Volatility Surges as Central Bank Bonanza Starts; BoC and Fed to Cut Today – Action Forex

Volatility picked up sharply as markets entered the first leg of a two-day central bank bonanza, with the BoC and the Fed set to announce policy decisions today, followed by the BoJ and European ECB tomorrow. Traders are bracing for a flurry of rate moves, guidance shifts, and potential surprises that could set the tone for global markets into November.

Aussie leads the weekly performance chart, bolstered by today’s stronger-than-expected CPI report that forced traders to rapidly unwind bets on a near-term RBA rate cut. The stronger inflation pulse, coupled with firmer activity data, reinforced the case for the RBA to hold rates steady for an extended period.

That view gained further traction after CBA became a major domestic bank to call for no more rate cuts in the current cycle. The bank’s economists emphasized that the RBA would need to see a “material” rise in unemployment and softer inflation before considering renewed easing.

Commodity-linked peers also benefited. Kiwi and Loonie advanced in tandem, buoyed by firm risk appetite as Wall Street hit new highs. Optimism that the U.S.–China tariff truce will be extended past November helped sustain the global equity rally, with DOW, S&P 500, and NASDAQ all closing at record levels overnight.

Meanwhile, Yen saw renewed buying interest after U.S. Treasury Secretary Scott Bessent voiced support for Japan’s monetary independence, urging Prime Minister Sanae Takaichi’s new government to allow the BoJ to decide its policy direction without political pressure. The remarks were widely interpreted as a signal that Washington would not object to a potential BoJ rate hike in coming months. Still, Yen’s strength failed to offset the broader strength in risk and commodity currencies. Yen is sitting mid-table along with Swiss Franc.

At the weaker end of the spectrum, Sterling remains under heavy pressure amid renewed fiscal worries. Reports of a GBP 20B deterioration in the UK’s public finances have dented confidence in Chancellor Rachel Reeves’ upcoming budget plans. Dollar is the second weakest major as traders await tonight’s Fed decision, where a 25bps cut is fully priced in, followed by Euro which rounds out the top three.

Focus now turns squarely to the BoC and Fed announcements later today. Both are expected to cut interest rates by 25bps, but forward guidance will be crucial. The BoC is likely nearing the end of its easing cycle, while the Fed’s tone will shape expectations for an additional cut in December.

In Asia, at the time of writing, Nikkei is up 2.21% at new record. Hong Kong is on holiday. China Shanghai SSE is up 0.41%. Singapore Strait Times is down -0.22%. Japan 10-year JGB yield is up 0.015 at 1.655. Overnight, DOW rose 0.34%. S&P 500 rose 0.23%. NASDAQ rose 0.80%. 10-year yield fell -0.014 to 3.983.

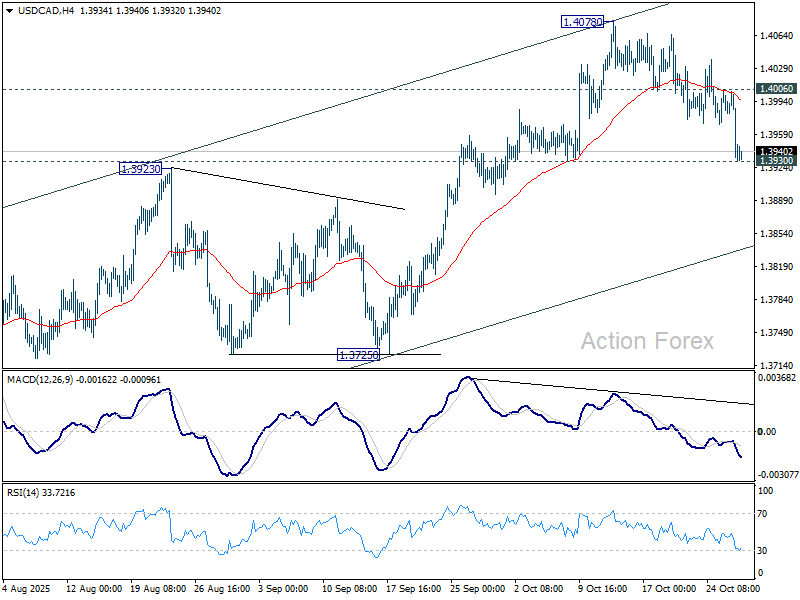

USD/CAD break or hold? 1.3930 support tested ahead of BoC–Fed double cuts

Global attention turns to North America today, with both the BoC and the Fed expected to deliver 25bps rate cuts. The BoC’s decision will come first at 13:45 GMT, followed by the Fed’s announcement later at 18:00 GMT.

The BoC’s overnight rate is widely expected to fall to 2.25%, reflecting the bank’s persistent concern about growth despite recent resilience in jobs and inflation data. Policymakers remain uneasy about the impact of U.S. tariffs and weak domestic demand, even as headline inflation overshoots target. For Governor Tiff Macklem and his team, the near-term goal remains cushioning the economy without reigniting price pressures.

Most analysts expect today’s cut to be the final one of this cycle, with the BoC likely to enter a prolonged pause. A Reuters poll showed 21 of 34 economists forecasting rates at 2.25% by the end of 2026, implying stability for an extended period. Only eight respondents saw further easing to 2.00% or below.

Still, the balance of risks leans dovish, as agreed by most, and a terminal rate at 2.00% is a real possibility. Growth remains soft, exports are vulnerable to trade restrictions, and business confidence has yet to rebound. Policymakers are likely to leave the door open for further cuts without explicitly signaling another move.

Attention will then shift to the Fed, which is widely expected to lower the federal funds rate to 3.75–4.00%. Futures markets also price in a 90% probability of another 25bps cut in December, taking the target range to 3.50–3.75%.

However, the 2026 policy path remains clouded by diverging risks — inflation could reaccelerate if tariffs bite harder, even as the labor market shows signs of fatigue. A recent Reuters survey reflected this uncertainty, showing economists split seven ways on where rates might stand by the end of next year — anywhere between 2.25%–2.50% and 3.75%–4.00%.

The debate has been complicated further by speculation over who will replace Chair Jerome Powell when his term ends in May. Treasury Secretary Scott Bessent confirmed earlier this week that the shortlist includes Fed Governors Christopher Waller and Michelle Bowman, National Economic Council Director Kevin Hassett, former Fed Governor Kevin Warsh, and BlackRock executive Rick Rieder, all representing slightly different shades of monetary philosophy.

Given that backdrop, Powell is unlikely to make any firm commitments on policy beyond today’s meeting. Markets will instead look to the December Summary of Economic Projections and updated dot plot for clarity on the 2026 rate path.

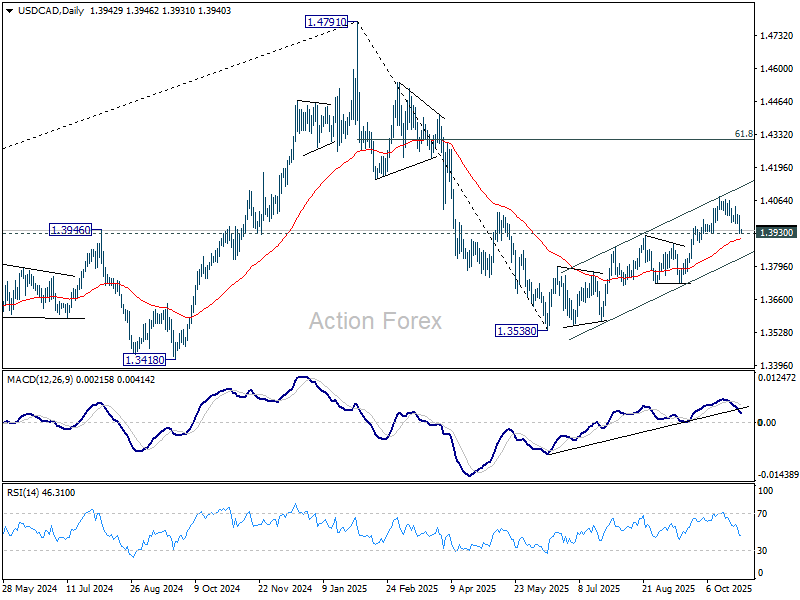

In the currency markets, USD/CAD has weakened sharply just ahead of the twin policy events, hovering just above 1.3930 support after yesterday’s selloff. A rebound from current levels would keep the broader uptrend from 1.3538 intact, with a break above 1.4006 suggesting the rally’s resumption through 1.4078.

Conversely, decisive break below 1.3930 would signal that the advance has likely topped, opening the way for a deeper pullback toward the channel floor near 1.3829, where the next key directional cue will emerge.

Australia inflation shock: CPI surges to 3.2%, core re-accelerates

Australia’s inflation surprised sharply to the upside in Q3, reigniting concerns that price pressures are proving stickier than expected. Headline CPI jumped 1.3% qoq, accelerating from 0.7% in Q2 and beating expectations of 1.1% — marking the strongest quarterly increase since Q1 2023. The Australian Bureau of Statistics said the largest contributor was a 9.0% rise in electricity costs, which alone drove much of the headline surge.

On an annual basis, CPI rose to 3.2% yoy, sharply higher than the previous 2.1% yoy and above forecasts of 3.0%. That marks the fastest pace of annual inflation since Q2 2024. Electricity costs were again the main driver, soaring 23.6% from a year earlier despite targeted government relief measures.

Core inflation was equally strong. Trimmed mean CPI — the RBA’s preferred measure — rose 1.0% qoq, up from 0.7% and above expectations of 0.8%. Annually, core inflation accelerated to 3.0% yoy from 2.7%, underlining persistent price pressures across utilities and essential services, exceeding the RBA’s 2–3% target range again. This marks the first uptick in the trimmed mean since Q4 2022, confirming that underlying price momentum remains firm.

The data strengthen the case for the RBA to delay or even reconsider rate-cut expectations for the near term.

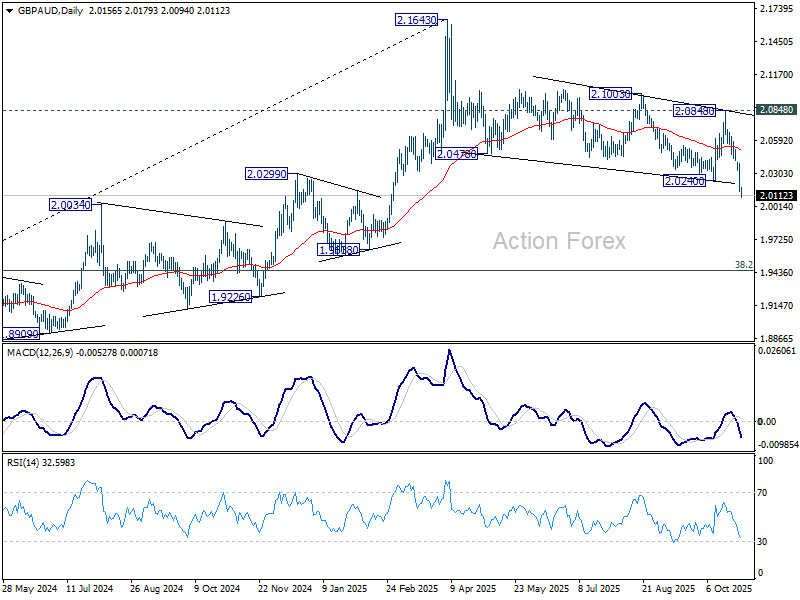

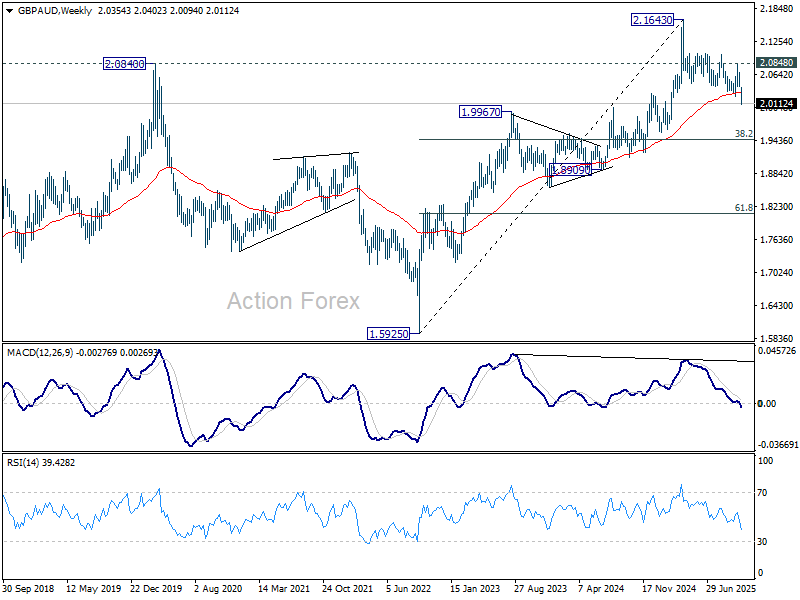

Aussie soars, Sterling slumps, GBP/AUD confirms medium term bearish turn

Aussie surged sharply on after the hotter-than-expected inflation print shattered hopes for a RBA rate cut next week. Crucially, the upside surprise wasn’t confined to energy-driven headline gains. The broad-based acceleration in core inflation confirmed that price pressures have become more entrenched.

RBA Governor Michele Bullock had warned earlier this week that any 0.9% or higher quarterly increase in the trimmed mean would constitute a “material miss.” The 1.0% outcome squarely fits that definition, virtually guaranteeing the central bank will keep rates unchanged at next week’s policy meeting. With economic activity showing tentative signs of recovery, the balance of risks has shifted decisively toward fewer rate cuts over the next year.

In the currency markets, Aussie’s rally coincided with broad-based weakness in the British pound, which remains weighed down by fiscal concerns following reports of a worsening UK budget shortfall. As a result, GBP/AUD has become the week’s standout mover for now, falling more than 1.5% to its lowest levels in months.

Technically, GBP/AUD’s break of 2.0240 support confirms resumption of the decline from 2.1643. More importantly, the decisive break below the 55 W EMA (now at 2.0309) reinforces a bearish bias, confirming a medium-term top at 2.1643 under bearish MACD divergence conditions.

The fall from 2.1643 high is viewed as at least correcting the entire rise from 1.5925 (2022 low), with scope to even reversing the whole move.

In either case, as long as 2.0858 resistance holds, the outlook remains bearish with the next target at 38.2% retracement of 1.5925 to 2.1643 at 1.9459.

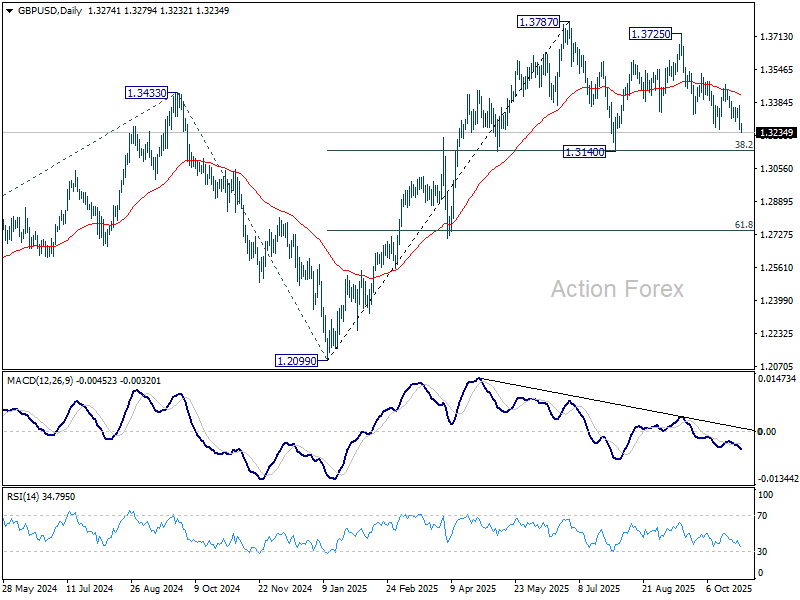

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3223; (P) 1.3297; (R1) 1.3345; More…

GBP/USD’s fall from 1.3725 resumed by breaking through 1.3247 support today. Intraday bias is now on the downside for 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, above 1.3368 minor resistance will turn intraday bias neutral first. However, decisive break of 1.3140/2 will complete a double top pattern (1.3787/3725) and turn near term outlook bearish.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.