Dollar Extends Rally as Fed Hawks Push Back on Rate Cut – Action Forex

Dollar’s rally gained momentum as markets headed into the final U.S. session of both the week and the month, supported by a fresh round of hawkish remarks from Fed officials. After a few days dominated by post-FOMC positioning, the greenback found renewed strength as investors reconsidered the likelihood of another rate cut in December.

Kansas City Fed President Jeffrey Schmid, who dissented against this week’s 25-basis-point reduction, said the economy remained strong with inflation still “too high,” adding that monetary policy should continue to “lean against demand growth.” His comments were quickly echoed by Dallas Fed President Lorie Logan, who also argued that there was no need to cut rates this week given the economy’s resilience. Logan went further, suggesting that another cut in December would only be warranted if there were clear evidence of a faster decline in inflation or a sharp weakening in the labor market.

For now, futures markets still assign about a 60% probability of a 25-basis-point cut in December. However, if more Fed hawks step forward in the coming weeks, that pricing could slip closer to an even split, marking a notable shift from the 90% probability seen before Wednesday’s FOMC meeting.

In currency markets, Aussie remains the top performer of the week, but Dollar is closing in rapidly and could overtake by session’s end if buying persists. Loonie also ranks near the top, though its August GDP contraction has capped upside momentum. At the other end, Sterling continues to struggle, staying at the bottom alongside Swiss Franc and Yen, while Euro and Kiwi trade in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.31%. DAX is down -0.52%. CAC is down -0.44%. UK 10-year yield is down -0.013 at 4.419. Germany 10-year yield is down -0.01 at 2.638. Earlier in Asia, Nikkei rose 2.12%. Hong Kong HSI fell -1.43%. China Shanghai SSE fell -0.81%. Singapore Strait Times fell -0.20%. Japan 10-year JGB yield rose 0.012 to 1.659.

Fed’s Schmi: Cutting now won’t fix labor issues, may damage credibility

Kansas City Fed President Jeffrey Schmid offered a firm defense of his decision to oppose this week’s quarter-point rate cut, arguing that the U.S. economy remains resilient and inflation too high to justify further policy easing.

In a statement, Schmid said the labor market is “largely in balance”, the economy continues to show “momentum,” and policy remains “only modestly restrictive.” On that basis, he judged it appropriate to hold rates steady at this week’s meeting.

Schmid emphasized that monetary policy should continue to “lean against demand growth” to give supply room to expand and relieve price pressures.

The Kansas City Fed chief also highlighted the uneven effects of monetary policy on the Fed’s dual mandate. He noted that current labor market stresses are more structural, driven by technology and demographics, rather than cyclical weakness that rate cuts could effectively address. As such, he questioned the utility of further easing to support employment at this stage.

On the other hand, Schmid warned that even small rate reductions could have “longer-lasting effects on inflation” if markets begin to doubt the Fed’s commitment to its 2% target.

Canada GDP shrinks -0.3% mom in August, broad-based weakness offsets September rebound hopes

Canada’s economy contracted -0.3% mom in August, a much steeper decline than the expected flat reading, highlighting broad-based weakness across both goods and services sectors.

According to Statistics Canada, goods-producing industries fell -0.6%, marking the fifth contraction this year. Services-producing industries slipped -0.1%, the first decline in six months. The data reinforce concerns that Canada’s growth momentum remains fragile amid trade headwinds and domestic softness.

Looking ahead, advance estimates suggest GDP rose 0.1% mom in September, offering a modest sign of stabilization. Gains in finance, insurance, mining, oil and gas extraction, and manufacturing were partly offset by declines in wholesale and retail trade.

Eurozone CPI eases to 2.1%, but core holds firm at 2.4%

Eurozone inflation slowed slightly in October, though underlying price pressures remained sticky. According to the flash estimate, headline CPI edged down to 2.1% yoy from 2.2%, in line with expectations. Core inflation, which excludes energy, food, alcohol and tobacco, held steady at 2.4%, surprising on the upside compared with forecasts of 2.3%.

A closer look at the breakdown shows services inflation rose to 3.4% from 3.2%, confirming that the most persistent source of price pressure continues to come from the labor-intensive service sector. Meanwhile, food, alcohol and tobacco inflation eased to 2.5%, non-energy industrial goods slowed to 0.6%, and energy prices fell -1.0%, marking a deeper decline than September’s -0.4%.

Japan’s Tokyo core CPI surges to 2.8%, BoJ hike timing still unclear

Japan’s Tokyo CPI figures for October showed broad-based acceleration in inflation, adding to pressure on the BoJ but stopping short of forcing an immediate policy move. Core CPI (excluding fresh food) climbed from 2.5% to 2.8% yoy, beating expectations of 2.6%. Core-core measure (excluding fresh food and energy) matched that rise, also hitting 2.8%, while headline inflation accelerated from 2.5% to 2.8%.

The increase was driven partly by a 38.4% surge in rice prices and the expiration of water-fee subsidies, which lifted utility costs. Food inflation, excluding fresh items, remained high at 6.7%, though slightly slower than September’s 6.9%. Meanwhile, services inflation was relatively steady at 1.6%, well below the 4.1% gain in goods prices. The mix suggests cost pressures are persistent but not yet translating into sustained demand-led inflation.

At its meeting yesterday, the BoJ left the policy rate unchanged at 0.50%. Governor Kazuo Ueda said the likelihood of the Bank’s baseline projection materializing had “heightened somewhat,” but reiterated that the BoJ wants to await “a bit more data” before considering another rate hike. He emphasized the need to observe whether firms continue to raise wages in response to higher U.S. tariffs before committing to further tightening. Overall, the latest inflation data and BoJ remarks reinforce expectations that the next rate hike remains a coin toss between December and January.

Japan’s industrial production rises 2.2% mom in September, indecisive fluctuation continues

Japan’s industrial production rose 2.2% mom in September, beating expectations of 1.6% and marking the first increase in three months. However, the Ministry of Economy, Trade and Industry kept its assessment unchanged, describing output as “fluctuating indecisively,” highlighting that the recovery remains fragile.

According to METI’s survey, manufacturers expect production to grow 1.9% mom in October but shrink -0.9% in November, pointing to continued short-term volatility.

Gains in September were broad-based, with 13 of 15 industrial sectors expanding. Notably, production machinery output surged 6.2% mom, driven by strong shipments of semiconductor manufacturing equipment to China and Taiwan. In contrast, transport equipment (excluding motor vehicles) and steel and non-ferrous metals recorded modest declines.

Meanwhile, retail sales rose 0.5% yoy, missing expectations of 0.7%, reflecting soft consumer demand despite improving wage and price trends.

China NBS Manufacturing PMI falls to 49 in October, contraction deepens

China’s official manufacturing PMI fell from 49.8 to 49.0 in October, missing expectations of 49.7 and marking the lowest reading in six months. The sector has now been in contraction since April. The new orders index dropped to 48.8 from 49.7, while the production sub-index declined sharply to 49.7 from 51.9, pointing to a broad slowdown in both output and demand.

NBS chief statistician Huo Lihui attributed the weaker reading to “the early release of some demand before the National Day holiday” and a “more complex international environment” that continues to weigh on activity.

Outside the factory sector, Non-Manufacturing PMI edged up slightly to 50.1 from 50.0, though it also missed forecasts of 50.2. As a result, the Composite PMI, which combines manufacturing and services, slipped to 50.0 from 50.6.

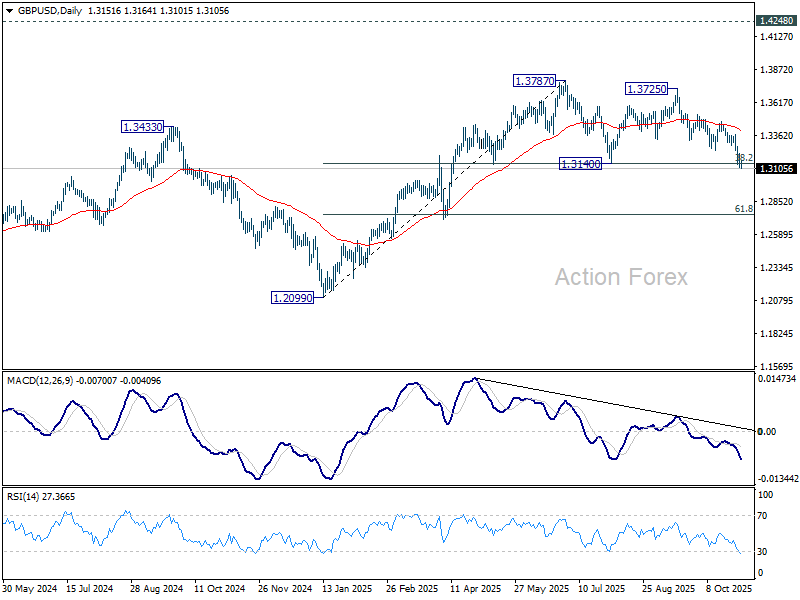

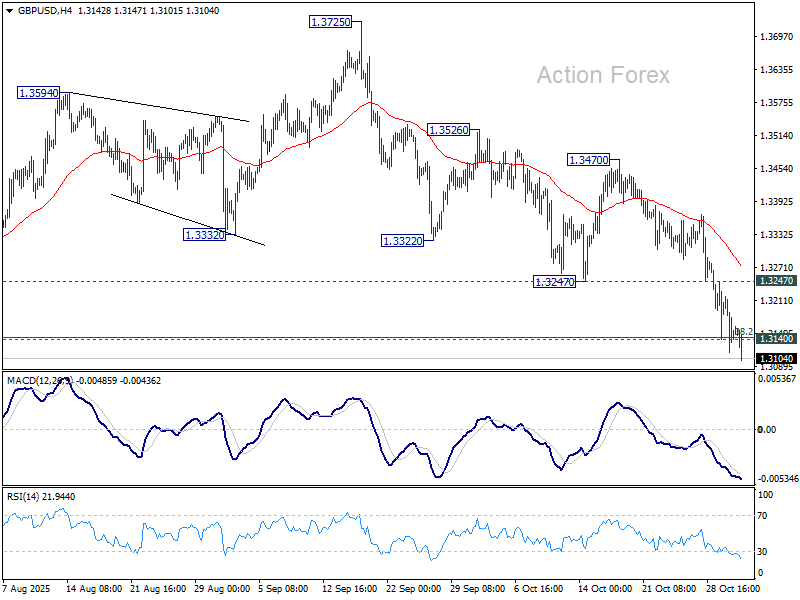

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3105; (P) 1.3162; (R1) 1.3207; More…

GBP/USD’s decline continues today and the break of 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142) now suggests that a double top pattern (1.3787/3725) was already in place. Intraday bias stays on the downside for 61.8% retracement at 1.2744 next. On the upside break of 1.3247 support turned resistance is needed to indicate short term bottoming. Otherwise, risk will stay on the downside in case of recovery.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Sustained trading below 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099. Firm break there will confirm bearish reversal. In case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside.