Dollar Rises Along with Yields as Fed Expectations Adjustment Continues – Action Forex

Dollar extended its rebound as North American trading got underway, gaining further momentum following Wednesday’s hawkish Fed rate cut. The greenback’s strength came as markets continued to digest the Fed’s divided decision and Chair Jerome Powell’s pushback against expectations for another cut in December.

U.S. Treasury yields also climbed, with the 10-year yield breaking above 4.1% and appearing poised to extend its near-term rebound. The move reflects a market reassessment of the Fed’s trajectory after Powell emphasized that future easing is “not a foregone conclusion.” As a result, the probability of a December rate cut has slipped to 68.8%, down sharply from around 90% at the start of the week.

Still, the broader policy debate remains nuanced. The Fed’s latest Summary of Economic Projections places the neutral rate—the level neither stimulating nor restricting the economy—within a 2.8% to 3.5% range. With the current policy rate at 3.75–4.00%, the stance is still modestly restrictive, but not overly tight. Some policymakers may still see room to bring rates slightly closer to neutral as a form of insurance, particularly given the data blackout caused by the ongoing government shutdown.

For now, Dollar is the day’s top performer, followed by Swiss Franc and Euro, which is trading cautiously ahead of the ECB decision. The euro remains steady, with investors expecting the central bank to hold its deposit rate at 2.00% and maintain a neutral tone, signaling comfort with current policy settings.

At the other end of the spectrum, Yen is under heavy pressure, with selling resuming after the BoJ’s uneventful policy hold. Aussie and Kiwi also softened, reflecting a cooling of risk-on sentiment following earlier optimism over the Trump–Xi trade deal. Elsewhere, Sterling and Loonie are trading mid-pack.

On the trade front, China’s Commerce Ministry said it will cooperate with the U.S. to “properly resolve” issues surrounding TikTok’s U.S. operations. But there is not timeline nor details provided. TikTok will likely remain a sticky issue despite the progress in de-escalation trade tension with the Trump–Xi summit in South Korea.

In Europe, at the time of writing, FTSE is down -0.61%. DAX is down -0.15%. CAC is down -0.91%. UK 10-year yield is up 0.005 at 4.445. Germany 10-year yield is up 0.032 at 2.657. Earlier in Asia, Nikkei rose 0.04%. Hong Kong HSI fell -0.24%. China Shanghai SSE fell -0.73%. Singapore Strait Times fell -0.06%. Japan 10-year JGB yield fell -0.007 to 1.647.

Eurozone GDP beats expectations with 0.2% growth in Q3

The Eurozone economy expanded by 0.2% qoq in Q3, outpacing expectations of a 0.1% increase. EU GDP rose 0.3% qoq, marking a modest but welcome pickup in growth momentum. Compared with the same period last year, seasonally adjusted GDP grew 1.3% yoy in the Eurozone and 1.5% across the EU.

Among member states, performance was uneven but generally positive. Sweden led the bloc with a robust 1.1% quarterly increase, followed by Portugal (+0.8%) and Czechia (+0.7%). In contrast, Lithuania (-0.2%), Ireland, and Finland (both -0.1%) saw mild contractions. The data show that 14 countries posted positive year-on-year growth, with only one economy contracting.

Swiss KOF climbs to 101.3, outlook brightens

Switzerland’s KOF Economic Barometer rose more than expected in October, advancing from 98.0 to 101.3 against forecasts of 99.0. The index’s move above the 100-threshold suggests that short-term prospects are now slightly above the long-term average, hinting at a firmer growth backdrop heading into year-end.

The KOF Institute noted that most indicator groups contributed positively to the uptick. In particular, manufacturing, financial and insurance services, and other service industries all displayed a more favorable outlook. However, the report pointed out a setback in private consumption, underscoring that household spending remains a relative weak spot even as business sentiment strengthens.

BoJ holds at 0.50%, keeps gradual tightening bias intact

The BoJ left its overnight call rate unchanged at 0.50% as widely expected. The decision came by a 7–2 vote, with Hajime Takata and Naoki Tamura again dissenting in favor of a 25bps rate hike to move policy a little closer to neutral. The repeat split highlights the growing divergence within the board as policymakers debate how quickly to normalize monetary conditions.

In its quarterly Outlook Report, the BoJ made only marginal revisions to its forecasts, signaling that the economic and inflation outlook remains broadly stable. The bank raised its fiscal 2025 GDP forecast slightly from 0.6% to 0.7%, while projections for 2026 and 2027 were left unchanged at 0.7% and 1.0%, respectively.

On prices, the BoJ kept its core CPI forecast at 2.7% for 2025, 1.8% for 2026, and 2.0% for 2027. Core-core CPI (excluding both fresh food and energy) was nudged higher to 2.0% in 2026 from 1.9%, with other years unchanged (2026 at 2.8% and 2027 at 2.0%). The bank reiterated that underlying inflation is expected to reach 2% in the latter half of the projection period through March 2027, retaining language from July that risks to the inflation outlook remain “roughly balanced.”

The BoJ also reiterated that it would continue to raise its policy rate and adjust the degree of monetary support “in accordance with improvements in the economy and prices.”

New Zealand ANZ business confidence surges to seven-month high, green shoots emerging

New Zealand’s ANZ Business Confidence Index surged sharply in September, rising from 49.6 to 58.1, the highest level since February. Own Activity Outlook also improved modestly, up from 43.4 to 44.6, marking its strongest reading since April.

Inflation expectations, meanwhile, remained broadly steady. The share of firms expecting to raise prices over the next three months eased slightly from 46% to 44%. Those anticipating cost increases ticked up from 75% to 76%. One-year-ahead inflation expectations edged higher from 2.71% to 2.75%.

ANZ noted that “green shoots are emerging, particularly for interest-rate-sensitive sectors.” The bank highlighted stronger retail sentiment as evidence that the economy is beginning to warm alongside the spring season, with monetary easing and high rural incomes supporting regional confidence and broader recovery momentum.

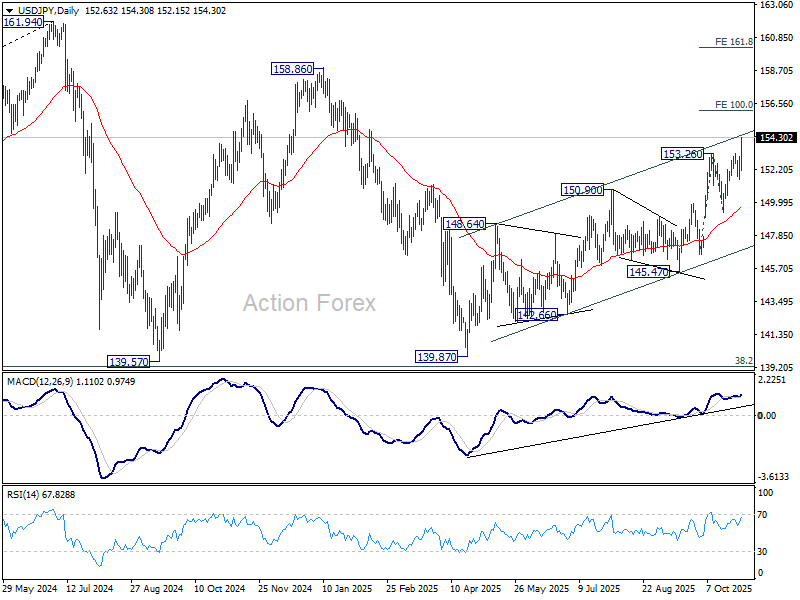

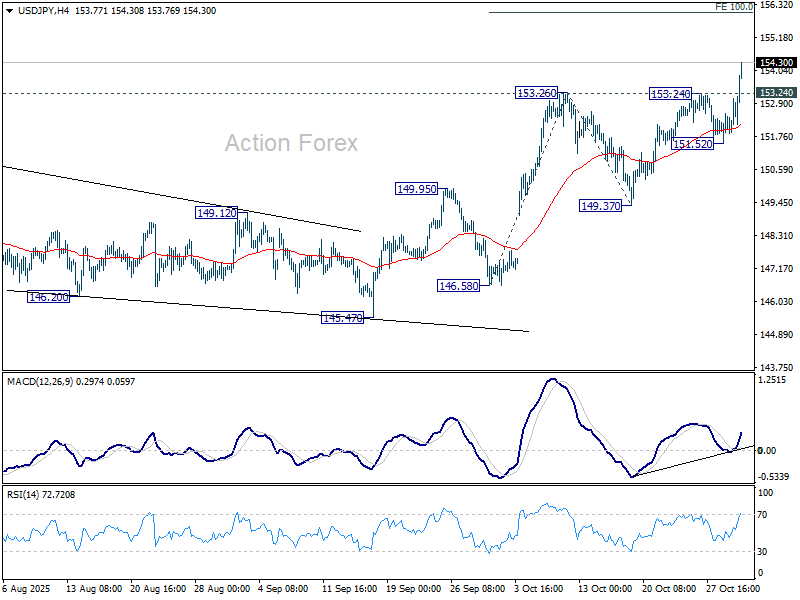

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.83; (P) 152.45; (R1) 153.35; More…

Dollar’s strong break of 153.26 confirms resumption of whole rise from 139.87. Intraday bias is back on the upside for 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Firm break there will target 158.86 resistance next. On the downside, below 153.24 resistance turned support will turn intraday bias neutral first. But outlook will stay bullish as long as 151.52 support holds, in case of retreat.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.