Dollar Extends Gains as Markets Dismiss Dovish Fed Remarks, RBA in Focus Next – Action Forex

Dollar climbed across the board today, defying dovish rhetoric from Fed Governor Stephen Miran. The greenback’s resilience suggests that Miran’s influence on expectations is limited, with investors noting that he represents the dovish edge of a divided policy spectrum.

The broader committee remains split. Kansas City Fed President Jeffrey Schmid argued recently against imminent rate cuts, while Governor Christopher Waller has indicated more openness to easing. With such divergent signals, markets are reluctant to price in aggressive near-term action, instead waiting for the next set of meaningful data.

That makes this week’s private-sector reports — ISM Manufacturing and Services, along with ADP employment — particularly crucial. With the U.S. government still partially shut down and official data releases suspended, traders are relying on these indicators to gauge whether the economy retains its resilience or is slipping under the weight of high rates.

Also, with no consensus emerging, the Fed’s upcoming communications will be heavily scrutinized for any hint of a shift toward a clearer majority view.

In the next Asian session, attention is turning to the RBA’s policy decision. Aussie held firm as markets positioned for a hawkish hold following last week’s stronger-than-expected CPI. All of Australia’s Big Four banks now expect the RBA to remain on hold through year-end, with differing views on when cuts might resume.

ANZ and Westpac see February as a “plausible” but uncertain window, NAB projects a move in the June quarter, while Commonwealth Bank expects no further reductions in the foreseeable future. Bullock’s remarks will likely determine whether markets stick with these cautious timelines or push back expectations further.

In today’s currency markets, Dollar leads the pack, followed by Aussie and Sterling. The Swiss Franc lags behind, with Loonie and Euro also under pressure. Yen and Kiwi sit mid-field.

In Europe, at the time of writing, FTSE is down -0.03%. DAX is up 0.83%. CAC is down -0.09%. UK 10-year yield is up 0.021 at 4.429. Germany 10-year yield is up 0.025 at 2.660. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.97%. China Shanghai SSE rose 0.55%. Singapore Strait Times rose 0.35%.

Fed’s Miran warns policy too tight amid credit market stress

Fed Governor Stephen Miran cautioned that U.S. monetary policy may already be too restrictive, arguing that the neutral rate sits “quite a ways” below the current stance. Speaking with Bloomberg TV, Miran said his relatively sanguine view on inflation suggests there is “no reason for keeping policy as restrictive” .

Miran also highlighted emerging strains in credit markets as a warning sign that policy may have overshot. He noted that “a series of seemingly uncorrelated credit problems” surfacing across sectors indicates financial stress that was previously masked by strong headline data.

“The longer you keep policy restrictive, the more you run the risk that monetary policy itself causes a downturn,” Miran warned.

UK PMI manufacturing finalized at 49.7, Budget may deepen structural strain

UK manufacturing showed tentative signs of life in October, with the final S&P Global PMI rising to 49.7 from September’s 46.2. However, the improvement remains fragile as sluggish demand and stock adjustments drove much of the uptick rather than a sustained pickup in new orders.

Rob Dobson, Director at S&P Global Market Intelligence, said the October survey was encouraging but cautioned that the rebound “could prove short-lived.” Output growth largely stemmed from manufacturers working through backlogs and allowing inventories to build amid weak demand at home and abroad.

Dobson added that upcoming fiscal developments could complicate the outlook further. Many firms worry that the forthcoming Budget may aggravate structural challenges left by last year’s policy tightening, weighing on confidence even as activity improves. Business optimism rose to an eight-month high but remains below its long-run average.

Eurozone PMI manufacturing at 50.0, very delicate sprout of economic recovery

Eurozone manufacturing activity barely expanded in October, with the final HCOB PMI coming in at 50.0, up marginally from 49.8 in September. National readings showed uneven trends: Greece and Spain led with readings above 52, while Germany (49.6) and Italy (49.9) hovered just below the neutral mark. France and Austria remained in contraction, both at 48.8.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, described the improvement as a “very delicate sprout of economic recovery.” Output has risen for eight consecutive months, but new orders remain stagnant, suggesting that growth lacks momentum. The survey also showed that overall demand across the Eurozone remains subdued, with factories struggling to generate fresh business despite tentative output gains.

The regional breakdown highlights persistent divergence. Germany’s factory sector remains fragile, France’s is in recession, and Italy’s shows only persistent weakness. Meanwhile, Spain’s moderate expansion stands out but offers limited offset. De la Rubia warned that France’s political tensions and renewed production slump are weighing on cross-border demand, acting as a drag on its trading partners and complicating hopes for a broader industrial rebound heading into year-end.

Swiss CPI slows to 0.1% yoy in October, broad decline in prices

Swiss inflation cooled further in October, with headline CPI slipping -0.3% mom — weaker than expectations of -0.1% mom. Annual inflation eased to just 0.1% yoy from 0.2% yoy, undershooting forecasts of 0.3% yoy. The data confirmed that price pressures remain virtually absent.

Core inflation also weakened notably, falling -0.2% mom and slowing to 0.5% yoy from 0.7% yoy. Both domestic and imported prices fell during the month, by -0.2% mom and -0.5% mom respectively, suggesting broad-based softness. The sharper decline in imported prices reflects the strong franc’s continued dampening effect on imported goods and energy costs, while domestic components also showed only marginal resilience.

China RatingDog PMI manufacturing falls to 50.6; export orders and prices decline

China’s manufacturing activity expanded at a slower pace in October, with the RatingDog PMI easing to 50.6 from 51.2, missing expectations of 50.9. The moderation reflects weaker demand momentum and growing headwinds from global trade tensions, which weighed on both output and new export orders.

According to RatingDog founder Yao Yu, both demand and production expansion softened. Export orders fell “sharply into contraction territory” as heightened trade uncertainty curbed overseas demand. Production growth also cooled, though sub-indices remained in expansion territory. Purchasing activity “slowed significantly”, signaling greater caution among manufacturers heading into year-end.

Price pressures was a drag on profits, as raw material costs rose while finished goods prices fell. Exporters reduced selling prices for the first time since April to stay competitive amid fragile external demand. Still, the survey offered a bright spot: the employment index returned to expansion for the first time since March, reaching its highest level since August 2023.

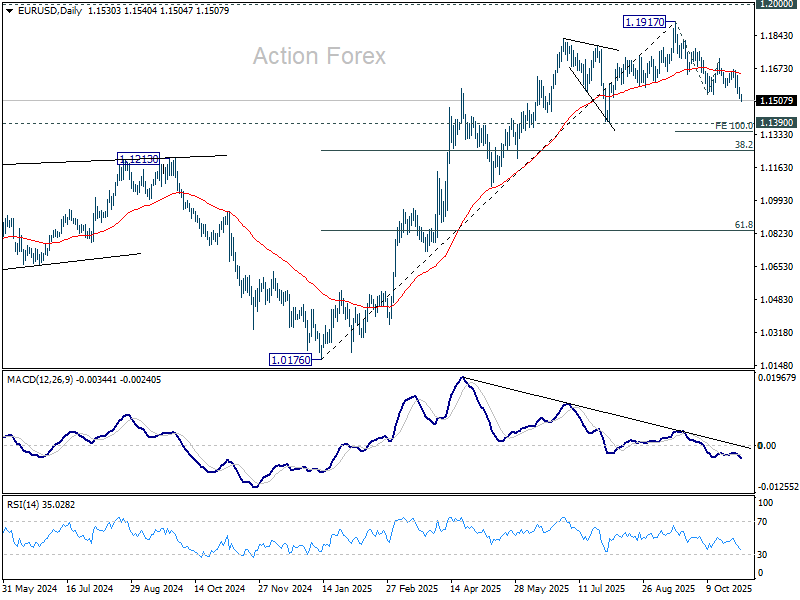

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1513; (P) 1.1545; (R1) 1.1569; More…

EUR/USD’s fall from 1.1917 continues today and 4H MACD suggests that downside momentum remains firm. Intraday bias stays on the downside for 100% projection of 1.1917 to 1.1540 from 1.1727 at 1.1350. Decisive break there would prompt downside acceleration to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1576 minor resistance will turn bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1306) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.