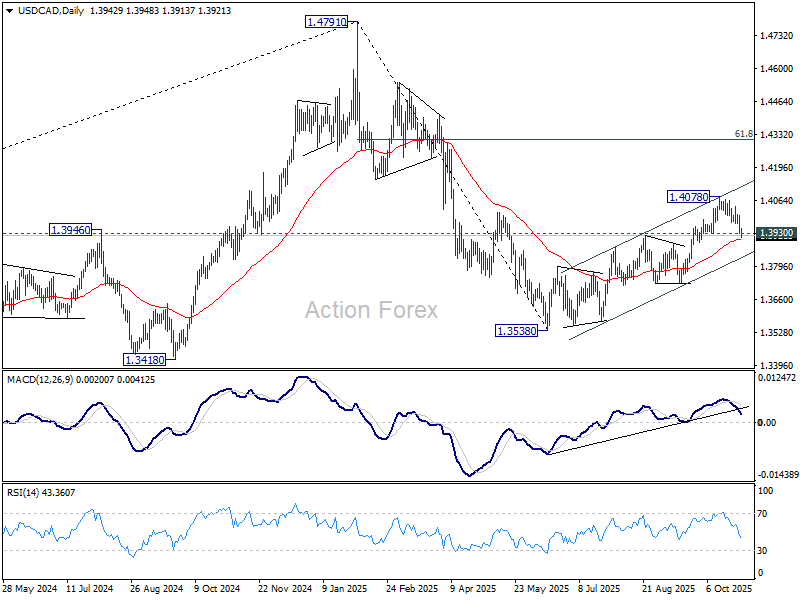

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3918; (P) 1.3962; (R1) 1.3989; More…

Intraday bias in USD/CAD is back now on the downside with break of 1.3930 support. Fall from 1.4078 should extend to rising channel support (now at 1.3835). Sustained break there will be a sign of bearish reversal. That is, rebound from has completed at 1.4078, and further fall would be seen to 1.3725 support for confirmation. On the upside, though, above 1.3969 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds. However, firm break of 1.3725 will revive the case that fall from 1.4791 is indeed a larger scale correction.